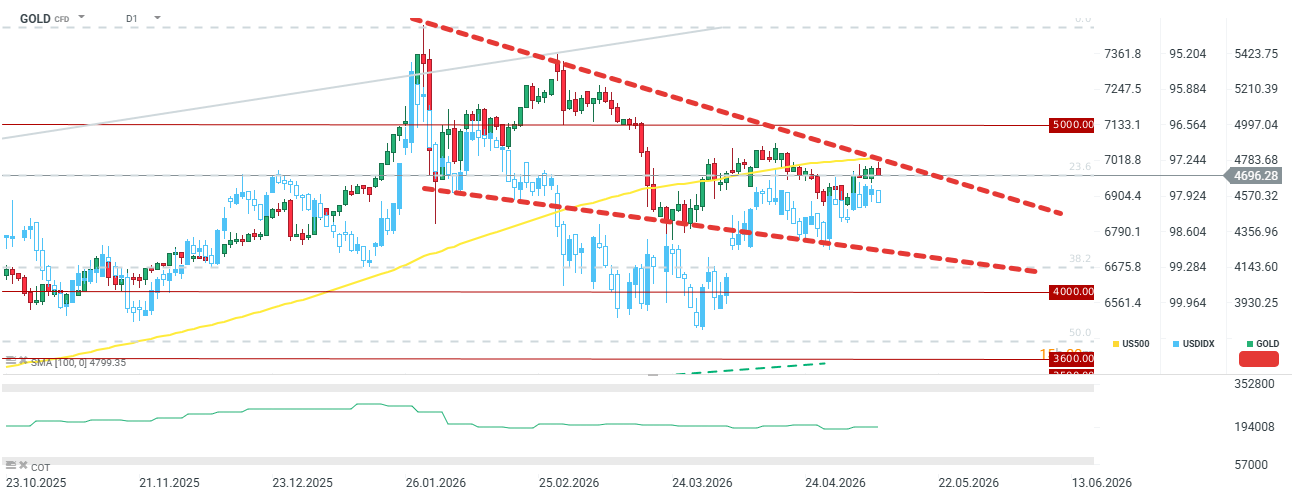

- Gold is dropping below $4,700 per ounce

- The key macro report for the gold and the dollar is the US CPI release

- Recent data from the World Gold Council for the Q1 2026 was supporting for the gold but with some minor drawbacks

- Gold is dropping below $4,700 per ounce

- The key macro report for the gold and the dollar is the US CPI release

- Recent data from the World Gold Council for the Q1 2026 was supporting for the gold but with some minor drawbacks

Gold prices are shedding approximately 0.5% during Tuesday's session, following several days of stagnation and a failure to decisively break above the $4,700 per ounce level. Notably, the price remains below the 100-period moving average and the downward trendline.

We are observing a slightly stronger dollar today, driven not only by expectations of higher inflation but also by the geopolitical impasse in the Middle East. Reports suggest Trump is considering a resumption of hostilities in Iran following the rejection of the latest peace plan.

Today’s CPI inflation is expected to rise to 3.7% y/y, while core inflation is projected to reach 2.7% y/y. If inflation proves to be "sticky," pressure on the central bank will mount, which could weigh on precious metals in the near term. On the other hand, it is worth noting that silver broke out of its resistance zone yesterday, accompanied by a sharp rebound in copper prices.

The fundamental outlook for gold remains solid: demand is being driven by central bank purchases and retail investors buying physical gold. However, ETF demand saw a significant drop in Q1, and we have yet to see a meaningful recovery, even with Wall Street hitting record highs. Gold requires a clear improvement in the Middle East situation and certainty that inflation is merely transitory and will not trigger a fresh wave of interest rate hikes.

Key Data: World Gold Council Report

- Total demand (including OTC): Total gold demand increased by 2% y/y to 1,230 tonnes. Conversely, excluding OTC, there was a decrease of 9% y/y and 10% q/q.

- Record central bank purchases: Central banks purchased 243 tonnes of gold.

- Jewelry consumption: Jewelry demand fell sharply by nearly 1/4 on both a yearly and quarterly basis, dropping to 335 tonnes.

- Gold supply: Total supply increased minimally year-on-year, reaching 1,230 tonnes; however, this represents a significant decline compared to the previous two quarters, which may suggest a potential ongoing deficit.

Daily Summary: Wall Street Regains Ground; Another Intervention in the Yen Market❓

Three Markets to Watch Next Week (July 31, 2026)

Market Wrap: European equities at 3-week highs! Apple dips in US premarket!

Euro Area core inflation above estiamtes! EURUSD under key resistance!

The content of this report has been created by XTB S.A., with its registered office in Warsaw, at Prosta 67, 00-838 Warsaw, Poland, (KRS number 0000217580) and supervised by Polish Supervision Authority ( No. DDM-M-4021-57-1/2005). This material is a marketing communication within the meaning of Art. 24 (3) of Directive 2014/65/EU of the European Parliament and of the Council of 15 May 2014 on markets in financial instruments and amending Directive 2002/92/EC and Directive 2011/61/EU (MiFID II). Marketing communication is not an investment recommendation or information recommending or suggesting an investment strategy within the meaning of Regulation (EU) No 596/2014 of the European Parliament and of the Council of 16 April 2014 on market abuse (market abuse regulation) and repealing Directive 2003/6/EC of the European Parliament and of the Council and Commission Directives 2003/124/EC, 2003/125/EC and 2004/72/EC and Commission Delegated Regulation (EU) 2016/958 of 9 March 2016 supplementing Regulation (EU) No 596/2014 of the European Parliament and of the Council with regard to regulatory technical standards for the technical arrangements for objective presentation of investment recommendations or other information recommending or suggesting an investment strategy and for disclosure of particular interests or indications of conflicts of interest or any other advice, including in the area of investment advisory, within the meaning of the Trading in Financial Instruments Act of 29 July 2005 (i.e. Journal of Laws 2019, item 875, as amended). The marketing communication is prepared with the highest diligence, objectivity, presents the facts known to the author on the date of preparation and is devoid of any evaluation elements. The marketing communication is prepared without considering the client’s needs, his individual financial situation and does not present any investment strategy in any way. The marketing communication does not constitute an offer of sale, offering, subscription, invitation to purchase, advertisement or promotion of any financial instruments. XTB S.A. is not liable for any client’s actions or omissions, in particular for the acquisition or disposal of financial instruments, undertaken on the basis of the information contained in this marketing communication. In the event that the marketing communication contains any information about any results regarding the financial instruments indicated therein, these do not constitute any guarantee or forecast regarding the future results.