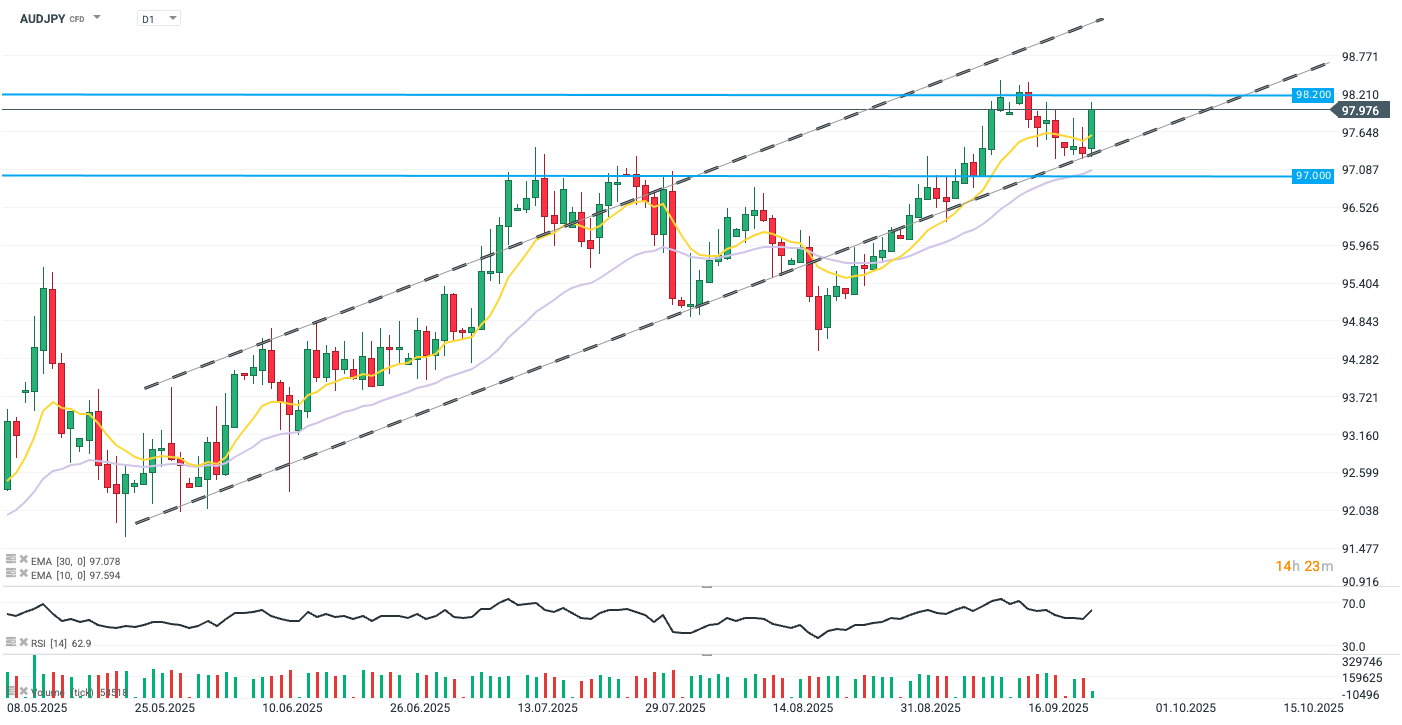

AUDJPY rebounds bullishly by 0.7%, with yen giving up the most against the Australian dollar among all G10 currencies. Dynamic appreciation of AUDJPY has been motivated by trend-supporting data from both economies, particularly higher monthly inflation reading in Australia that caps expectations for further monetary easing in the country.

AUDUSD rebounds from the lower bound of the well pronounced increasing channel. Today’s gains erase the recent correction which pushed the pair off of its highest levels since the start of 2025. Source: xStation5

What is shaping AUDJPY today?

-

Australia’s consumer price index rose 3.0% in August from a year earlier, up from 2.8% in July and slightly above forecasts. The increase was partly due to base effects but highlighted persistent pressures, particularly in services such as restaurant meals, takeaway food, andf audiovisual services. Core inflation was mixed: the trimmed mean eased to 2.6%, while the measure excluding volatile items climbed to 3.4%. Housing costs also ticked higher, suggesting upside risks for third-quarter inflation after months of moderation.

-

Markets quickly adjusted rate expectations after the inflation surprise, with major banks and financial institutions abandoning calls for a November cut. Odds of a move dropped to 50% from nearly 70% before the data, with investors now expecting rates to stay at 3.6% until at least May 2026. Analysts flagged the labour market as the key variable for policy direction, though its volatility makes a near-term cut less likely. The RBA continues to emphasize quarterly CPI as its preferred guide.

-

On the JPY side, Japan’s private sector activity is visibly slowing, as indicated by September’s flash PMIs. The composite index hit the lowest in four months, with manufacturing falling more than expected from 49.7 to 48.4, the lowest since March, due to sharp order declines and weaker exports. Services’ expansion helped to offset the downturn in manufacturing with solid activity and sales, reflecting robust domestic demand. Cost pressures persisted, selling prices rose, and employment growth slowed to a two-year low.

Cocoa loses 5% amid rising inventories on ICE

Oil gains 3% amid US - Iran escalation and supply disruption on the Black Sea

🔼 Gold gains 1.7%

🛢️Brent Crude Oil Tests $95 per Barrel

The content of this report has been created by XTB S.A., with its registered office in Warsaw, at Prosta 67, 00-838 Warsaw, Poland, (KRS number 0000217580) and supervised by Polish Supervision Authority ( No. DDM-M-4021-57-1/2005). This material is a marketing communication within the meaning of Art. 24 (3) of Directive 2014/65/EU of the European Parliament and of the Council of 15 May 2014 on markets in financial instruments and amending Directive 2002/92/EC and Directive 2011/61/EU (MiFID II). Marketing communication is not an investment recommendation or information recommending or suggesting an investment strategy within the meaning of Regulation (EU) No 596/2014 of the European Parliament and of the Council of 16 April 2014 on market abuse (market abuse regulation) and repealing Directive 2003/6/EC of the European Parliament and of the Council and Commission Directives 2003/124/EC, 2003/125/EC and 2004/72/EC and Commission Delegated Regulation (EU) 2016/958 of 9 March 2016 supplementing Regulation (EU) No 596/2014 of the European Parliament and of the Council with regard to regulatory technical standards for the technical arrangements for objective presentation of investment recommendations or other information recommending or suggesting an investment strategy and for disclosure of particular interests or indications of conflicts of interest or any other advice, including in the area of investment advisory, within the meaning of the Trading in Financial Instruments Act of 29 July 2005 (i.e. Journal of Laws 2019, item 875, as amended). The marketing communication is prepared with the highest diligence, objectivity, presents the facts known to the author on the date of preparation and is devoid of any evaluation elements. The marketing communication is prepared without considering the client’s needs, his individual financial situation and does not present any investment strategy in any way. The marketing communication does not constitute an offer of sale, offering, subscription, invitation to purchase, advertisement or promotion of any financial instruments. XTB S.A. is not liable for any client’s actions or omissions, in particular for the acquisition or disposal of financial instruments, undertaken on the basis of the information contained in this marketing communication. In the event that the marketing communication contains any information about any results regarding the financial instruments indicated therein, these do not constitute any guarantee or forecast regarding the future results.