Exactly one year ago, following the decline in Arabica coffee prices below 300 cents per pound, we could discuss the end of high prices in the coffee market. Although prices in stores and cafes remained high, the outlook regarding changing global fundamentals gave consumers hope that the situation would improve. Last October, we observed another peak near 440 cents per pound, but since then, the price dived to 250 cents per pound at the turn of May and June in anticipation of record harvests in Brazil. Now, however, the weather is once again dictating the market narrative, pushing coffee prices up to as much as 350 cents per pound, hitting nearly the highest levels this year. On July 6, the price of coffee recorded its largest daily increase since 2000, amounting to over 15%. Are we facing another wave of high prices in the coffee market and other agricultural commodities?

Weather Roller Coaster and the Specter of "Super El Niño"

The main director of the whole confusion is, as always, the weather, which can deal cards on agricultural markets in a ruthless way. In the key Brazilian region of Minas Gerais, responsible for a lion's share of global Arabica production, powerful June downpours appeared first. In the week ending June 28, rainfall was nearly 2000% higher than the historical norm, which completely prevented machinery from entering fields and severely worsened bean quality, delaying harvests to 52% (compared to 60% a year earlier and 55% against the 5-year average). As if that wasn't enough, there was a drastic turn in the other direction immediately after, with an absolute lack of rainfall (a clean 0 mm) at the beginning of July. Coffee crops really dislike variable weather, which is why such a 180-degree turn can cause harvest prospects for this and the next season to change drastically.

The price effect on exchanges was immediate and textbook:

- During the July 6 session, September Arabica contracts saw a spectacular one-day jump of nearly 18%, ending the session with a 15% increase, breaking the 350 cents per pound barrier for the first time since January. It was the largest single-day price movement since 2000.

- The cheaper and stronger coffee variety, Robusta, didn't stay behind, rising by 8% and crossing the 4100 USD per ton level.

It is worth emphasizing that the El Niño weather phenomenon affects the weather in Brazil in a mixed way, but has an unambiguous meaning for coffee production in Southeast Asia. Severe droughts cause Robusta production to clearly fall.

In response to changing weather prospects, investment funds began scrambling to cover short positions, reacting to the official formation of the El Niño weather anomaly in the Pacific. Meteorologists currently give a 67% chance for the arrival of a devastating version of "Super El Niño," which threatens the proper flowering of coffee trees.

Fertilizers, Labor Costs, and Empty Warehouses

If you are counting on distributors and cafe owners taking these hikes on their own shoulders, let's face the truth, as market fundamentals are ruthless to consumers:

- Certified Arabica stocks monitored by the ICE exchange have shrunk to their lowest level in over 2 years. There is simply a shortage of physical goods on the market. Although USDA data shows a surplus for several years, global stocks are constantly decreasing.

- In Vietnam (a key Robusta producer), farmers are fighting early drought and drastic annual cost pressure. Fertilizer and fuel prices there have jumped by 30% year-on-year, and labor costs by another 33%.

- Historical analyses from recent years show that August is often one of the best months for coffee prices in the year, and the growth potential based on the 5-year average can persist until the end of the year.

The Whole Menu is Getting More Expensive, meaning not just coffee

To complete the bleak picture of the market, it's worth looking at other soft commodities, because coffee is not an isolated island of high prices. Sweet-tooth lovers must also prepare their wallets. Cocoa, which after a spectacular price rise in 2024 saw a deep crash in early April 2026 to the level of 3000 USD per ton (caused by massive demand destruction and modification of recipes by manufacturers), suddenly shot up at the turn of June and July, noting the highest levels since January. Exactly during the same hot session of July 6, the September cocoa contract in New York rose by about 13–14%, reaching a 6-month peak at the level of 5700 USD per ton. The reason? Almost identical: excessive rains in West Africa, which flooded transport routes and caused tree disease epidemics, and additionally had a negative impact on previously unsold cocoa, which now may not be suitable for any deliveries.

It seems that after a momentary spring break, consumers must prepare for the return of high prices. The combination of unpredictable weather anomalies associated with El Niño, relentless pressure on production costs (expensive fertilizers, fuels, labor), and drastically shrinking stocks means that our daily moment of pleasure with a cup of our favorite drink in the near future may turn out to be a luxury good. It's time to get used to the thought that we will have to pay much more for our morning awakening in the coming months.

