16:30 - EIA, change in U.S. oil inventories:

- Crude oil inventories: -8.26M (Expected: -3M; Previous: -7.23M)

- Gasoline inventories: -0.91M (Expected: -1.4M; Previous: +0.19M)

- Distillate inventories: +0.95M (Expected: -0.2M; Previous: -0.2M)

The release shows short-term growth impulse for oil. The key signal is the combination of a large drop in crude imports and very high refinery runs, which results in sharp decline in commercial inventories.

The U.S. reserve buffer is becoming critical at a time when the market is already pricing in the best possible scenarios regarding the Iran-U.S. conflict.

The sharp inventory draw is a combination of a steep fall in crude imports, down by 754k barrels per day, and strong refinery utilization: crude runs rose to 17.2M barrels per day, and refinery utilization reached 96.7%.

U.S. commercial crude inventories, excluding the Strategic Petroleum Reserve, fell by 8.3M barrels to 418.2M barrels, already about 6% below the five-year average.

- Gasoline inventories fell by 0.9M barrels and are also about 6% below the five-year average.

- Distillate inventories rose by 1.0M barrels, but remain as much as 13% below the five-year average.

- Total crude inventories including the SPR fell by 17.2M barrels, with the strategic reserve alone down by 8.9M barrels. Although the decline is large, most of it is not “market-driven.”

- The decline in commercial crude inventories is visible in two key regions: the Gulf Coast (down about 4.8M barrels) and the Midwest (down about 4.5M barrels).

The EIA also assumes that the Strait of Hormuz remains effectively closed in the short term, and tanker traffic only gradually returns from Q3 2026, while fuller normalization of production and flows may take until 2027. The agency also estimated very large global inventory declines in Q2 and Q3 2026, and a drop in OECD inventories to the lowest levels since 2003.

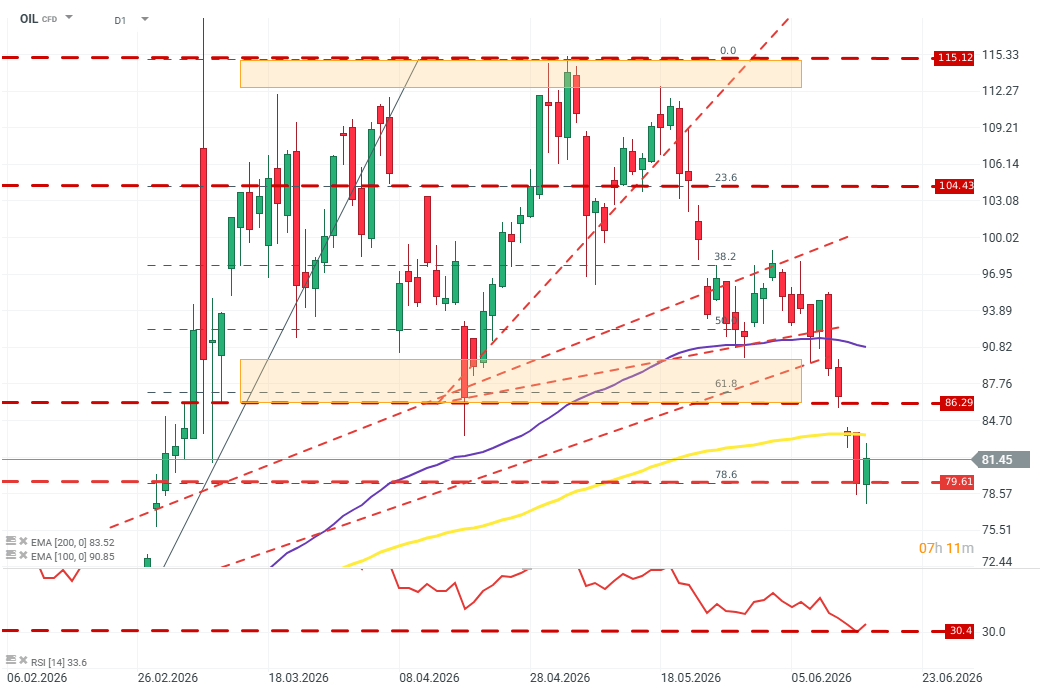

OIL (D1)

The RSI on oil contracts is currently in extreme overbought territory (around 30). Price bounced off the 78.6% Fibonacci level and may attempt to move back above the 200 EMA. If sellers shift into consolidation around these levels, the next target could be around $87. Source: xStation5.

Daily Summary: Wall Street Regains Ground; Another Intervention in the Yen Market❓

Three Markets to Watch Next Week (July 31, 2026)

Market Wrap: European equities at 3-week highs! Apple dips in US premarket!

Euro Area core inflation above estiamtes! EURUSD under key resistance!

The content of this report has been created by XTB S.A., with its registered office in Warsaw, at Prosta 67, 00-838 Warsaw, Poland, (KRS number 0000217580) and supervised by Polish Supervision Authority ( No. DDM-M-4021-57-1/2005). This material is a marketing communication within the meaning of Art. 24 (3) of Directive 2014/65/EU of the European Parliament and of the Council of 15 May 2014 on markets in financial instruments and amending Directive 2002/92/EC and Directive 2011/61/EU (MiFID II). Marketing communication is not an investment recommendation or information recommending or suggesting an investment strategy within the meaning of Regulation (EU) No 596/2014 of the European Parliament and of the Council of 16 April 2014 on market abuse (market abuse regulation) and repealing Directive 2003/6/EC of the European Parliament and of the Council and Commission Directives 2003/124/EC, 2003/125/EC and 2004/72/EC and Commission Delegated Regulation (EU) 2016/958 of 9 March 2016 supplementing Regulation (EU) No 596/2014 of the European Parliament and of the Council with regard to regulatory technical standards for the technical arrangements for objective presentation of investment recommendations or other information recommending or suggesting an investment strategy and for disclosure of particular interests or indications of conflicts of interest or any other advice, including in the area of investment advisory, within the meaning of the Trading in Financial Instruments Act of 29 July 2005 (i.e. Journal of Laws 2019, item 875, as amended). The marketing communication is prepared with the highest diligence, objectivity, presents the facts known to the author on the date of preparation and is devoid of any evaluation elements. The marketing communication is prepared without considering the client’s needs, his individual financial situation and does not present any investment strategy in any way. The marketing communication does not constitute an offer of sale, offering, subscription, invitation to purchase, advertisement or promotion of any financial instruments. XTB S.A. is not liable for any client’s actions or omissions, in particular for the acquisition or disposal of financial instruments, undertaken on the basis of the information contained in this marketing communication. In the event that the marketing communication contains any information about any results regarding the financial instruments indicated therein, these do not constitute any guarantee or forecast regarding the future results.