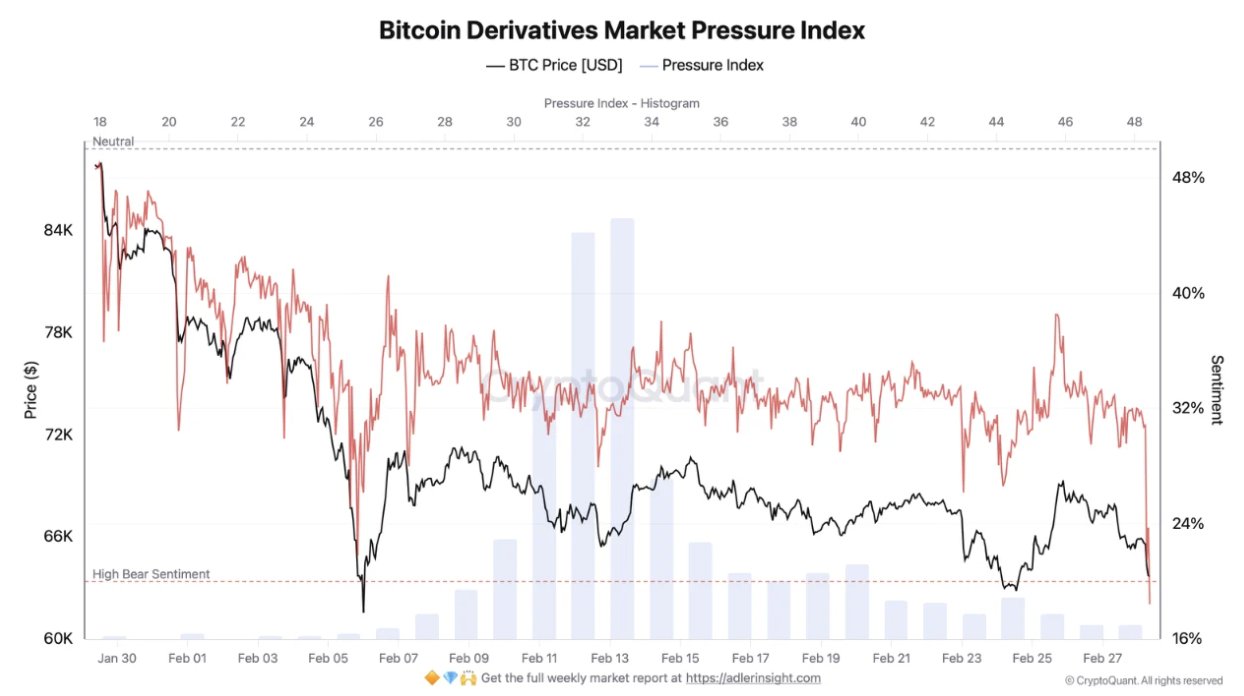

Despite the war in the Middle East and clearly weaker sentiment across equity markets—driven by rising oil prices and renewed inflation concerns - Bitcoin has reacted relatively calmly. Following the Israeli and U.S. strikes on targets in Iran, BTC briefly dropped to around $63,000 on Saturday morning, but has since rebounded by roughly 5% and is now stabilizing near $66,500. On-chain data initially confirmed selling pressure in BTC derivatives, with liquidations peaking at approximately $1.8 billion in positions, yet the market quickly regained balance.

