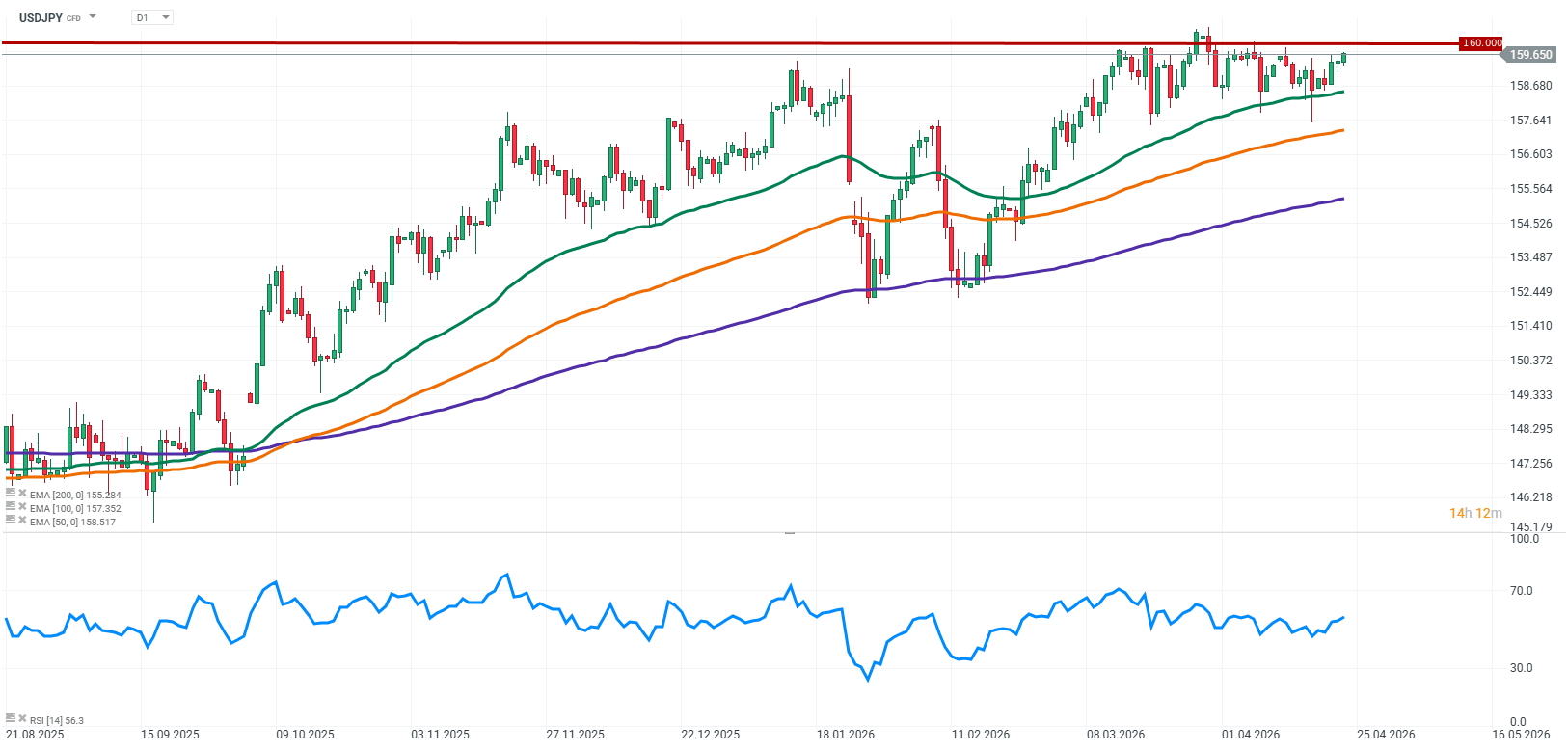

The USDJPY pair continues to trade in a heightened uncertainty environment, where geopolitical factors, macroeconomic data, and growing expectations regarding Bank of Japan policy are all influencing price action at the same time. The market is moving around key technical levels, with particular attention focused on the 160 area, which has been consistently defended and is widely viewed as a significant psychological barrier as well as a potential intervention zone for Japanese authorities. This raises an increasingly important question: whether this level will eventually be broken, and if so, under what conditions and timing. The current dynamics are driven both by global geopolitical tensions and by an intensifying debate over the possible normalization of monetary policy in Japan.

Source: xStation5

What drives USDJPY pricing?

Geopolitics and the Strait of Hormuz as a source of global risk aversion

One of the key drivers of market sentiment remains geopolitical tensions in regions critical for global energy transport, such as the Strait of Hormuz. The market reacts very sensitively to any risk of disruptions in oil and gas flows, which leads to higher energy prices and increased volatility.

Japan is heavily dependent on energy imports, largely sourced from the Persian Gulf region. As a result, rising oil and gas prices deteriorate Japan’s trade balance and increase imported inflation pressures. Therefore, prolonged tensions in the Hormuz region do not necessarily support the yen. Instead, they tend to weaken it. In this context, geopolitics does not provide a clear directional signal for USDJPY, but rather reinforces upside pressure on the pair while increasing overall volatility.

