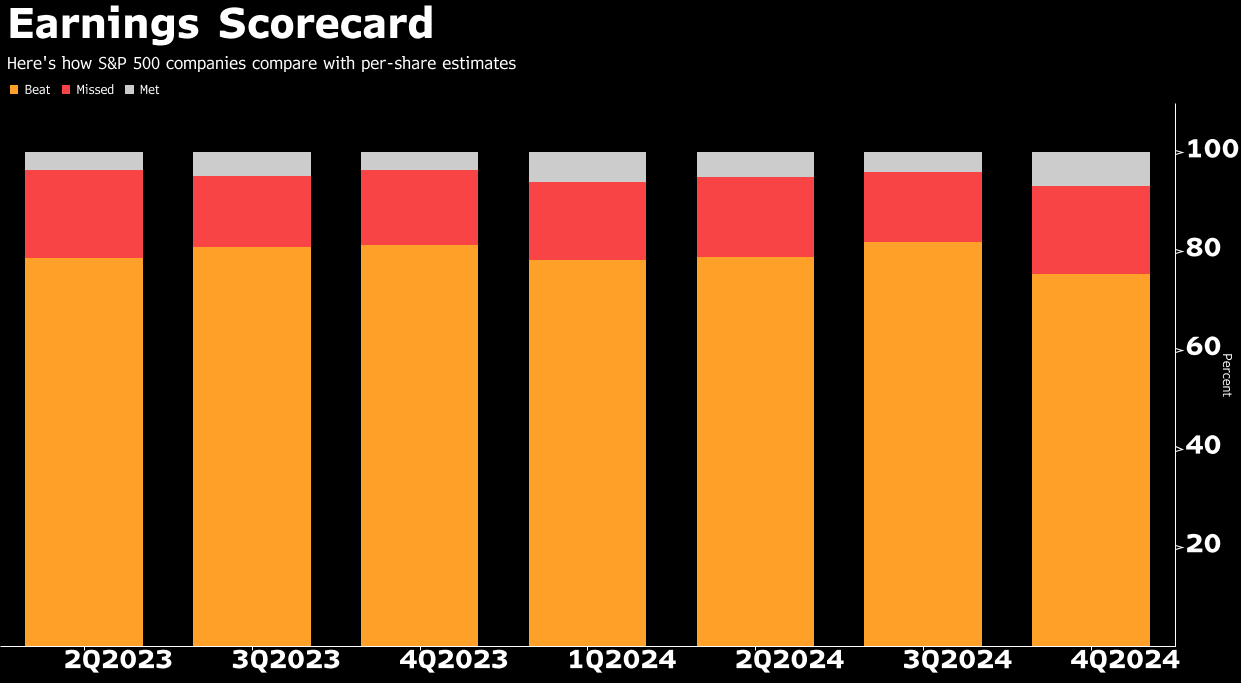

The American market has accustomed investors over recent quarters not only to dynamic growth but also to consistently surpassing consensus expectations. This makes the current earnings season look particularly weak compared to previous quarters. For the first time since Q4 2023, the percentage of S&P 500 companies that exceeded earnings-per-share (EPS) expectations has fallen below 80%. So far, only 75% of companies have reported better-than-expected results. Moreover, the share of companies reporting weaker-than-expected earnings is rising—currently at 18%, compared to 16% a year ago.

Share of companies that have exceeded expectations (orange), reported weaker results (red), and reported in line with expectations (gray). Source: Bloomberg Finance L.P.