Source: CryptoQuant

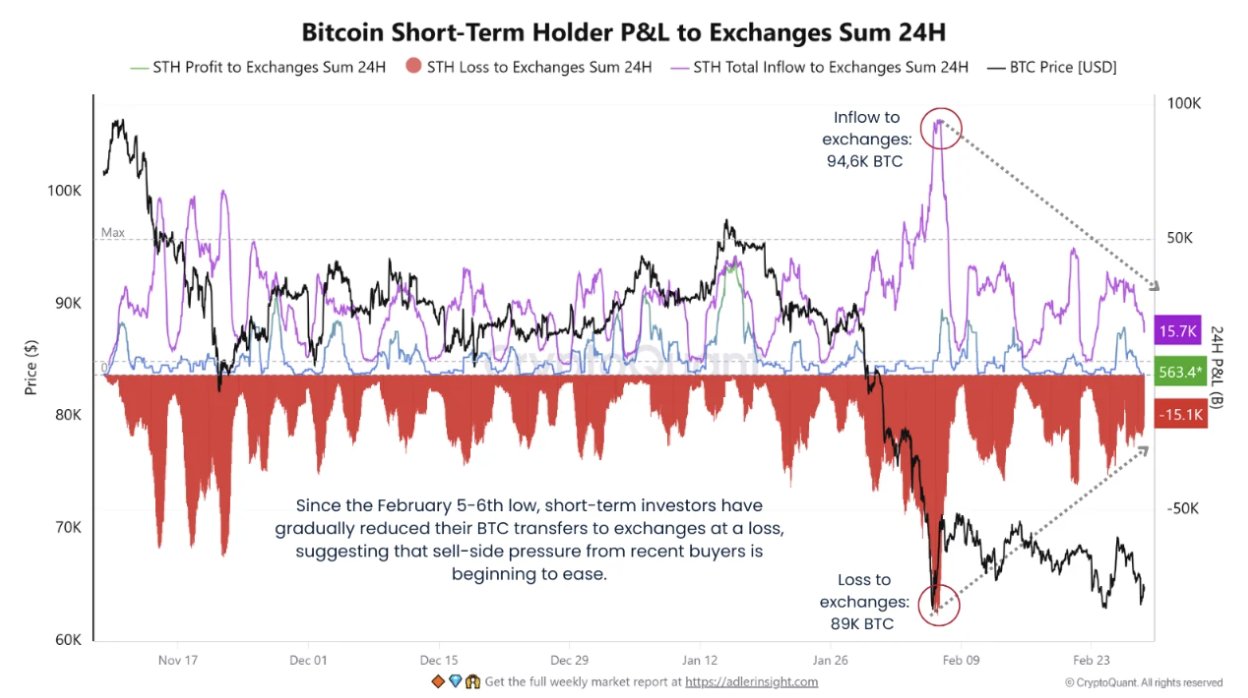

Somewhat surprisingly, short-term holders did not engage in массов selling, which may suggest a phase of “supply exhaustion” at this stage of the cycle and indicates that Bitcoin is currently held by relatively stronger hands.

