- China's Hang Seng Index failed to repeat yesterday's gains, and Chinese index futures today saw a nearly 3% correction in the rebound, driven by dovish signals from the PBoC. European indices CAC40 and FTSE posted near 0.5% declines, DAX retreated slightly;

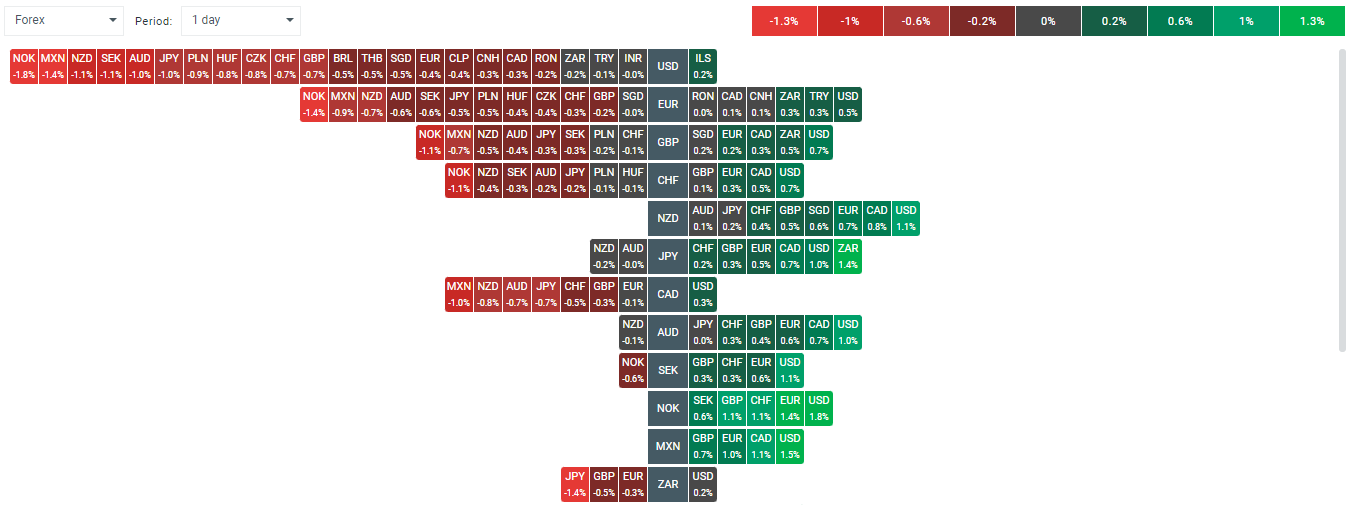

- The attention of the currency market today is captured by the dollar, which is recording a massive strengthening. USDIDX is gaining almost 0.7% and EURUSD has rapidly slid from local maxima near 1.12 to around 1.113 today, losing 0.4%. 10-year bond yields are up about 4 bps to 3.77%. Despite that gold gains 0.2% today,

- After a fairly positive opening of the US stock market, we are seeing a cooling of sentiment. Nvidia erased some of the growth and is now gaining 2%, while the US100 is trading flat and the US30 is losing 0.6%, buoyed largely by a nearly 5% drop in shares of pharmaceutical company Amgen

- Apple shares lose nearly 1% after August data pointed to low demand in China. New Street reported that it expects about 10% negative disappointment in this year's iPhone shipments (215 million shipments expected, 10% below consensus); however, it maintained its $225 per share rating

- Since news of the opening of the Three Mile Island nuclear power plant, which will supply power to Microsoft's data centers, speculative interest has been evident among uranium-related companies, with Denison Mines gaining nearly 6%, following an upgrade at BMO Capital

- U.S. new home sales data turned out to be marginally stronger than forecast. Home sales for August: 716,000 (expected: 699,000; previous: 751,000). The growth rate was -4.7% m/m (previous: 10.3% m/m). Earlier data showed an 11% increase in mortgage applications on a weekly basis, following last week's 14.2% increase.

- According to the US administration, there is still a risk of a full-blown escalation in the Middle East; Biden's statements indicate this, and Anthony Blinken indicated that the situation could escalate rapidly. Yesterday, Hezbollah took another rocket fire at Israel. Oil, however, retreated on the wave of 'de-escalation' of tensions in Libya.