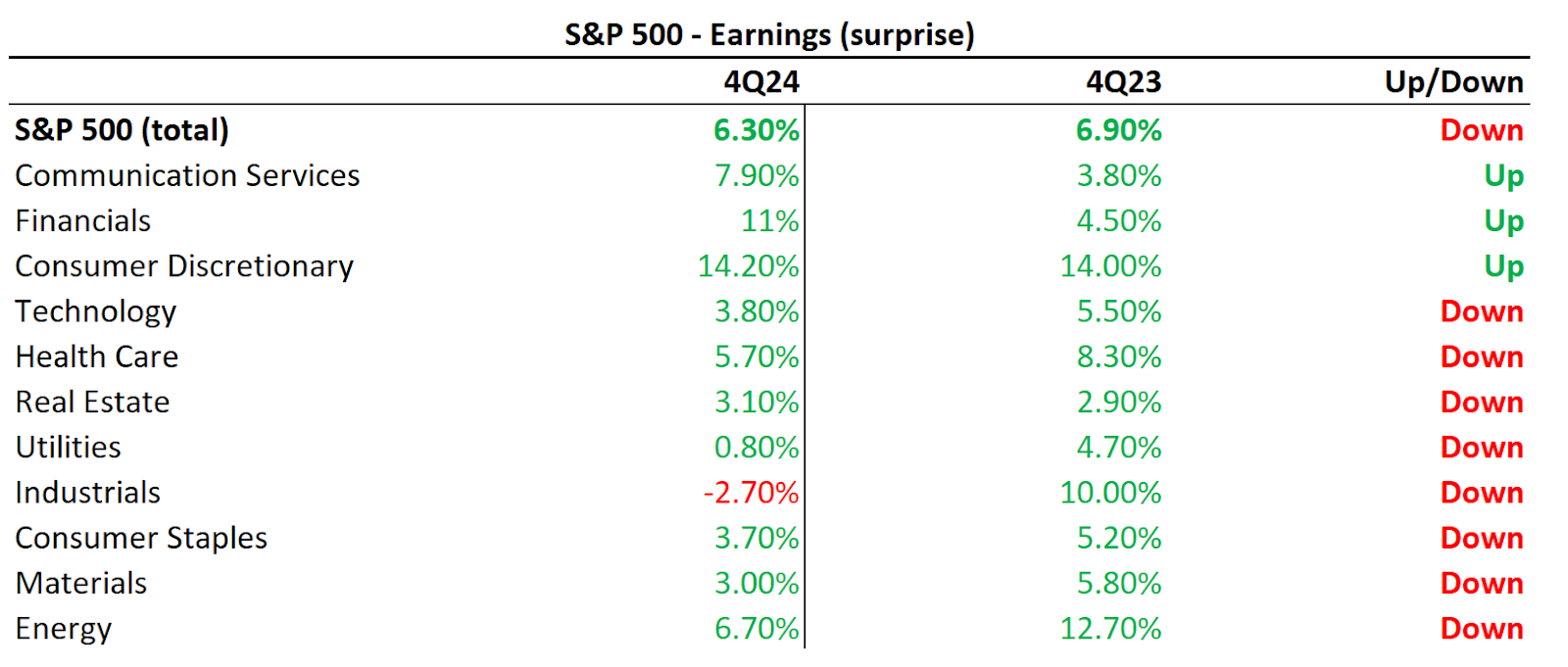

Among sectors, utilities are performing the worst. In this segment, only 47% of companies have reported earnings above expectations, while as many as 33% have shown lower profits. The strongest sector so far is finance, where 85% of companies have posted better-than-expected results. Additionally, the average EPS beat relative to expectations in this sector is the second highest after consumer discretionary, reaching 11%.

Compared to Q4 2023, only three sectors have shown a higher positive earnings surprise than a year earlier: financials, communication services, and consumer discretionary

Average difference in reported EPS versus consensus. Source: XTB Research, LSEG

Daily Summary: Markets limit the pullback while awaiting the Fed

France Challenges Palantir, Market Reacts.

US OPEN: Deeper sell-off and a SaaS rebound

Mercedes earninigs: Is optimism justified?

The content of this report has been created by XTB S.A., with its registered office in Warsaw, at Prosta 67, 00-838 Warsaw, Poland, (KRS number 0000217580) and supervised by Polish Supervision Authority ( No. DDM-M-4021-57-1/2005). This material is a marketing communication within the meaning of Art. 24 (3) of Directive 2014/65/EU of the European Parliament and of the Council of 15 May 2014 on markets in financial instruments and amending Directive 2002/92/EC and Directive 2011/61/EU (MiFID II). Marketing communication is not an investment recommendation or information recommending or suggesting an investment strategy within the meaning of Regulation (EU) No 596/2014 of the European Parliament and of the Council of 16 April 2014 on market abuse (market abuse regulation) and repealing Directive 2003/6/EC of the European Parliament and of the Council and Commission Directives 2003/124/EC, 2003/125/EC and 2004/72/EC and Commission Delegated Regulation (EU) 2016/958 of 9 March 2016 supplementing Regulation (EU) No 596/2014 of the European Parliament and of the Council with regard to regulatory technical standards for the technical arrangements for objective presentation of investment recommendations or other information recommending or suggesting an investment strategy and for disclosure of particular interests or indications of conflicts of interest or any other advice, including in the area of investment advisory, within the meaning of the Trading in Financial Instruments Act of 29 July 2005 (i.e. Journal of Laws 2019, item 875, as amended). The marketing communication is prepared with the highest diligence, objectivity, presents the facts known to the author on the date of preparation and is devoid of any evaluation elements. The marketing communication is prepared without considering the client’s needs, his individual financial situation and does not present any investment strategy in any way. The marketing communication does not constitute an offer of sale, offering, subscription, invitation to purchase, advertisement or promotion of any financial instruments. XTB S.A. is not liable for any client’s actions or omissions, in particular for the acquisition or disposal of financial instruments, undertaken on the basis of the information contained in this marketing communication. In the event that the marketing communication contains any information about any results regarding the financial instruments indicated therein, these do not constitute any guarantee or forecast regarding the future results.