Source: CryptoQuant

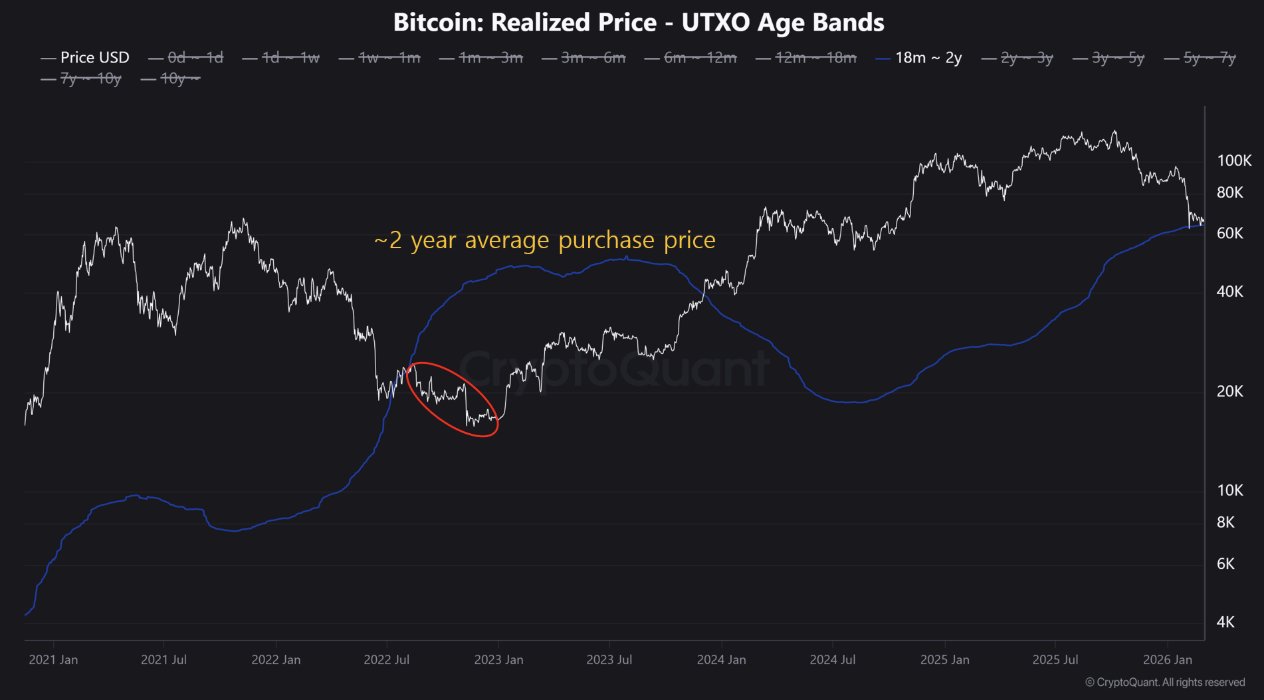

On the other hand, a significant portion of BTC supply accumulated over the past two years remains at a loss. A move below the psychologically important $60,000 level could sharply increase unrealized losses among long-term holders.

