Berkshire Hathaway is an investment company founded and led by one of the most legendary investors of all time - Warren Buffett. Over the past decades, the firm has delivered excellent and very consistent results. Its performance was particularly impressive during prolonged bear markets, such as the 2022–2023 downturn.

However, due to his advanced age, Warren Buffett had to step down as chief manager, handing the role to Greg Abel. The company published its first results under the leadership of the new CEO.

Financial metrics:

- Revenue: up more than 4% year over year to USD 93.7 billion.

- Operating profit: up 17% year over year to USD 11.35 billion.

- Net income attributable to shareholders: up nearly 120% to USD 10.1 billion.

- Share buybacks: USD 234 million.

- Cash: another record at USD 373.5 billion.

In terms of metrics and growth, the company continues to operate exceptionally well, slightly beating market consensus expectations. Despite Warren Buffett’s legendary status, the new CEO is also not in the spotlight.

What fuels the most debate around the company is its behavior relative to the broader market and its enormous cash position. Over the long term, Berkshire has outperformed the S&P 500 by a wide margin; however, in recent quarters the fund has clearly lagged the broader market - by around 12% versus the benchmark index.

This is particularly controversial given the huge cash pile. In previous market cycles, a high cash balance at the company signaled that it was waiting for the right moment to make large (ultimately very profitable) purchases. This sentiment regarding the company’s approach has been visible for quite some time, and the further the S&P 500 pulls ahead of Berkshire’s returns, the more questions market participants begin to ask.

That view of the fund may be fundamentally misguided. Berkshire is an investment company with a fundamentally different profile than today’s S&P 500, which is dominated by technology firms.

Warren Buffett’s genius came from his exceptional ability to generate growth during periods when market sentiment was negative. Berkshire prioritizes protecting investors’ capital first, and only then seeks to generate above-normal returns.

In recent quarters, however, the market appears to have remained in a mode of unwavering euphoria, almost entirely concentrated in technology stocks. Funds such as Berkshire cannot consistently beat broad-market returns, because doing so would require an unacceptable level of risk.

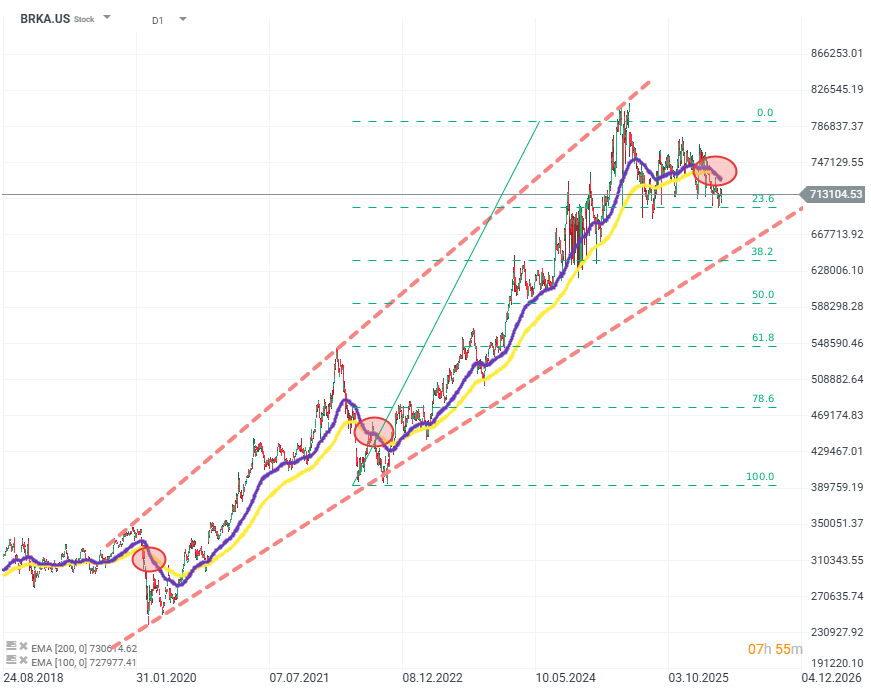

BRKA.US (D1)

On the chart, one can observe the EMA200 and EMA100 crossover from above for the first time since 2022. Historically, such behavior—contrary to traditional technical analysis—has preceded long-lasting growth periods. Will it be the same this time? Source: xStation5

Daily Summary: Equities Diverge as Tech Lags, Europe Rallies on Earnings & PMIs (24.07.2026)

US OPEN: Nasdaq hits 1-month low! Geopolitics bring AI trade down!

Market Wrap: European Stocks Are Trying to Rebound as the Week Comes to an End💡

Alphabet shares are down 22% from their all-time high 🚩 Is Google ready to resume its bull run?

The content of this report has been created by XTB S.A., with its registered office in Warsaw, at Prosta 67, 00-838 Warsaw, Poland, (KRS number 0000217580) and supervised by Polish Supervision Authority ( No. DDM-M-4021-57-1/2005). This material is a marketing communication within the meaning of Art. 24 (3) of Directive 2014/65/EU of the European Parliament and of the Council of 15 May 2014 on markets in financial instruments and amending Directive 2002/92/EC and Directive 2011/61/EU (MiFID II). Marketing communication is not an investment recommendation or information recommending or suggesting an investment strategy within the meaning of Regulation (EU) No 596/2014 of the European Parliament and of the Council of 16 April 2014 on market abuse (market abuse regulation) and repealing Directive 2003/6/EC of the European Parliament and of the Council and Commission Directives 2003/124/EC, 2003/125/EC and 2004/72/EC and Commission Delegated Regulation (EU) 2016/958 of 9 March 2016 supplementing Regulation (EU) No 596/2014 of the European Parliament and of the Council with regard to regulatory technical standards for the technical arrangements for objective presentation of investment recommendations or other information recommending or suggesting an investment strategy and for disclosure of particular interests or indications of conflicts of interest or any other advice, including in the area of investment advisory, within the meaning of the Trading in Financial Instruments Act of 29 July 2005 (i.e. Journal of Laws 2019, item 875, as amended). The marketing communication is prepared with the highest diligence, objectivity, presents the facts known to the author on the date of preparation and is devoid of any evaluation elements. The marketing communication is prepared without considering the client’s needs, his individual financial situation and does not present any investment strategy in any way. The marketing communication does not constitute an offer of sale, offering, subscription, invitation to purchase, advertisement or promotion of any financial instruments. XTB S.A. is not liable for any client’s actions or omissions, in particular for the acquisition or disposal of financial instruments, undertaken on the basis of the information contained in this marketing communication. In the event that the marketing communication contains any information about any results regarding the financial instruments indicated therein, these do not constitute any guarantee or forecast regarding the future results.