Nasdaq 100 futures (US100) are up 0.15% today, pushing toward the 26,000 mark. The index appears just one step away from record territory, even as the sell-off in several tech heavyweights such as Microsoft and Palantir continues. Meanwhile, the Q4 2025 earnings season is now clearly past the midpoint, and the market is receiving a set of signals that can be read without overinterpreting them. The picture is consistent and repeatable: companies are delivering, revisions are moving higher, and earnings growth remains in double digits.

What we know for sure (with 59% of S&P 500 companies having reported)

-

76% of companies beat EPS expectations, and 73% beat on revenues.

-

Reported earnings are, on average, 7.6% above estimates, broadly in line with history (between the 5-year and 10-year averages).

-

Revenues are, on average, 1.4% above estimates (below the 5-year average of 2.0%, but in line with the 10-year average of 1.4%).

-

The blended earnings growth rate stands at 13.0% y/y for the S&P 500. If it holds, this would be the fifth consecutive quarter of double-digit earnings growth.

-

The blended revenue growth rate is 8.8% y/y, which would be the strongest pace since Q3 2022 (11.0%) and the 21st consecutive quarter of revenue growth for the index.

-

In-season revisions: as of December 31, the market was pricing 8.3% earnings growth for Q4; today it is 13.0%, reflecting positive EPS surprises and upward drift in the aggregate.

-

Q1 2026 guidance: 23 companies issued negative EPS guidance, while 28 issued positive guidance.

-

The S&P 500’s forward 12-month P/E is 21.5, above both the 5-year average (20.0) and the 10-year average (18.8). That matters because the market is not “cheap,” so the quality of earnings delivery carries extra weight.

Why do tech and globally exposed companies look better right now?

A practical angle from the data is geographic revenue exposure. With the US dollar softer, companies generating more sales outside the US are showing clearly stronger growth.

-

Companies with >50% of sales in the US: earnings +10.0% y/y, revenues +7.7% y/y

-

Companies with >50% of sales outside the US: earnings +17.7% y/y, revenues +11.9% y/y

Here is the key analytical nuance: NVIDIA is the largest single contributor to that outperformance. Excluding NVIDIA from the “more international exposure” group, growth cools to earnings +12.0% and revenues +9.9%. The gap narrows, but it does not disappear, suggesting the FX tailwind and broader global exposure are real, with NVDA providing an extra boost.

What has lifted the growth rate in recent days?

-

Over the past week, the improvement in the earnings growth rate has been driven mainly by positive EPS surprises, led by Communication Services, Health Care, and Financials.

-

Since December 31, the largest contributions to the increase in the earnings growth rate have come from Industrials, Information Technology, and Communication Services.

-

On the revenue side (since December 31), the biggest contributors to improved revenue growth have been Information Technology, Communication Services, Health Care, and Industrials.

-

9 of 11 sectors are reporting y/y earnings growth, led by Information Technology, Industrials, and Communication Services.

-

Two sectors are reporting y/y earnings declines: Consumer Discretionary and Health Care.

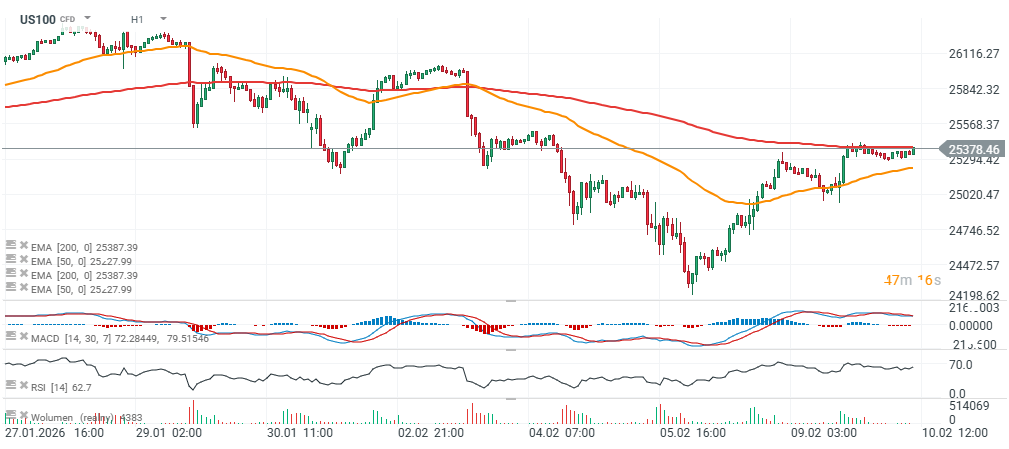

US100 (H1 timeframe)

US100 is trading above the 200-period EMA (red line) and sits roughly 1,000 points below the all-time high near 26,400.

Source: xStation5

Source: xStation5

Market Wrap: Energy Leads Gains in Europe, ASML Rebounds 🔼 Alcon Rises 4% After Earnings

Will the Wall Street Rally Gain Momentum? 🗽 A Recap of the US Earnings Season

Chart of the Day: USDJPY Rises Again. Intervention Is Not Enough — Markets Await BoJ Action

Economic Calendar: RBA Holds Rates, Markets Await US Housing Data

The content of this report has been created by XTB S.A., with its registered office in Warsaw, at Prosta 67, 00-838 Warsaw, Poland, (KRS number 0000217580) and supervised by Polish Supervision Authority ( No. DDM-M-4021-57-1/2005). This material is a marketing communication within the meaning of Art. 24 (3) of Directive 2014/65/EU of the European Parliament and of the Council of 15 May 2014 on markets in financial instruments and amending Directive 2002/92/EC and Directive 2011/61/EU (MiFID II). Marketing communication is not an investment recommendation or information recommending or suggesting an investment strategy within the meaning of Regulation (EU) No 596/2014 of the European Parliament and of the Council of 16 April 2014 on market abuse (market abuse regulation) and repealing Directive 2003/6/EC of the European Parliament and of the Council and Commission Directives 2003/124/EC, 2003/125/EC and 2004/72/EC and Commission Delegated Regulation (EU) 2016/958 of 9 March 2016 supplementing Regulation (EU) No 596/2014 of the European Parliament and of the Council with regard to regulatory technical standards for the technical arrangements for objective presentation of investment recommendations or other information recommending or suggesting an investment strategy and for disclosure of particular interests or indications of conflicts of interest or any other advice, including in the area of investment advisory, within the meaning of the Trading in Financial Instruments Act of 29 July 2005 (i.e. Journal of Laws 2019, item 875, as amended). The marketing communication is prepared with the highest diligence, objectivity, presents the facts known to the author on the date of preparation and is devoid of any evaluation elements. The marketing communication is prepared without considering the client’s needs, his individual financial situation and does not present any investment strategy in any way. The marketing communication does not constitute an offer of sale, offering, subscription, invitation to purchase, advertisement or promotion of any financial instruments. XTB S.A. is not liable for any client’s actions or omissions, in particular for the acquisition or disposal of financial instruments, undertaken on the basis of the information contained in this marketing communication. In the event that the marketing communication contains any information about any results regarding the financial instruments indicated therein, these do not constitute any guarantee or forecast regarding the future results.