The pound is recording sharp losses against all G10 currencies (GBPUSD: -0.2%, GBPJPY: -0.7%, EURGBP: +0.25%) in the aftermath of a UK labor report that underscored a progressive softening in the jobs market. This surprise uptick in unemployment suggests that the Bank of England’s recent dovish hold may, in fact, be already falling behind the curve.

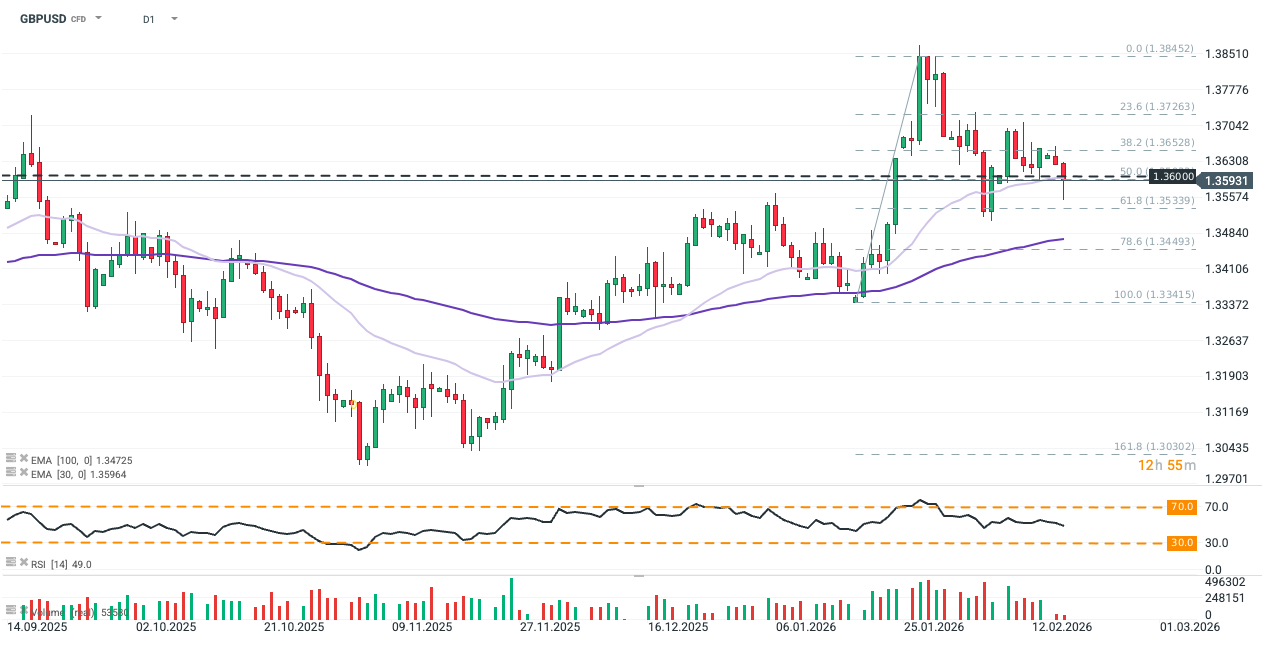

GBPUSD dropped sharply below the key support level at 1.36000 following the labour data release. Dip buyers limited the decline by brining the pair back to the 50.0 Fibonacci retracement level coinciding with 30-day expontential moving average (EMA30; light purple), although the price seems reluctant to recover above the above-mentioned key level. Source: xStation5

