While market attention is often focused on large declines in index futures, primarily following the massive drop of SpaceX during yesterday's session, an equally dynamic sell-off is also taking place in the precious metals market. Gold is down 1.7% and is already close to $4,100 per ounce, while silver is down nearly 4% and is close to the $62 per ounce level.

Since reaching a record level around $5,600 at the end of January, gold has already lost about 5% since the beginning of the year, and in the current quarter alone, it has recorded a decline of almost 12%, wiping out all gains from this year. Concerns about persistent inflation have effectively overshadowed the temporary optimism associated with peace negotiations between the US and Iran, which have currently lowered the price of Brent crude oil below $78.

Inflationary pressure and the hawkish Fed

- Conflict in the Middle East: The conflict, which has been ongoing for almost four months, has caused an increase in consumer and energy prices, fueling concerns about inflation becoming entrenched.

- Prospect of higher rates: Rising prices increase the likelihood that central banks will decide to tighten monetary policy further. This is a direct inhibiting factor for gold, which, unlike bonds, does not pay interest.

- Hawkish tone of policymakers: The head of the Chicago Fed, Austan Goolsbee, expressed deep concern about inflation, which remains clearly above target and is heading in the wrong direction. The atmosphere is also being heated up by the new head of the Fed, Kevin Warsh, who adopted hawkish rhetoric and declared an absolute fight to restore price stability.

- Strong US dollar: Hawkish market expectations for interest rates, combined with resilient macro data from the US, have significantly strengthened the dollar. EURUSD fell to around 1.14

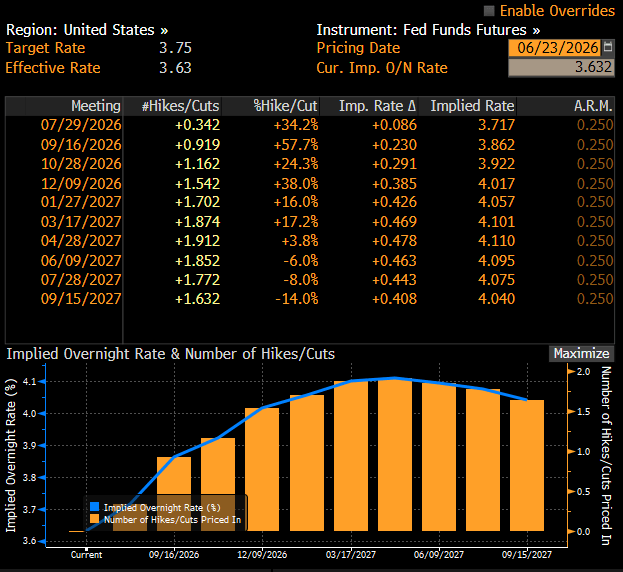

The market is pricing in a strong chance of a rate hike as early as September, although this will be difficult due to the upcoming midterm elections and the review of the entire Fed's operation, which is to be summarised by working groups appointed by Warsh at the end of this year. Source: Bloomberg Finance LP

The market is pricing in a strong chance of a rate hike as early as September, although this will be difficult due to the upcoming midterm elections and the review of the entire Fed's operation, which is to be summarised by working groups appointed by Warsh at the end of this year. Source: Bloomberg Finance LP