Source: CryptoQuant

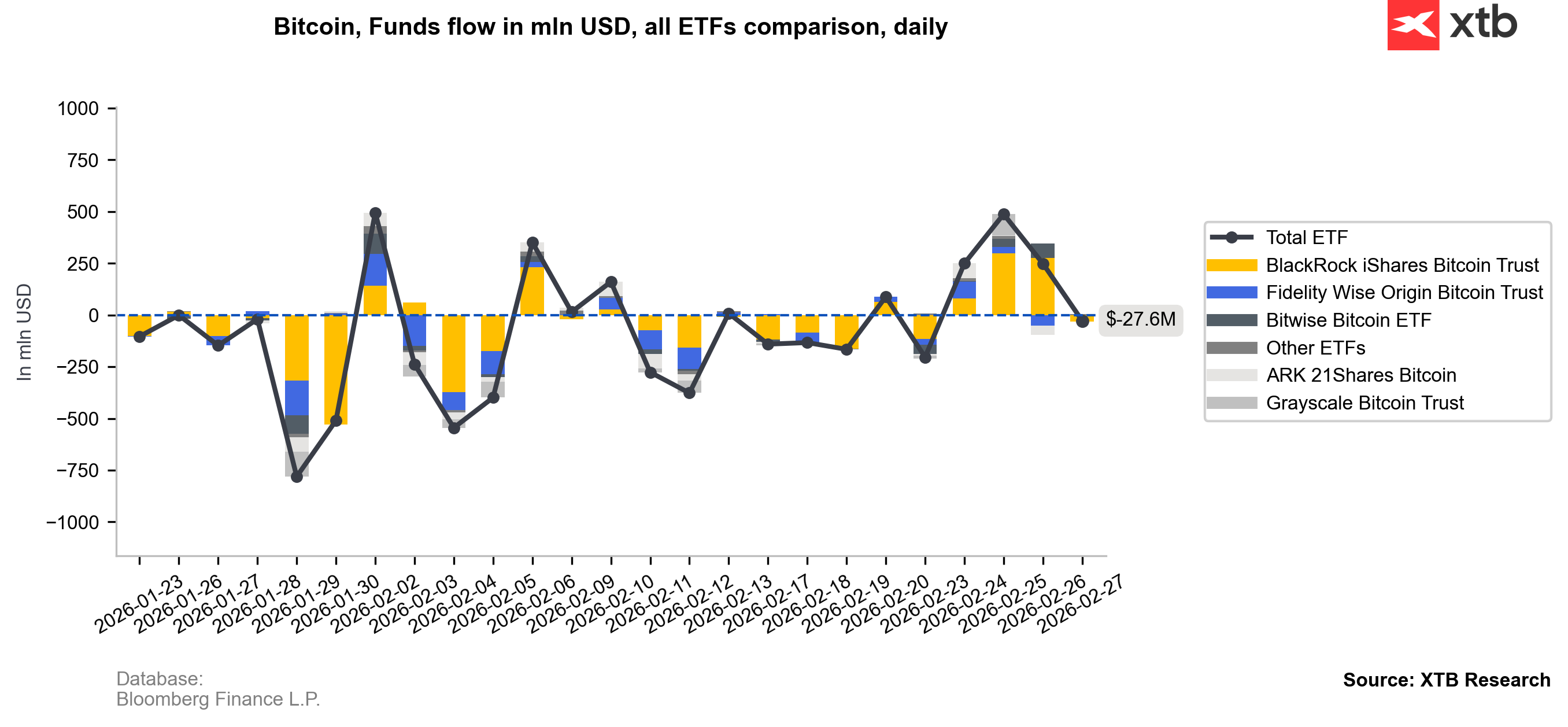

ETFs are not panicking (as for now)