Inventories according to the EIA indicated a stronger than expected decline in stocks. There was a decline in inventories, plus a drop in refining capacity utilization with fuel demand rising, but Brent Crude lost more than 2.3%

- Change in Brent Crude inventories: -4.47 million brk (expected: -1.43 million brk; previous: -1.63 million brk)

- Gasoline inventories: -1.5 million brk (expected: +0.2 million brk; previous: +0.069 million brk)

- Distillate stocks: -2.2 million brk (expected: -1.2 million brk; previous: +0.125 million brk)

- Russian President Putin indicated today that Russia would consider a nuclear response to even a conventional attack on its territory by a non-nuclear-weapon state, but supported by a nuclear-armed state, or group of nuclear-armed states. He indicated that new geopolitical realities will change Russia's 'nuclear doctrine'

- Among agricultural commodities, we can see the largest drop of almost 1.7% in cotton futures, however sentiments around wheat, soybean, coffee and sugar are solid, as grains gain in the range of 1-1.5%.

- Despite positive comments from analysts at QCP Capital, sentiment around cryptocurrencies remains mixed. Bitcoin slides to $63.500, despite dovish signals from China, where the PBoC announced rate cuts, potentially boosting interest in bitcoin and ETFs listed in Hong Kong

- OECD Chief Economist Pereira called, that US economy is very robust. OECD sees the US Federal Reserve cutting rates to 3.50% by end 2025, and ECB cutting to 2.25% by end 2025; estimates 2024 US GDP growth forecast at 2.6% (unchanged), but trims 2025 to 1.6% (1.8% previously).

The US dollar dominates today's currency market session, but despite that gold gains almost 0.2% today. Source: xStation5

The US dollar dominates today's currency market session, but despite that gold gains almost 0.2% today. Source: xStation5

Daily Summary: Equities Diverge as Tech Lags, Europe Rallies on Earnings & PMIs (24.07.2026)

Three markets to watch next week (24.07.2026)

Oil Slides Ahead of the Weekend!

BREAKING: Eurozone recovery? Positive PMI data tempered by high oil and gas prices

The content of this report has been created by XTB S.A., with its registered office in Warsaw, at Prosta 67, 00-838 Warsaw, Poland, (KRS number 0000217580) and supervised by Polish Supervision Authority ( No. DDM-M-4021-57-1/2005). This material is a marketing communication within the meaning of Art. 24 (3) of Directive 2014/65/EU of the European Parliament and of the Council of 15 May 2014 on markets in financial instruments and amending Directive 2002/92/EC and Directive 2011/61/EU (MiFID II). Marketing communication is not an investment recommendation or information recommending or suggesting an investment strategy within the meaning of Regulation (EU) No 596/2014 of the European Parliament and of the Council of 16 April 2014 on market abuse (market abuse regulation) and repealing Directive 2003/6/EC of the European Parliament and of the Council and Commission Directives 2003/124/EC, 2003/125/EC and 2004/72/EC and Commission Delegated Regulation (EU) 2016/958 of 9 March 2016 supplementing Regulation (EU) No 596/2014 of the European Parliament and of the Council with regard to regulatory technical standards for the technical arrangements for objective presentation of investment recommendations or other information recommending or suggesting an investment strategy and for disclosure of particular interests or indications of conflicts of interest or any other advice, including in the area of investment advisory, within the meaning of the Trading in Financial Instruments Act of 29 July 2005 (i.e. Journal of Laws 2019, item 875, as amended). The marketing communication is prepared with the highest diligence, objectivity, presents the facts known to the author on the date of preparation and is devoid of any evaluation elements. The marketing communication is prepared without considering the client’s needs, his individual financial situation and does not present any investment strategy in any way. The marketing communication does not constitute an offer of sale, offering, subscription, invitation to purchase, advertisement or promotion of any financial instruments. XTB S.A. is not liable for any client’s actions or omissions, in particular for the acquisition or disposal of financial instruments, undertaken on the basis of the information contained in this marketing communication. In the event that the marketing communication contains any information about any results regarding the financial instruments indicated therein, these do not constitute any guarantee or forecast regarding the future results.