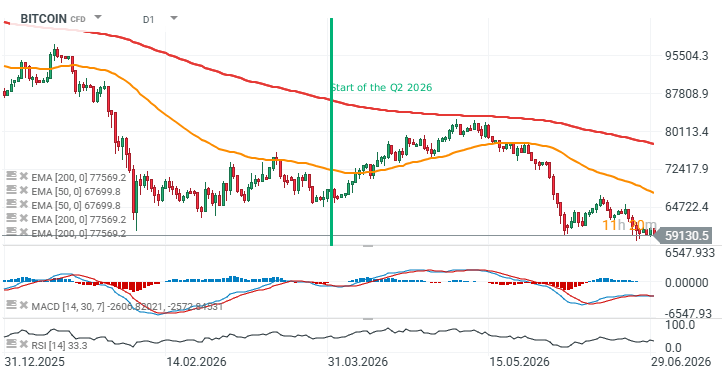

Bitcoin had a disastrous start to the year and an equally weak second quarter, during which the rally toward $81,000 completely faded. As a result, the cryptocurrency plunged to its lowest levels of 2026, while spot demand remains subdued, profit-taking continues to dominate, and derivatives positioning points to persistent caution among investors.

Key developments

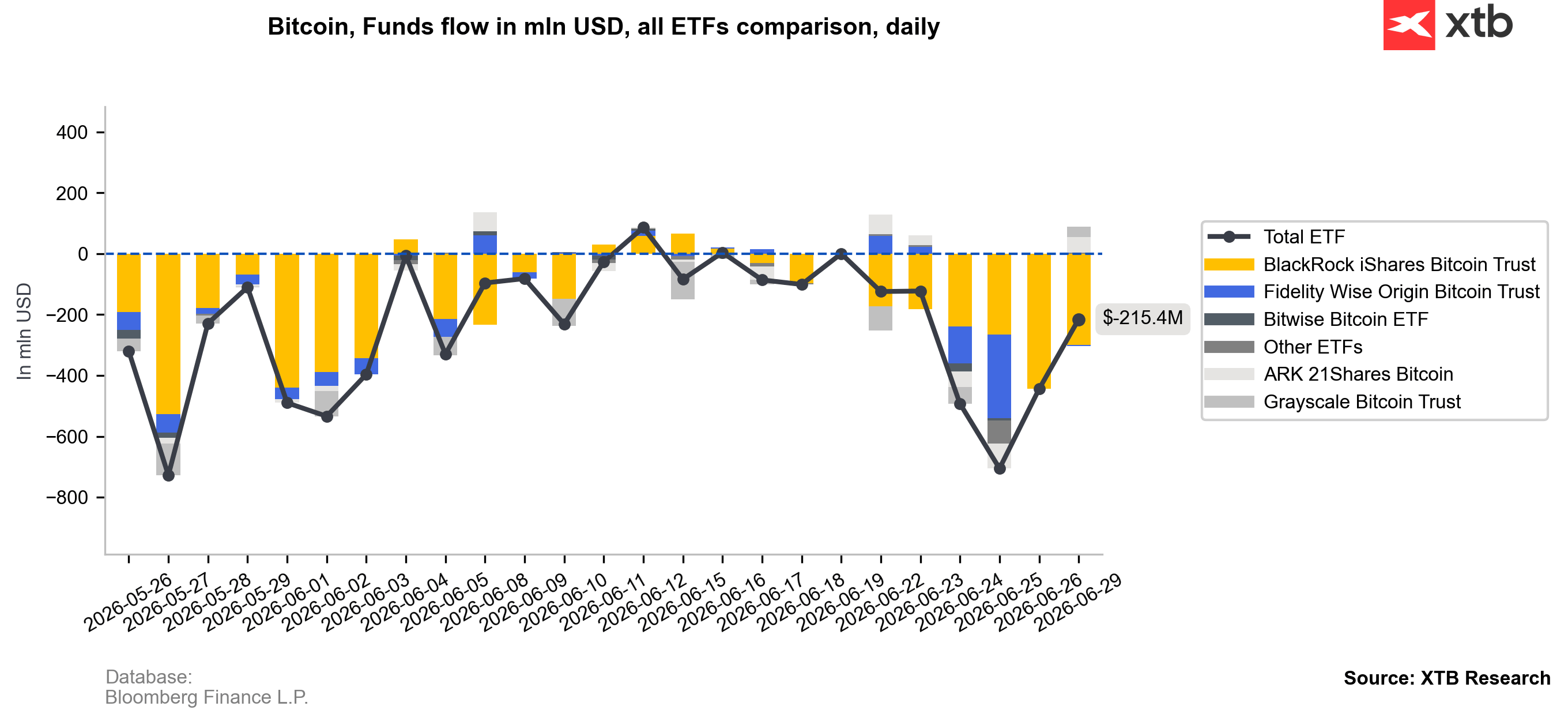

- In June, Bitcoin fell below $60,000 for the first time since 2024. The main drag has been persistent outflows from U.S. spot Bitcoin ETFs, which totaled an estimated $4.5–6 billion during the final weeks of the first half of the year.

- The weakness began early. In January, Bitcoin and Ethereum ETFs recorded nearly $1 billion in outflows in a single day, setting a negative tone for the year. Despite a strong rebound in March, when ETFs attracted $1.32 billion of inflows, spot Bitcoin ETFs still finished the first quarter with roughly $500 million in net outflows.

- Selling pressure intensified again in May and June. A six-day streak of more than $1.5 billion in ETF outflows reduced net inflows for 2026 to just around $536 million. At the same time, the ETF market became increasingly concentrated around BlackRock and Fidelity, which had previously attracted most of the inflows but also turned into net sellers in recent weeks.