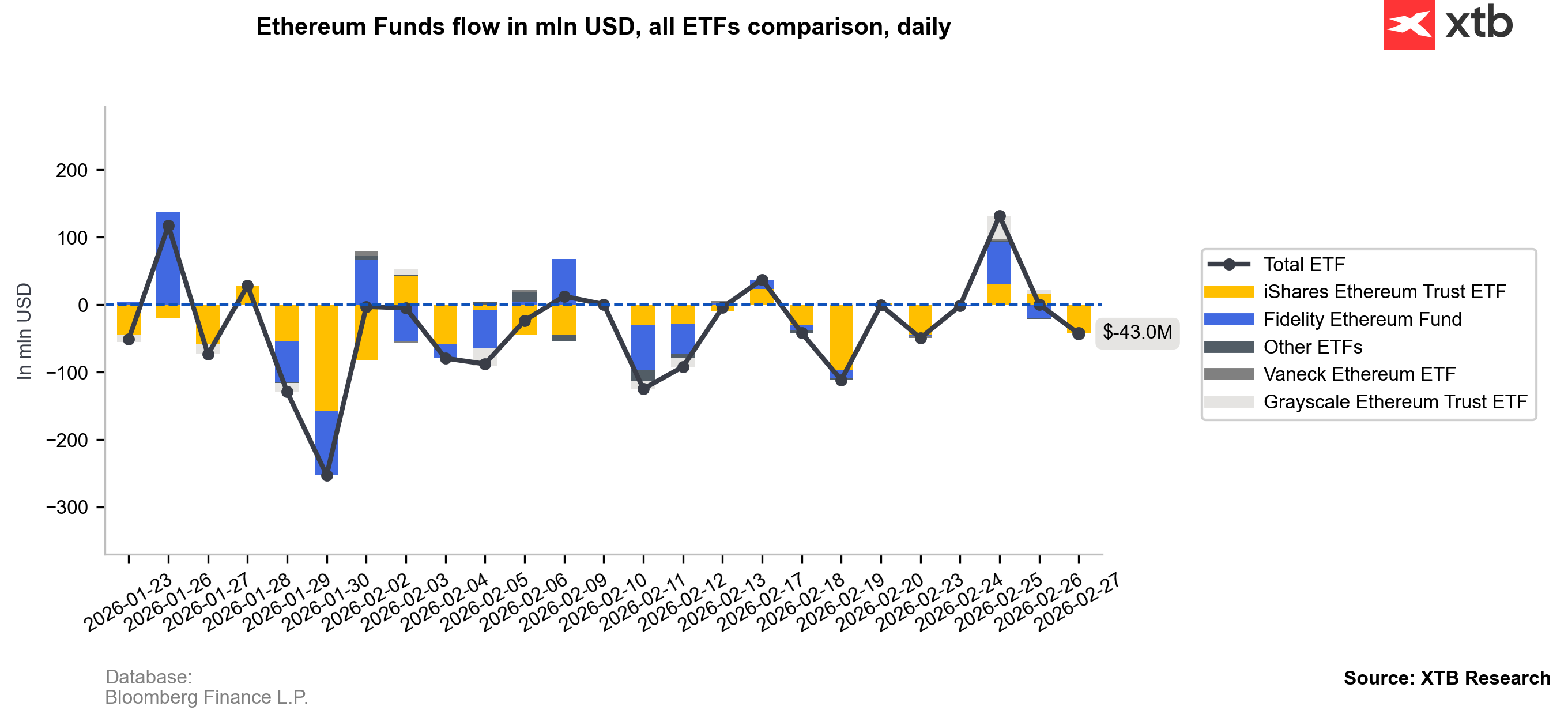

At this stage of the market cycle, investor focus remains firmly on Bitcoin, while Ethereum has clearly taken a back seat. This is visible in ETF flows: capital continues to favor Bitcoin, and without a sustained rebound in BTC, a broader crypto bull market including ETH - appears unlikely for now. With the exception of last Monday and Friday, Bitcoin ETFs recorded clearly positive net inflows last week. Ethereum ETFs, by contrast, saw only marginally positive flows.

Source: XTB Research, Bloomberg Finance L.P.

