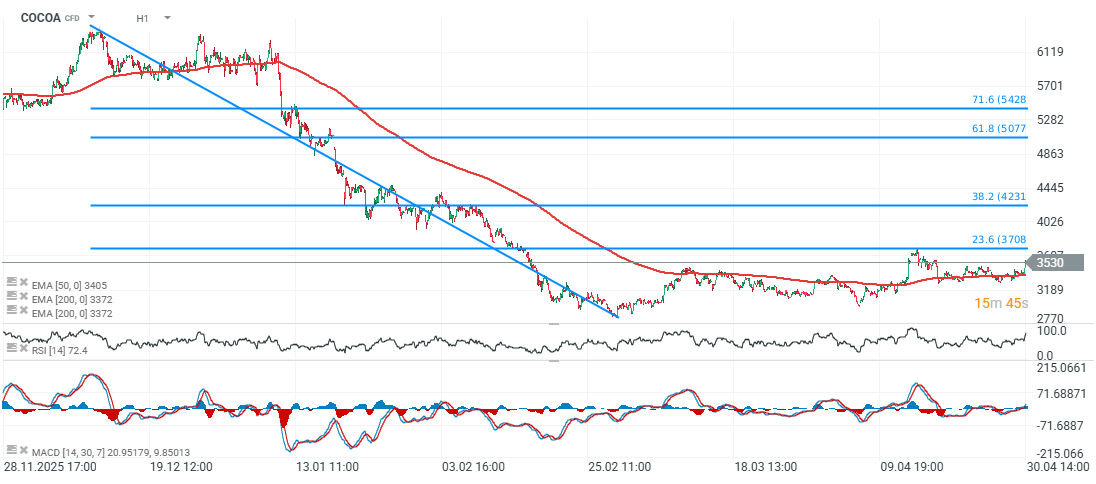

Cocoa futures on ICE (COCOA) are surging more than 4% today, rebounding from the local lows. Recent World Bank headlines suggesting a 50% collapse in cocoa prices in 2026 have sparked understandable concern across producing countries and among market participants. However, from a commodities market perspective, this interpretation reflects a misreading of base effects rather than a forward-looking signal of further downside. A closer look at price dynamics, positioning, and fundamentals suggests that the bulk of the correction is already behind us, and current levels are closer to a cyclical floor than the start of a new leg lower.

The correction has already played out

The cocoa market has undergone one of the most aggressive mean-reversion phases in recent commodity history.

- ICE cocoa futures have declined roughly 70 - 75% from the December 2024 peak (~$12,900/t)

- Prices are currently trading in the $3,000 - $3,500 range

- Year-to-date (2026), the market is down around 40 - 45%

Against this backdrop, the World Bank’s 2026 average forecast of ~$3,800/t is not a bearish call in spot terms. It reflects a year-on-year comparison to an inflated 2025 average rather than a projection of further structural downside from current levels. The forecast describes normalization, not collapse.

Is there a floor? Evidence points to yes

From a physical market standpoint, several factors suggest that the $3,000 region is increasingly acting as a support zone. Certified exchange stocks have recently peaked and are now starting to draw down, while European grinder inventories are tightening as destocking cycles mature. Commercial positioning also indicates reduced panic hedging compared to the 2024–2025 extremes. In other words, the supply overhang that followed the price spike is being absorbed, not expanding. However, it's not guaranteed and any weather change can change the market.

Weather risk: the underestimated variable

One of the most underappreciated elements in current pricing is weather asymmetry. The World Bank itself assigns a ~60% probability of El Niño conditions in H2 2026, which has historically:

- reduced rainfall across the West African cocoa belt

- disrupted yields during critical pod development phases

This directly challenges the baseline assumptions of a +34% production recovery in Ghana and +5% in Côte d’Ivoire. Market implication: if El Niño materializes, the current surplus narrative could quickly flip into supply tightening, forcing a repricing of risk.

Demand: destruction likely near its limits

The demand side has been under pressure, but the adjustment process appears mature. Over the past 12–18 months, chocolate manufacturers have reformulated products, reduced cocoa content, and adjusted packaging and portion sizes. However, elasticity has limits. Q1 grindings in Europe and North America were weak, but incremental demand destruction is slowing. As lower prices filter through, hedging cycles reset and forward cover is rebuilt, with grindings likely to stabilize into mid-2026 and gradually recover thereafter.

The World Bank vs market consensus

It is important to contextualize the World Bank forecast within the broader analyst spectrum. The Bank sits at the bearish end of institutional estimates. Other benchmarks include J.P. Morgan’s ~$6,000/t medium-term anchor and ING’s ~$4,400–$4,600/t equivalent for 2026. Rabobank and Citigroup have revised surplus estimates downward, pointing to a tighter supply picture than the Bank’s baseline suggests. Consensus view:

- 2026 likely closes just below $4,000/t

- with upside risk into 2027 as demand normalizes and weather risks are priced in

From a commodities strategy perspective, four pillars currently define the cocoa market: weather risk (El Niño probability), inventory normalization (stocks drawing down), demand stabilization (post-reformulation plateau), and supply.

COCOA (H1, D1)

Source: xStation5

Source: xStation5

Nasdaq-100 under pressure after chip sell-off

China Is Building Its Own Chip-Making Machines. ASML Under Pressure as the Technology War Enters a New Phase

US Open: Wall Street Rebounds After US Iran Ceasefire

🔴European TTF gas prices fall by 7.5%

The content of this report has been created by XTB S.A., with its registered office in Warsaw, at Prosta 67, 00-838 Warsaw, Poland, (KRS number 0000217580) and supervised by Polish Supervision Authority ( No. DDM-M-4021-57-1/2005). This material is a marketing communication within the meaning of Art. 24 (3) of Directive 2014/65/EU of the European Parliament and of the Council of 15 May 2014 on markets in financial instruments and amending Directive 2002/92/EC and Directive 2011/61/EU (MiFID II). Marketing communication is not an investment recommendation or information recommending or suggesting an investment strategy within the meaning of Regulation (EU) No 596/2014 of the European Parliament and of the Council of 16 April 2014 on market abuse (market abuse regulation) and repealing Directive 2003/6/EC of the European Parliament and of the Council and Commission Directives 2003/124/EC, 2003/125/EC and 2004/72/EC and Commission Delegated Regulation (EU) 2016/958 of 9 March 2016 supplementing Regulation (EU) No 596/2014 of the European Parliament and of the Council with regard to regulatory technical standards for the technical arrangements for objective presentation of investment recommendations or other information recommending or suggesting an investment strategy and for disclosure of particular interests or indications of conflicts of interest or any other advice, including in the area of investment advisory, within the meaning of the Trading in Financial Instruments Act of 29 July 2005 (i.e. Journal of Laws 2019, item 875, as amended). The marketing communication is prepared with the highest diligence, objectivity, presents the facts known to the author on the date of preparation and is devoid of any evaluation elements. The marketing communication is prepared without considering the client’s needs, his individual financial situation and does not present any investment strategy in any way. The marketing communication does not constitute an offer of sale, offering, subscription, invitation to purchase, advertisement or promotion of any financial instruments. XTB S.A. is not liable for any client’s actions or omissions, in particular for the acquisition or disposal of financial instruments, undertaken on the basis of the information contained in this marketing communication. In the event that the marketing communication contains any information about any results regarding the financial instruments indicated therein, these do not constitute any guarantee or forecast regarding the future results.