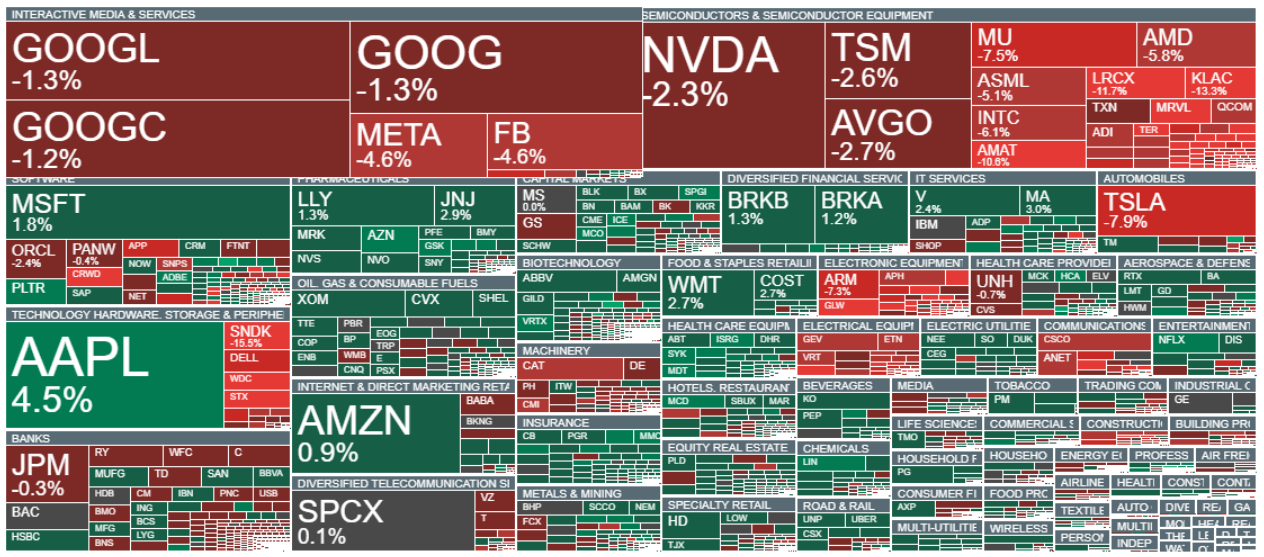

U.S. equity sentiment deteriorated sharply during the second half of the session, with the Nasdaq 100 falling 2.3% despite an initially positive reaction to weaker-than-expected U.S. nonfarm payroll (NFP) data. Micron is down 7.5%, while several semiconductor companies have dropped by more than 10%. Among the Big Tech names, Meta Platforms is the biggest laggard, losing nearly 5%, whereas Apple (AAPL.US) is outperforming with a gain of around 4.5%. Tesla is also under pressure, falling almost 8%, despite reporting second-quarter vehicle deliveries that exceeded market expectations.

As U.S. Treasury yields declined following the weaker NFP report and oil prices remained lower, gold rebounded above $4,100 per ounce, while silver gained nearly 2.5%. The U.S. dollar weakened, pushing EUR/USD almost 0.5% higher to above 1.143. Bitcoin recovered toward $62,000, although sentiment across the cryptocurrency market remains cautious. Meanwhile, Brent crude is trading around $71.50 per barrel, staging a modest rebound after the sharp declines seen in recent sessions.

U.S. macroeconomic data

The latest U.S. labor market report came in significantly weaker than expected.

- Nonfarm Payrolls (NFP) increased by 57,000, well below the 113,000 consensus forecast and the previous reading of 172,000.

- The U.S. unemployment rate fell to 4.2%, beating expectations of 4.3%.

- Initial Jobless Claims came in at 215,000, better than the expected 218,000 and unchanged from the previous reading.

- Average Hourly Earnings rose 3.5% year-over-year, above the 3.4% consensus.

- Private Payrolls increased by just 49,000, missing expectations of 107,000.

- Continuing Jobless Claims declined to 1.814 million, slightly below the expected 1.820 million.

- The Average Workweek remained unchanged at 34.3 hours, in line with expectations.

- Average Hourly Earnings rose 0.3% month-over-month, matching both the forecast and the previous reading.

- Manufacturing Payrolls increased by 3,000, meeting expectations but below the previous 7,000 increase.

- The Labor Force Participation Rate fell to 61.5%, below both the 61.8% forecast and the previous reading.

- Government Payrolls declined by 8,000, following a 52,000 increase in the previous month.

The latest EIA Natural Gas Storage Report showed an inventory build of 87 billion cubic feet (Bcf), slightly above the 84 Bcf consensus forecast and the previous 76 Bcf increase. Natural gas futures initially moved lower following the release but later erased those early losses.

In the commodities market, CBOT wheat futures continue to trade above 600 cents per bushel, while ICE cocoa futures are down around 1.2% on the day.