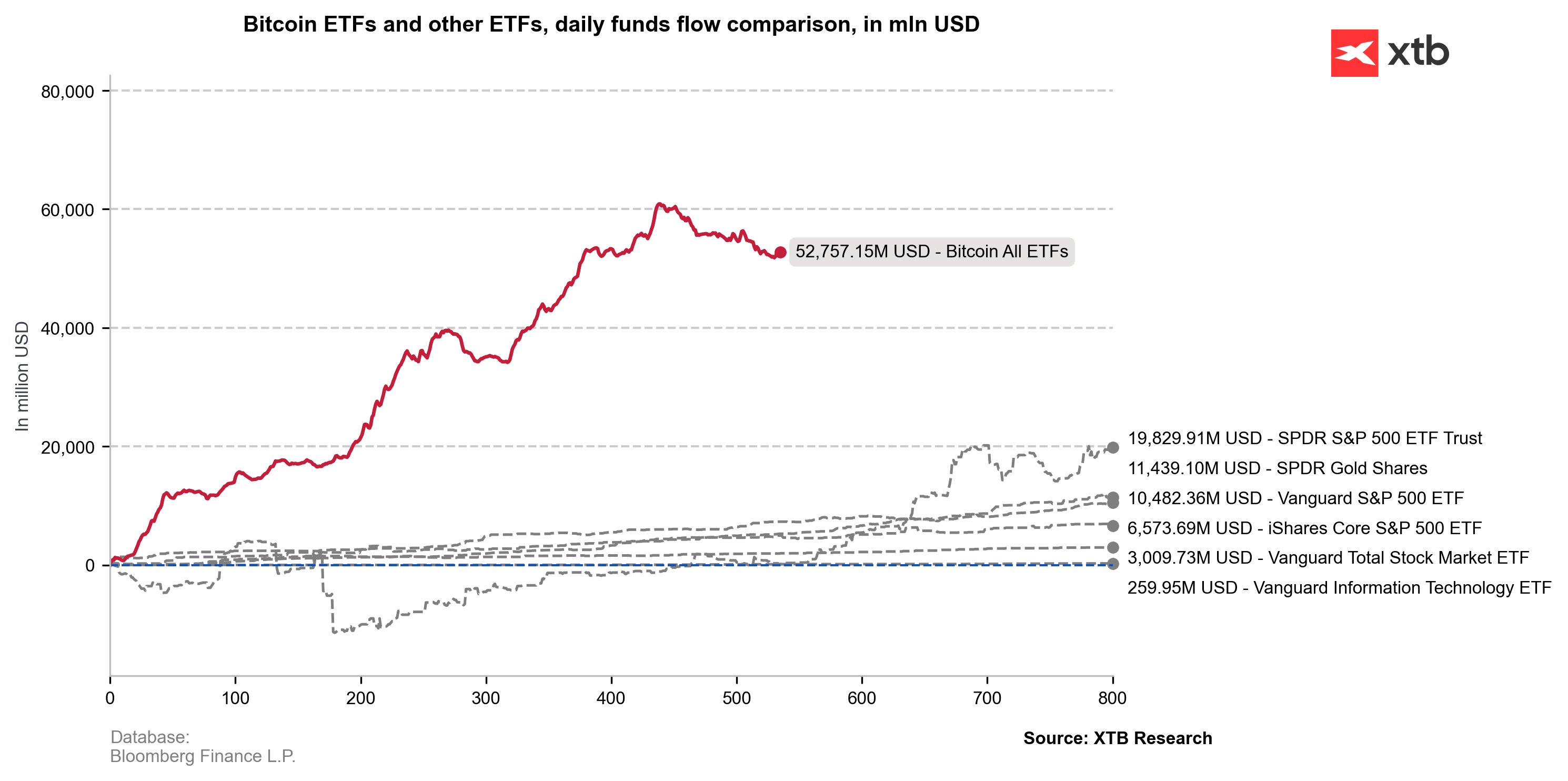

Cumulative capital in crypto ETFs remains substantial. From peak levels, assets have declined by roughly 15%, despite Bitcoin falling nearly 50% from its all-time highs. This suggests that although ETF-related selling has accelerated in recent months, it is still far from extreme.

Source: XTB Research, Bloomberg Finance L.P.

Bitcoin and Ethereum charts (D1)

From a technical perspective, Bitcoin appears set to remain in consolidation between $60,000 and $72,000 in the near term. The market is likely searching for a catalyst to trigger a more decisive move in either direction. Another downward impulse toward $50,000 cannot be ruled out- especially if global equity conditions deteriorate further, favoring the U.S. dollar, bond yields, and oil. Conversely, a decisive breakout above the $74,000–$75,000 area would increase the probability of a more durable recovery attempt.

Source: xStation5

Daily Summary: Failure of negotiations in the gulf, oil and gas prices soar

US OPEN: Debt and the Strait of Hormuz fuel growing concerns.

⬆️TTF gas rises over 6% near 58 EUR

Economic Calendar: Markets Awaken After a Weekend of Geopolitical Deadlock🚢

The content of this report has been created by XTB S.A., with its registered office in Warsaw, at Prosta 67, 00-838 Warsaw, Poland, (KRS number 0000217580) and supervised by Polish Supervision Authority ( No. DDM-M-4021-57-1/2005). This material is a marketing communication within the meaning of Art. 24 (3) of Directive 2014/65/EU of the European Parliament and of the Council of 15 May 2014 on markets in financial instruments and amending Directive 2002/92/EC and Directive 2011/61/EU (MiFID II). Marketing communication is not an investment recommendation or information recommending or suggesting an investment strategy within the meaning of Regulation (EU) No 596/2014 of the European Parliament and of the Council of 16 April 2014 on market abuse (market abuse regulation) and repealing Directive 2003/6/EC of the European Parliament and of the Council and Commission Directives 2003/124/EC, 2003/125/EC and 2004/72/EC and Commission Delegated Regulation (EU) 2016/958 of 9 March 2016 supplementing Regulation (EU) No 596/2014 of the European Parliament and of the Council with regard to regulatory technical standards for the technical arrangements for objective presentation of investment recommendations or other information recommending or suggesting an investment strategy and for disclosure of particular interests or indications of conflicts of interest or any other advice, including in the area of investment advisory, within the meaning of the Trading in Financial Instruments Act of 29 July 2005 (i.e. Journal of Laws 2019, item 875, as amended). The marketing communication is prepared with the highest diligence, objectivity, presents the facts known to the author on the date of preparation and is devoid of any evaluation elements. The marketing communication is prepared without considering the client’s needs, his individual financial situation and does not present any investment strategy in any way. The marketing communication does not constitute an offer of sale, offering, subscription, invitation to purchase, advertisement or promotion of any financial instruments. XTB S.A. is not liable for any client’s actions or omissions, in particular for the acquisition or disposal of financial instruments, undertaken on the basis of the information contained in this marketing communication. In the event that the marketing communication contains any information about any results regarding the financial instruments indicated therein, these do not constitute any guarantee or forecast regarding the future results.