US500, the US S&P 500 index futures, is trading higher during Wednesday’s morning session, supported by signals from Donald Trump, who indicated an indefinite extension of the ceasefire with Iran while awaiting a final, joint stance from Tehran. In recent weeks, gains in the S&P 500 appear to be significantly driven by buying activity from algorithmic Commodity Trading Advisors (CTAs), as confirmed by Goldman Sachs Prime data. After today’s US session, Tesla and IBM - both key index components are set to report earnings.

Are CTAs still buying?

Goldman Sachs signals that CTA buying potential in the S&P 500 remains positive in the short term, although it has weakened compared to a week ago. In practice, this means that over the coming week, trend-following strategies may still support Wall Street regardless of the market scenario.

- In a flat market scenario, Goldman estimates roughly $16 billion of buying over the next week. Over a one-month horizon, this drops to around $14 billion—significantly lower than previous forecasts of over $45 billion.

- In a strong upside scenario, the model still points to positive CTA flows: about $16 billion over a week and roughly $17 billion over a month. However, this too marks a clear cooling from earlier expectations, which were closer to $50 billion.

- The most notable shift appears in a downside scenario. In the short term, even with a sharper sell-off, CTAs would still be net buyers—around $16.5 billion over a week. The issue emerges over a longer horizon: in this case, the model points to roughly $19 billion of selling over the following month.

- This marks an important shift in tone, as just a week ago even a weaker market scenario still showed a slightly positive flow. Now, it appears that the medium-term demand cushion is beginning to fade.

- This change is driven by the rebuilding of CTA positioning. The more buying has already taken place, the less mechanical demand remains for the weeks ahead.

- In other words, short-term support for the S&P 500 has not disappeared, but its strength is gradually weakening. The market may still benefit from systematic buying flows, although the impulse is no longer as strong as before.

- Notably, the pace of global equity buying by CTAs over the past week ranked among the top five strongest episodes on record, totaling around $86 billion. The model also pointed to an additional $70 billion of potential demand over the following five sessions in a stable market environment.

- Historically, such rapid buying waves have often led to short-term consolidation, followed by renewed upside. According to Goldman Sachs, average returns for the S&P 500 in similar episodes were around +2.2% after one month and over +8% after three months.

From an investor perspective, the takeaway is relatively straightforward: in the short term, CTAs are still supporting the market, but over the medium term this effect is becoming less certain especially if a stronger wave of selling emerges on Wall Street.

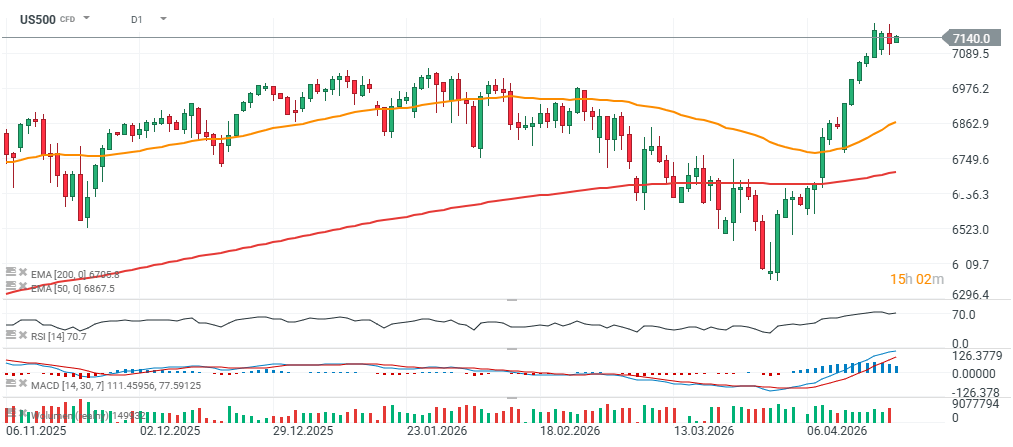

US500 (D1 chart)

S&P 500 futures (June contract) continue to show positive momentum, but the market is entering overbought territory, suggesting some caution is warranted. A short-term bullish signal emerged after breaking above the 9-period moving average, supporting the continuation of the uptrend. At the same time, a negative technical signal appeared in the form of a daily price reversal, which could point to a temporary slowdown in the trend—although buyers quickly stepped back in.

Another mild warning sign is the close below the local pivot level, indicating that buying pressure is no longer as strong as before. RSI has moved above 70, confirming overbought conditions and increasing the risk of a short-term correction. The nearest upside targets are in the 7170–7230 range, while immediate support levels are around 7075 and then near 7030.

Source: xStation5

Daily summary: Sense of relief to global markets🎢 OIL prices dip 8%🚨

BREAKING: US ISM Manufacturing - Strong Beat Across the Board

Eurozone PMIs: German Factory Revival Masks Underlying Stagnation 🇪🇺

Wall Street rebounds as Q2 earnings season significantly exceeds investors expectations

The content of this report has been created by XTB S.A., with its registered office in Warsaw, at Prosta 67, 00-838 Warsaw, Poland, (KRS number 0000217580) and supervised by Polish Supervision Authority ( No. DDM-M-4021-57-1/2005). This material is a marketing communication within the meaning of Art. 24 (3) of Directive 2014/65/EU of the European Parliament and of the Council of 15 May 2014 on markets in financial instruments and amending Directive 2002/92/EC and Directive 2011/61/EU (MiFID II). Marketing communication is not an investment recommendation or information recommending or suggesting an investment strategy within the meaning of Regulation (EU) No 596/2014 of the European Parliament and of the Council of 16 April 2014 on market abuse (market abuse regulation) and repealing Directive 2003/6/EC of the European Parliament and of the Council and Commission Directives 2003/124/EC, 2003/125/EC and 2004/72/EC and Commission Delegated Regulation (EU) 2016/958 of 9 March 2016 supplementing Regulation (EU) No 596/2014 of the European Parliament and of the Council with regard to regulatory technical standards for the technical arrangements for objective presentation of investment recommendations or other information recommending or suggesting an investment strategy and for disclosure of particular interests or indications of conflicts of interest or any other advice, including in the area of investment advisory, within the meaning of the Trading in Financial Instruments Act of 29 July 2005 (i.e. Journal of Laws 2019, item 875, as amended). The marketing communication is prepared with the highest diligence, objectivity, presents the facts known to the author on the date of preparation and is devoid of any evaluation elements. The marketing communication is prepared without considering the client’s needs, his individual financial situation and does not present any investment strategy in any way. The marketing communication does not constitute an offer of sale, offering, subscription, invitation to purchase, advertisement or promotion of any financial instruments. XTB S.A. is not liable for any client’s actions or omissions, in particular for the acquisition or disposal of financial instruments, undertaken on the basis of the information contained in this marketing communication. In the event that the marketing communication contains any information about any results regarding the financial instruments indicated therein, these do not constitute any guarantee or forecast regarding the future results.