Japanese macro data and PMI signals

Recently, Japanese PMI data has attracted more attention, showing a gradual improvement in economic activity. While this is not yet a strong upward trend, signs of stabilization in both manufacturing and services increase the likelihood that the Bank of Japan will have more room to continue normalizing monetary policy.

For the FX market, this is important because the yen has remained under pressure for years due to ultra-loose monetary conditions. Even small shifts in this area can have a meaningful impact on global capital flows.

Inflation (CPI) as a key BOJ catalyst

One of the most important short-term drivers remains Japanese CPI data, which plays a central role in shaping expectations regarding future Bank of Japan actions. If inflation remains above the 2% target, markets increasingly price in the possibility of further rate hikes or at least a more hawkish communication stance from the central bank. In such a scenario, upward pressure on the yen increases.

Conversely, weaker inflation data reinforces expectations that ultra-loose policy will be maintained for longer, which supports further yen weakness against the dollar.

Bank of Japan policy and interest rate differentials

A key medium- and long-term factor remains Bank of Japan policy, which is gradually moving away from its long-standing regime of ultra-low interest rates and yield curve control. Even though this process is slow, its direction is highly significant for markets.

USDJPY is particularly sensitive to the interest rate differential between the US and Japan, which has been a major driver of yen weakness through carry trade strategies for years. Any narrowing of this spread could trigger significant capital flows and lead to shifts in the medium-term trend.

The 160 level and intervention risk

The 160 level on USDJPY remains a key reference point, both technically and politically. Historically, levels around this area have been repeatedly highlighted as zones of heightened vigilance by Japanese authorities regarding excessive FX volatility.

As a result, markets are increasingly pricing in the risk of intervention by the Japanese Ministry of Finance, which may take the form of either verbal warnings or direct FX market operations. Such interventions typically result in sharp but often short-lived strengthening of the yen.

Key Takeways

-

USDJPY remains in a high-volatility environment where direction is driven simultaneously by macroeconomic data, geopolitical developments, and central bank policy.

-

Geopolitical tensions, including the situation in the Strait of Hormuz, increase global risk aversion.

-

Japanese macro data, particularly PMIs, indicate gradual economic improvement and support the case for further BOJ normalization.

-

Inflation (CPI) remains a key short-term catalyst for BOJ expectations and the yen’s direction.

-

BOJ policy is becoming an increasingly important source of volatility, with even small communication shifts capable of moving the market.

-

The US–Japan interest rate differential remains the core structural driver of USD/JPY, and its potential narrowing could reshape medium-term dynamics.

-

The 160 level represents a major psychological and political barrier, increasing the risk of intervention or verbal action by Japanese authorities.

-

The market remains in a phase dominated by expectations and narratives, which supports sharp but often short-lived price moves.

Daily Summary: Semiconductors Rise in the Shadow of Geopolitical Turmoil

Tech sector catches its breath 🚀

Red Sea, but not the indices : The effects of the Bab al-Mandab blockade.

US OPEN: Semiconductors drive a rebound

The content of this report has been created by XTB S.A., with its registered office in Warsaw, at Prosta 67, 00-838 Warsaw, Poland, (KRS number 0000217580) and supervised by Polish Supervision Authority ( No. DDM-M-4021-57-1/2005). This material is a marketing communication within the meaning of Art. 24 (3) of Directive 2014/65/EU of the European Parliament and of the Council of 15 May 2014 on markets in financial instruments and amending Directive 2002/92/EC and Directive 2011/61/EU (MiFID II). Marketing communication is not an investment recommendation or information recommending or suggesting an investment strategy within the meaning of Regulation (EU) No 596/2014 of the European Parliament and of the Council of 16 April 2014 on market abuse (market abuse regulation) and repealing Directive 2003/6/EC of the European Parliament and of the Council and Commission Directives 2003/124/EC, 2003/125/EC and 2004/72/EC and Commission Delegated Regulation (EU) 2016/958 of 9 March 2016 supplementing Regulation (EU) No 596/2014 of the European Parliament and of the Council with regard to regulatory technical standards for the technical arrangements for objective presentation of investment recommendations or other information recommending or suggesting an investment strategy and for disclosure of particular interests or indications of conflicts of interest or any other advice, including in the area of investment advisory, within the meaning of the Trading in Financial Instruments Act of 29 July 2005 (i.e. Journal of Laws 2019, item 875, as amended). The marketing communication is prepared with the highest diligence, objectivity, presents the facts known to the author on the date of preparation and is devoid of any evaluation elements. The marketing communication is prepared without considering the client’s needs, his individual financial situation and does not present any investment strategy in any way. The marketing communication does not constitute an offer of sale, offering, subscription, invitation to purchase, advertisement or promotion of any financial instruments. XTB S.A. is not liable for any client’s actions or omissions, in particular for the acquisition or disposal of financial instruments, undertaken on the basis of the information contained in this marketing communication. In the event that the marketing communication contains any information about any results regarding the financial instruments indicated therein, these do not constitute any guarantee or forecast regarding the future results.