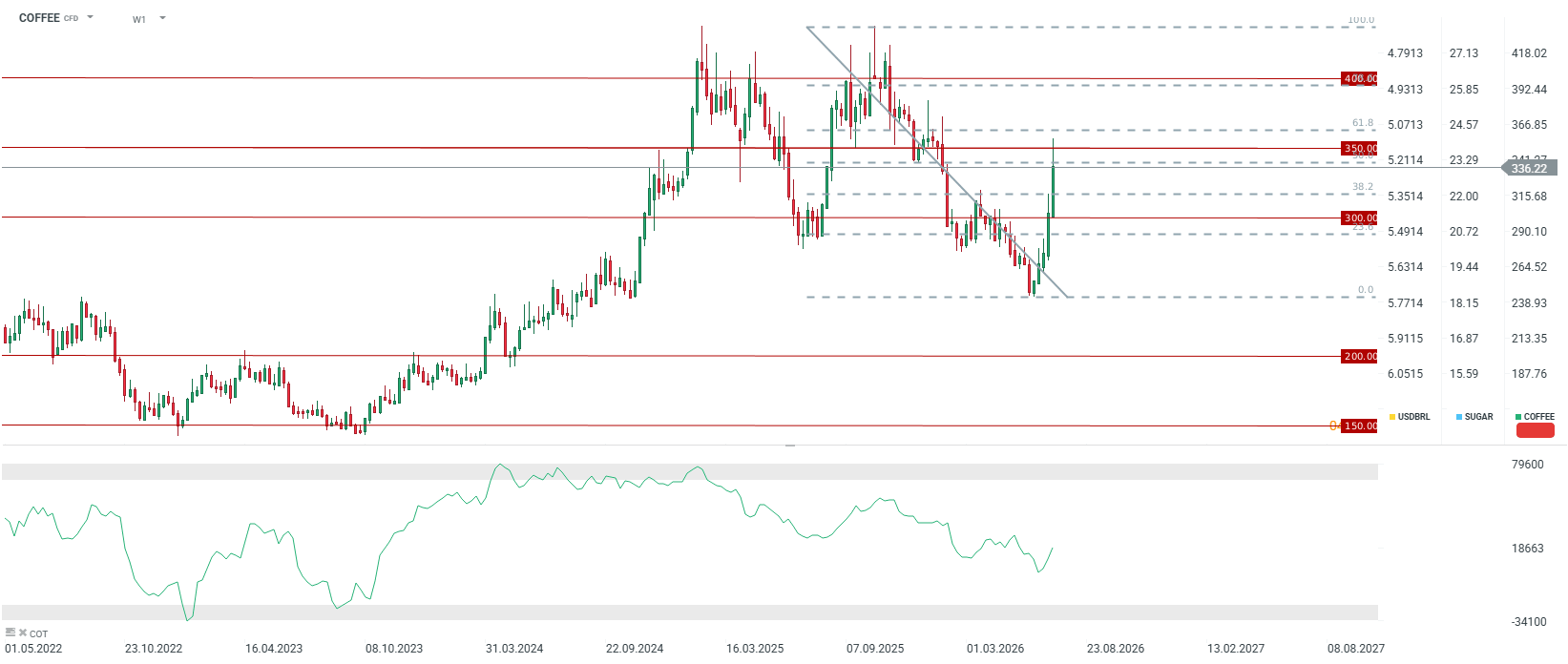

The chart presents the weekly behavior of coffee prices.

In just 5 weeks, coffee recovered almost 8 months of losses. Source: xStation5

In just 5 weeks, coffee recovered almost 8 months of losses. Source: xStation5

Daily Summary: Chip War Weighs on Wall Street as Oil Plunges After US–Iran Ceasefire ⭐

Nasdaq-100 under pressure after chip sell-off

China Is Building Its Own Chip-Making Machines. ASML Under Pressure as the Technology War Enters a New Phase

US Open: Wall Street Rebounds After US Iran Ceasefire

The content of this report has been created by XTB S.A., with its registered office in Warsaw, at Prosta 67, 00-838 Warsaw, Poland, (KRS number 0000217580) and supervised by Polish Supervision Authority ( No. DDM-M-4021-57-1/2005). This material is a marketing communication within the meaning of Art. 24 (3) of Directive 2014/65/EU of the European Parliament and of the Council of 15 May 2014 on markets in financial instruments and amending Directive 2002/92/EC and Directive 2011/61/EU (MiFID II). Marketing communication is not an investment recommendation or information recommending or suggesting an investment strategy within the meaning of Regulation (EU) No 596/2014 of the European Parliament and of the Council of 16 April 2014 on market abuse (market abuse regulation) and repealing Directive 2003/6/EC of the European Parliament and of the Council and Commission Directives 2003/124/EC, 2003/125/EC and 2004/72/EC and Commission Delegated Regulation (EU) 2016/958 of 9 March 2016 supplementing Regulation (EU) No 596/2014 of the European Parliament and of the Council with regard to regulatory technical standards for the technical arrangements for objective presentation of investment recommendations or other information recommending or suggesting an investment strategy and for disclosure of particular interests or indications of conflicts of interest or any other advice, including in the area of investment advisory, within the meaning of the Trading in Financial Instruments Act of 29 July 2005 (i.e. Journal of Laws 2019, item 875, as amended). The marketing communication is prepared with the highest diligence, objectivity, presents the facts known to the author on the date of preparation and is devoid of any evaluation elements. The marketing communication is prepared without considering the client’s needs, his individual financial situation and does not present any investment strategy in any way. The marketing communication does not constitute an offer of sale, offering, subscription, invitation to purchase, advertisement or promotion of any financial instruments. XTB S.A. is not liable for any client’s actions or omissions, in particular for the acquisition or disposal of financial instruments, undertaken on the basis of the information contained in this marketing communication. In the event that the marketing communication contains any information about any results regarding the financial instruments indicated therein, these do not constitute any guarantee or forecast regarding the future results.