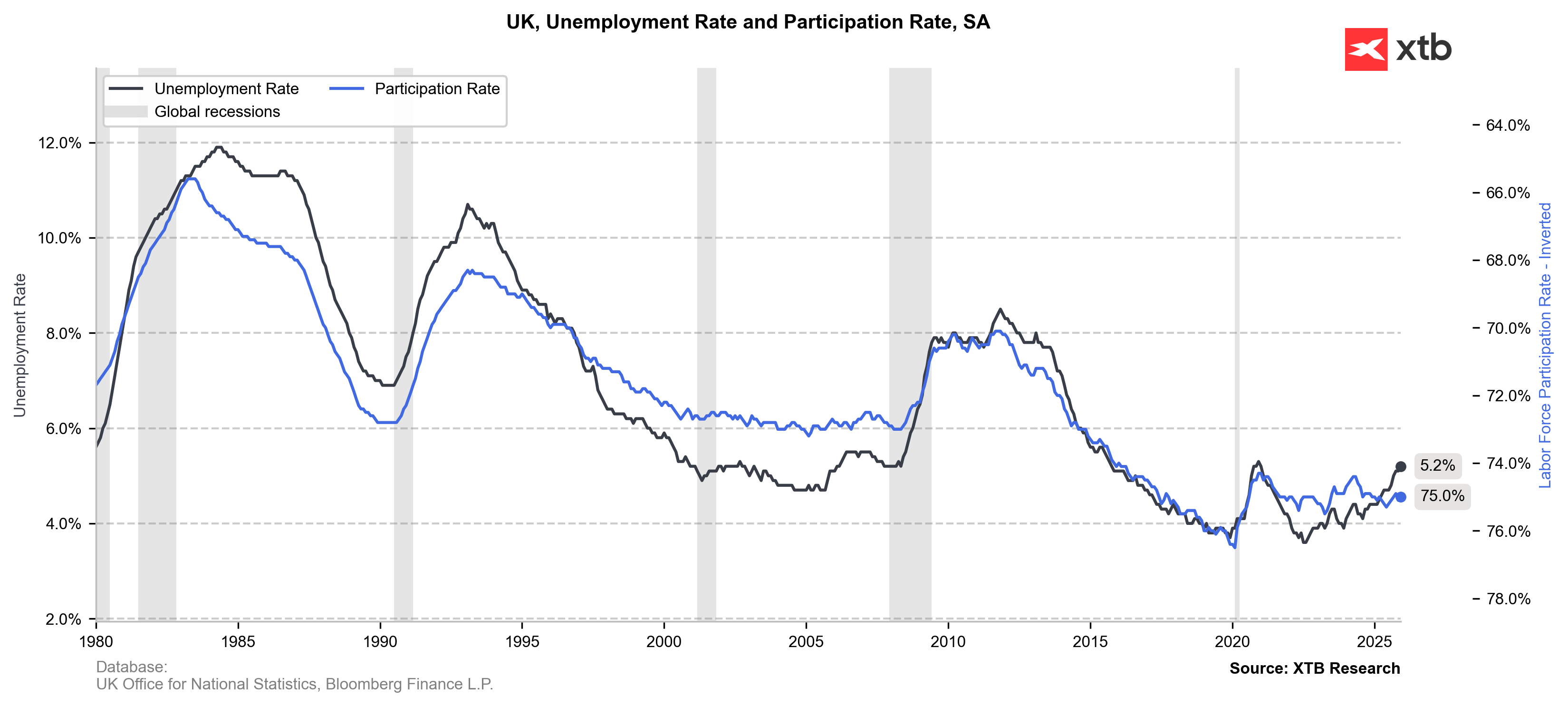

Unemployment Climbs to 5.2%

After holding steady at 5.1% for two months, the UK’s unemployment rate climbed to 5.2% in December (exceeding the Bloomberg consensus of 5.1%). This marks a nearly five-year high, edging closer to the 5.3% peak seen during the pandemic.

Concurrently, average earnings growth cooled from 4.5% to 4.2%, while stagnant vacancy figures confirmed mounting slack in the labor market — highlighting a distinct lack of hiring momentum as layoffs persist. Particularly alarming are the early January estimates for year-on-year employment change, which indicate a loss of over 134,000 jobs over the past year (-11k m/m), despite a backdrop of previously persistent inflation.