- In June, Strategy sold a small portion of its Bitcoin holdings for the first time since 2022, weighing on sentiment surrounding the world's largest corporate Bitcoin holder.

- The decline in Bitcoin prices also hit the mining industry. For some miners, production costs exceeded the market price of Bitcoin, while the network's hashrate fell by around 5.8% at the beginning of 2026, highlighting mounting pressure across the mining sector.

- The narrative of Bitcoin as a hedge against U.S. dollar weakness lost momentum as markets priced in a more hawkish Federal Reserve, higher interest rates, and a rotation of capital away from cryptocurrencies toward AI and semiconductor stocks, as well as the highly anticipated SpaceX IPO.

- On the regulatory front, investors are still waiting for a breakthrough. Progress on the Clarity Act in the United States remains slow, limiting institutional appetite despite continued expansion of cryptocurrency services by major financial firms.

Bitcoin chart (D1 timeframe)

Source: xStation5

Source: XTB Research, Bloomberg Finance L.P.

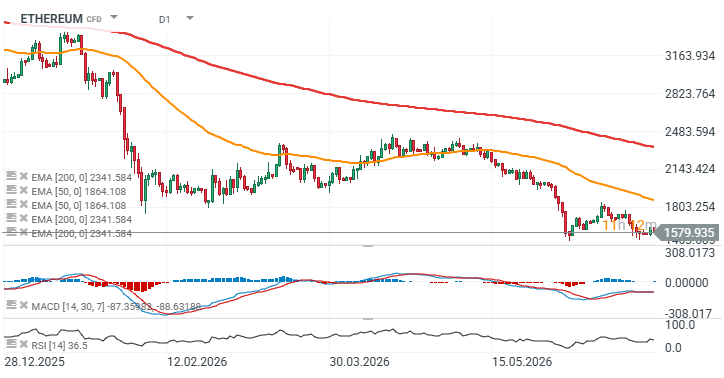

- Ethereum significantly underperformed Bitcoin during the first half of 2026, as investors favored Bitcoin ETFs while demand for ETH remained considerably weaker.

- Spot Ethereum ETFs continued to attract only modest institutional interest, with inflows remaining well below those seen in Bitcoin products despite periods of improving market sentiment.

- Ethereum staking reached another record high, with more than one-third of the total ETH supply locked in staking, reducing the amount of freely circulating coins.

- Layer-2 networks continued gaining traction, processing an increasing share of Ethereum transactions and helping lower fees on the main network.

- Decentralized finance (DeFi) activity remained resilient, although total value locked (TVL) stayed below previous cycle highs as investors remained cautious.

- Stablecoin usage on Ethereum continued to expand, reinforcing the network's position as the leading settlement layer for tokenized dollar transactions.

- Ethereum developers continued work on the Pectra upgrade, one of the network's most important upcoming protocol improvements, aimed at enhancing scalability, validator efficiency, and user experience.

- Despite improving on-chain fundamentals, ETH remained under pressure as higher U.S. interest rates and strong performance of AI-related equities continued to divert capital away from the broader cryptocurrency market.

Ethereum charts (D1 timeframe)

Source: xStation5

Daily Summary: China Shows Its Teeth on AI; The U.K. Sees a Government Revolution 🏛️

Market Wrap: Airlines Under Pressure, Europe Resists Expensive Oil

🛢️Brent crude retreats from $90

Is Another DeepSeek Moment Coming? Moonshot AI Increases Pressure on AI Giants

The content of this report has been created by XTB S.A., with its registered office in Warsaw, at Prosta 67, 00-838 Warsaw, Poland, (KRS number 0000217580) and supervised by Polish Supervision Authority ( No. DDM-M-4021-57-1/2005). This material is a marketing communication within the meaning of Art. 24 (3) of Directive 2014/65/EU of the European Parliament and of the Council of 15 May 2014 on markets in financial instruments and amending Directive 2002/92/EC and Directive 2011/61/EU (MiFID II). Marketing communication is not an investment recommendation or information recommending or suggesting an investment strategy within the meaning of Regulation (EU) No 596/2014 of the European Parliament and of the Council of 16 April 2014 on market abuse (market abuse regulation) and repealing Directive 2003/6/EC of the European Parliament and of the Council and Commission Directives 2003/124/EC, 2003/125/EC and 2004/72/EC and Commission Delegated Regulation (EU) 2016/958 of 9 March 2016 supplementing Regulation (EU) No 596/2014 of the European Parliament and of the Council with regard to regulatory technical standards for the technical arrangements for objective presentation of investment recommendations or other information recommending or suggesting an investment strategy and for disclosure of particular interests or indications of conflicts of interest or any other advice, including in the area of investment advisory, within the meaning of the Trading in Financial Instruments Act of 29 July 2005 (i.e. Journal of Laws 2019, item 875, as amended). The marketing communication is prepared with the highest diligence, objectivity, presents the facts known to the author on the date of preparation and is devoid of any evaluation elements. The marketing communication is prepared without considering the client’s needs, his individual financial situation and does not present any investment strategy in any way. The marketing communication does not constitute an offer of sale, offering, subscription, invitation to purchase, advertisement or promotion of any financial instruments. XTB S.A. is not liable for any client’s actions or omissions, in particular for the acquisition or disposal of financial instruments, undertaken on the basis of the information contained in this marketing communication. In the event that the marketing communication contains any information about any results regarding the financial instruments indicated therein, these do not constitute any guarantee or forecast regarding the future results.