Source: xStation 5

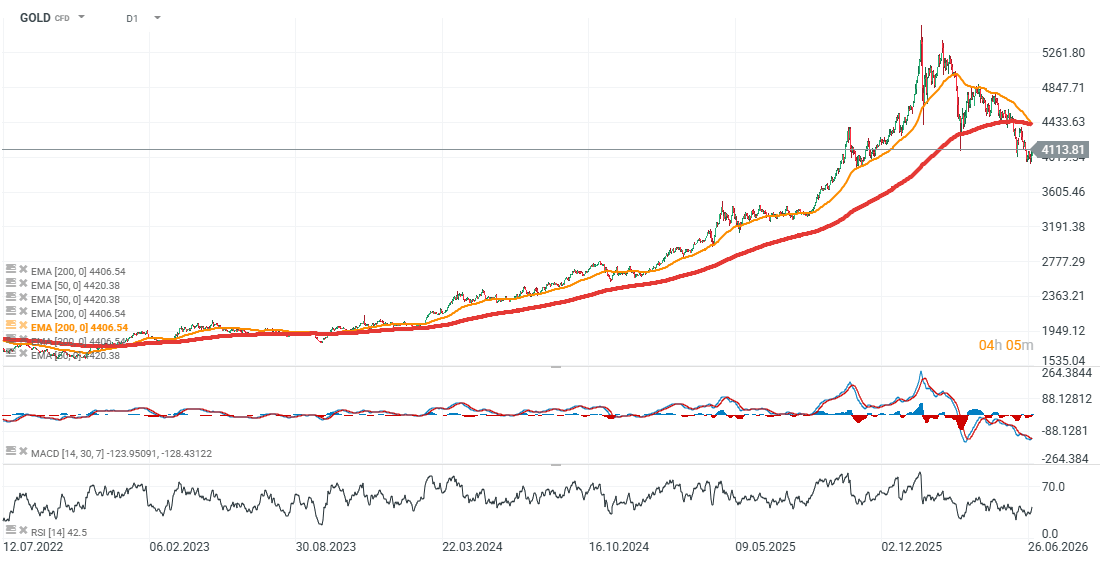

Gold (D1)

Gold has rebounded from the $3,900 area to above $4,100 per ounce, while the 50-day EMA has crossed below the 200-day EMA, forming a classic death cross. Interestingly, the last time this pattern appeared in 2023, it turned into a contrarian bullish signal, with gold beginning a major rally shortly after the moving averages crossed. The next major resistance is located around $4,400, while key support levels remain at $4,000 and $3,900.

Source: xStation 5

Oil rises over 3% 🛢️

Economic Calendar: Big Tech, Tensions Over Iran, and the ECB’s Decision ⏰

Morning Wrap: A New Threat of Conflict in the Middle East 🚨 (23.07.2026)

Daily Summary: Wall Street Stabilizes Despite Higher Oil Prices

The content of this report has been created by XTB S.A., with its registered office in Warsaw, at Prosta 67, 00-838 Warsaw, Poland, (KRS number 0000217580) and supervised by Polish Supervision Authority ( No. DDM-M-4021-57-1/2005). This material is a marketing communication within the meaning of Art. 24 (3) of Directive 2014/65/EU of the European Parliament and of the Council of 15 May 2014 on markets in financial instruments and amending Directive 2002/92/EC and Directive 2011/61/EU (MiFID II). Marketing communication is not an investment recommendation or information recommending or suggesting an investment strategy within the meaning of Regulation (EU) No 596/2014 of the European Parliament and of the Council of 16 April 2014 on market abuse (market abuse regulation) and repealing Directive 2003/6/EC of the European Parliament and of the Council and Commission Directives 2003/124/EC, 2003/125/EC and 2004/72/EC and Commission Delegated Regulation (EU) 2016/958 of 9 March 2016 supplementing Regulation (EU) No 596/2014 of the European Parliament and of the Council with regard to regulatory technical standards for the technical arrangements for objective presentation of investment recommendations or other information recommending or suggesting an investment strategy and for disclosure of particular interests or indications of conflicts of interest or any other advice, including in the area of investment advisory, within the meaning of the Trading in Financial Instruments Act of 29 July 2005 (i.e. Journal of Laws 2019, item 875, as amended). The marketing communication is prepared with the highest diligence, objectivity, presents the facts known to the author on the date of preparation and is devoid of any evaluation elements. The marketing communication is prepared without considering the client’s needs, his individual financial situation and does not present any investment strategy in any way. The marketing communication does not constitute an offer of sale, offering, subscription, invitation to purchase, advertisement or promotion of any financial instruments. XTB S.A. is not liable for any client’s actions or omissions, in particular for the acquisition or disposal of financial instruments, undertaken on the basis of the information contained in this marketing communication. In the event that the marketing communication contains any information about any results regarding the financial instruments indicated therein, these do not constitute any guarantee or forecast regarding the future results.