UK unemployment rate reached its highest since COVID. Source: XTB Research

BoE Outlook: Acceleration Toward Easing

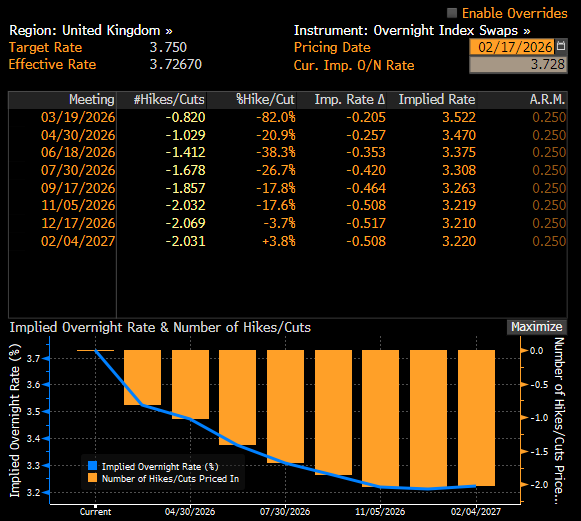

This data has accelerated bets on Bank of England (BoE) rate cuts in the coming months. Although the recent decision to hold rates at 3.75% was already perceived as dovish due to the narrow 5-4 MPC vote split, the deteriorating labor outlook will likely force a re-evaluation of the timing for easing. Swap markets are now pricing in an 82% probability of a March cut, with two total reductions anticipated by the end of 2026.

However, it will likely take months for businesses to feel the benefits of lower rates and regain the confidence to resume hiring, especially given the headwinds of a higher minimum wage. Additionally, recent payroll tax hikes are expected to dampen consumer confidence and spending, stifling the economic activity required for firms to break out of current stagnation. This suggests that without more aggressive monetary easing, the UK remains at risk of being trapped in a low-growth environment, notwithstanding recent marginal gains in labor productivity.

Source: Bloomberg Finance LP.

Economic Calendar: RBA Holds Rates, Markets Await US Housing Data

Morning Wrap: Trump Sets Conditions for Iran. Oil Rises as Hopes for a Quick Reopening of the Strait of Hormuz Fade

Daily Summary: Failure of negotiations in the gulf, oil and gas prices soar

FX Weekly: Yen Returns to Losses, Dollar Under Pressure (10.08.2026)

The content of this report has been created by XTB S.A., with its registered office in Warsaw, at Prosta 67, 00-838 Warsaw, Poland, (KRS number 0000217580) and supervised by Polish Supervision Authority ( No. DDM-M-4021-57-1/2005). This material is a marketing communication within the meaning of Art. 24 (3) of Directive 2014/65/EU of the European Parliament and of the Council of 15 May 2014 on markets in financial instruments and amending Directive 2002/92/EC and Directive 2011/61/EU (MiFID II). Marketing communication is not an investment recommendation or information recommending or suggesting an investment strategy within the meaning of Regulation (EU) No 596/2014 of the European Parliament and of the Council of 16 April 2014 on market abuse (market abuse regulation) and repealing Directive 2003/6/EC of the European Parliament and of the Council and Commission Directives 2003/124/EC, 2003/125/EC and 2004/72/EC and Commission Delegated Regulation (EU) 2016/958 of 9 March 2016 supplementing Regulation (EU) No 596/2014 of the European Parliament and of the Council with regard to regulatory technical standards for the technical arrangements for objective presentation of investment recommendations or other information recommending or suggesting an investment strategy and for disclosure of particular interests or indications of conflicts of interest or any other advice, including in the area of investment advisory, within the meaning of the Trading in Financial Instruments Act of 29 July 2005 (i.e. Journal of Laws 2019, item 875, as amended). The marketing communication is prepared with the highest diligence, objectivity, presents the facts known to the author on the date of preparation and is devoid of any evaluation elements. The marketing communication is prepared without considering the client’s needs, his individual financial situation and does not present any investment strategy in any way. The marketing communication does not constitute an offer of sale, offering, subscription, invitation to purchase, advertisement or promotion of any financial instruments. XTB S.A. is not liable for any client’s actions or omissions, in particular for the acquisition or disposal of financial instruments, undertaken on the basis of the information contained in this marketing communication. In the event that the marketing communication contains any information about any results regarding the financial instruments indicated therein, these do not constitute any guarantee or forecast regarding the future results.