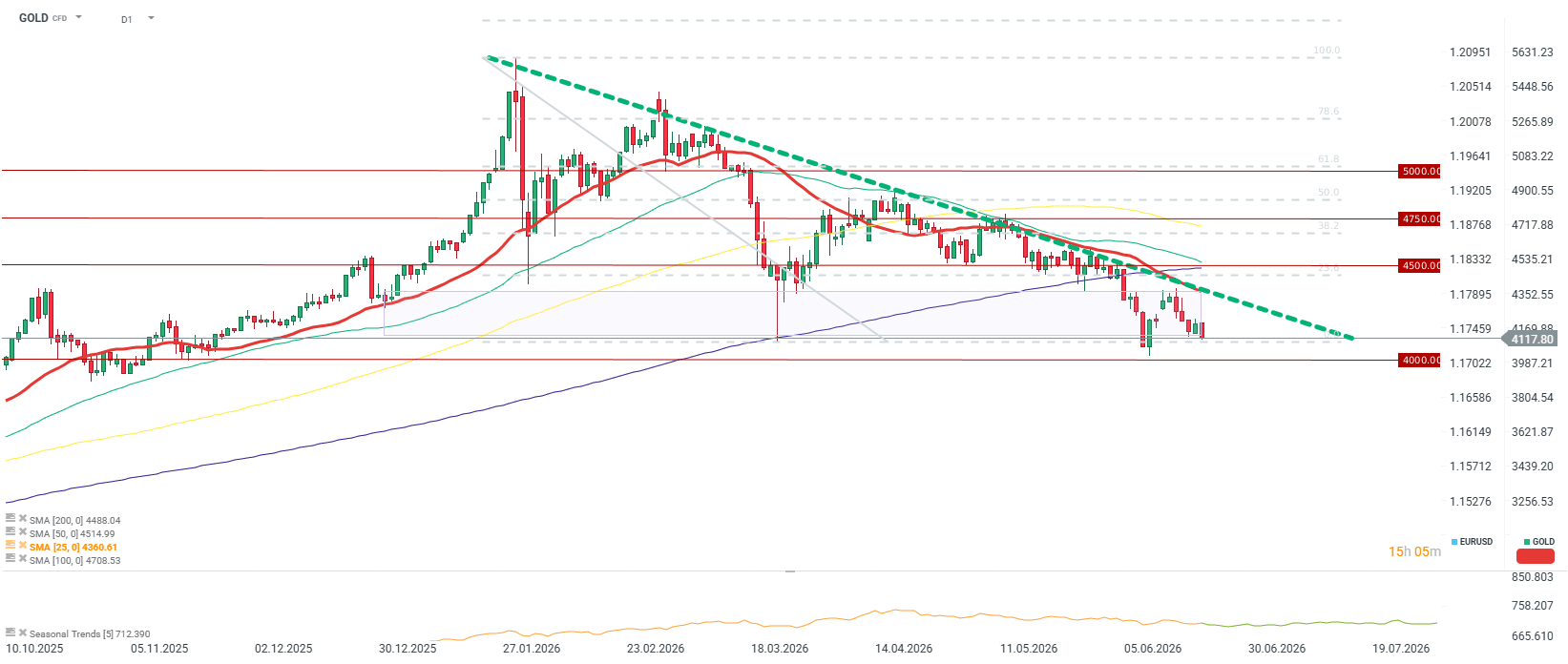

Technical situation and capital outflow

- Below key moving averages: The technical picture of the market has clearly deteriorated. Gold prices have permanently slipped below four key moving averages: 25, 50, 100, and 200-session. The 25-period average, which coincides with the falling trend line, may currently constitute short-term resistance.

- Lack of fund support and imports: Traditional sources of investment demand remain inactive. Continuous capital outflows and sales of units by gold-backed ETFs are visible. At the same time, local prices in China are traded at a discount compared to the Comex exchange, which suggests that local imports will not support the market in the near future.

- The only strong pillar: The only stable element of the puzzle remains the high demand from central banks, which is forecast to continue for a longer time.

Drastic forecast cuts by financial institutions

In light of the change in expectations regarding interest rates in the US, key investment banks decided to drastically revise their models:

- Deutsche Bank lowered its gold price forecasts by more than 1/5. Analysts estimate the price in the third quarter at $4,300 and $4,800 in the fourth quarter. The bank warns that if the Fed implements a scenario of 3-4 subsequent rate hikes, gold could fall to as low as $3,800. However, the market is currently pricing in less than 2 hikes.

- Goldman Sachs cut its year-end forecast by $500, setting a new target of $4,900 per ounce. This change results from the assumption that the US central bank will not make a single rate cut this year.

Morning Wrap: USA Halts Strikes – Oil Down, Stocks Up (03.08.2026)

Daily Summary: Wall Street Regains Ground; Another Intervention in the Yen Market❓

Three Markets to Watch Next Week (July 31, 2026)

Market Wrap: European equities at 3-week highs! Apple dips in US premarket!

The content of this report has been created by XTB S.A., with its registered office in Warsaw, at Prosta 67, 00-838 Warsaw, Poland, (KRS number 0000217580) and supervised by Polish Supervision Authority ( No. DDM-M-4021-57-1/2005). This material is a marketing communication within the meaning of Art. 24 (3) of Directive 2014/65/EU of the European Parliament and of the Council of 15 May 2014 on markets in financial instruments and amending Directive 2002/92/EC and Directive 2011/61/EU (MiFID II). Marketing communication is not an investment recommendation or information recommending or suggesting an investment strategy within the meaning of Regulation (EU) No 596/2014 of the European Parliament and of the Council of 16 April 2014 on market abuse (market abuse regulation) and repealing Directive 2003/6/EC of the European Parliament and of the Council and Commission Directives 2003/124/EC, 2003/125/EC and 2004/72/EC and Commission Delegated Regulation (EU) 2016/958 of 9 March 2016 supplementing Regulation (EU) No 596/2014 of the European Parliament and of the Council with regard to regulatory technical standards for the technical arrangements for objective presentation of investment recommendations or other information recommending or suggesting an investment strategy and for disclosure of particular interests or indications of conflicts of interest or any other advice, including in the area of investment advisory, within the meaning of the Trading in Financial Instruments Act of 29 July 2005 (i.e. Journal of Laws 2019, item 875, as amended). The marketing communication is prepared with the highest diligence, objectivity, presents the facts known to the author on the date of preparation and is devoid of any evaluation elements. The marketing communication is prepared without considering the client’s needs, his individual financial situation and does not present any investment strategy in any way. The marketing communication does not constitute an offer of sale, offering, subscription, invitation to purchase, advertisement or promotion of any financial instruments. XTB S.A. is not liable for any client’s actions or omissions, in particular for the acquisition or disposal of financial instruments, undertaken on the basis of the information contained in this marketing communication. In the event that the marketing communication contains any information about any results regarding the financial instruments indicated therein, these do not constitute any guarantee or forecast regarding the future results.