President Donald Trump reversed his stance twice in the space of a single day — first announcing that the deal with Iran was “dead” following the attacks on merchant ships in the Strait of Hormuz, and then suggesting that Tehran was desperately seeking an agreement. This 180-degree turnaround in the space of a dozen or so hours clearly illustrates how Trump’s unpredictable communication affects market sentiment in real time.

From ‘the deal is over’ to ‘they want the deal so badly’

On Wednesday 8 July, US index futures fell and oil prices soared by more than 5% after Trump declared that the truce with Iran was “over” following Iran’s attack on merchant ships. The S&P 500 closed the session down 0.28 per cent at 7,482.71 points. Just a few hours later, Trump changed his tone, claiming that Iran had “just phoned” and “wants a deal very, very badly”, though he noted that he did not know whether Tehran could be trusted to honour the terms. This news immediately triggered a reversal in market sentiment — futures contracts on US indices turned green. When a reporter asked why Iran was attacking merchant ships if it wanted a deal so badly, Trump replied briefly: “Because they’re a bit mad.”

This pattern is nothing new — since March, futures contracts have repeatedly reacted sharply to successive rounds of Trump’s rhetoric towards Iran, falling at times following threats of strikes and rebounding at other times following signs of an impending agreement.

Spain: from a ‘lost country’ to a ‘very generous partner’

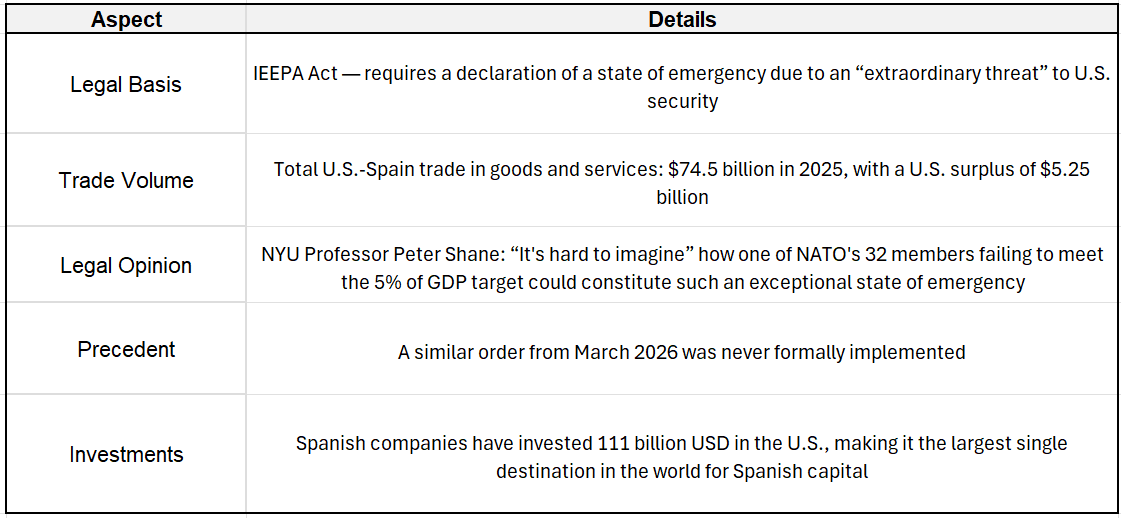

A similar narrative shift affected Spain. At the NATO summit in Ankara, Trump described Madrid as a “lost cause” and a “completely hopeless” partner, ordering Treasury Secretary Scott Bessent to immediately suspend all trade with Spain, including visas. The reason was Spain’s refusal to accept NATO’s new defence spending target of 5 per cent of GDP, as well as its earlier blocking of the use of joint military bases for attacks on Iran.

On the flight back to Washington aboard Air Force One, Trump changed his tone, claiming that Spain had “come round completely” and had been “very generous” — it had “honoured the request for numerous payments”. Prime Minister Pedro Sánchez, for his part, described the conversation as “very cordial”, noting that it had focused mainly on the World Cup and golf, rather than military spending.

How likely is an embargo on Spain?

Despite his statements, Trump has real, albeit limited, legal means at his disposal to impose an embargo.

The Department of the Treasury, the Department of Commerce and the Office of the US Trade Representative are due to draw up a “list” of Spanish products potentially subject to an embargo in the coming days, which suggests a selective rather than a blanket approach. It is worth bearing in mind that EU trade rules require a uniform approach towards all EU countries, which complicates unilateral action against Spain alone.

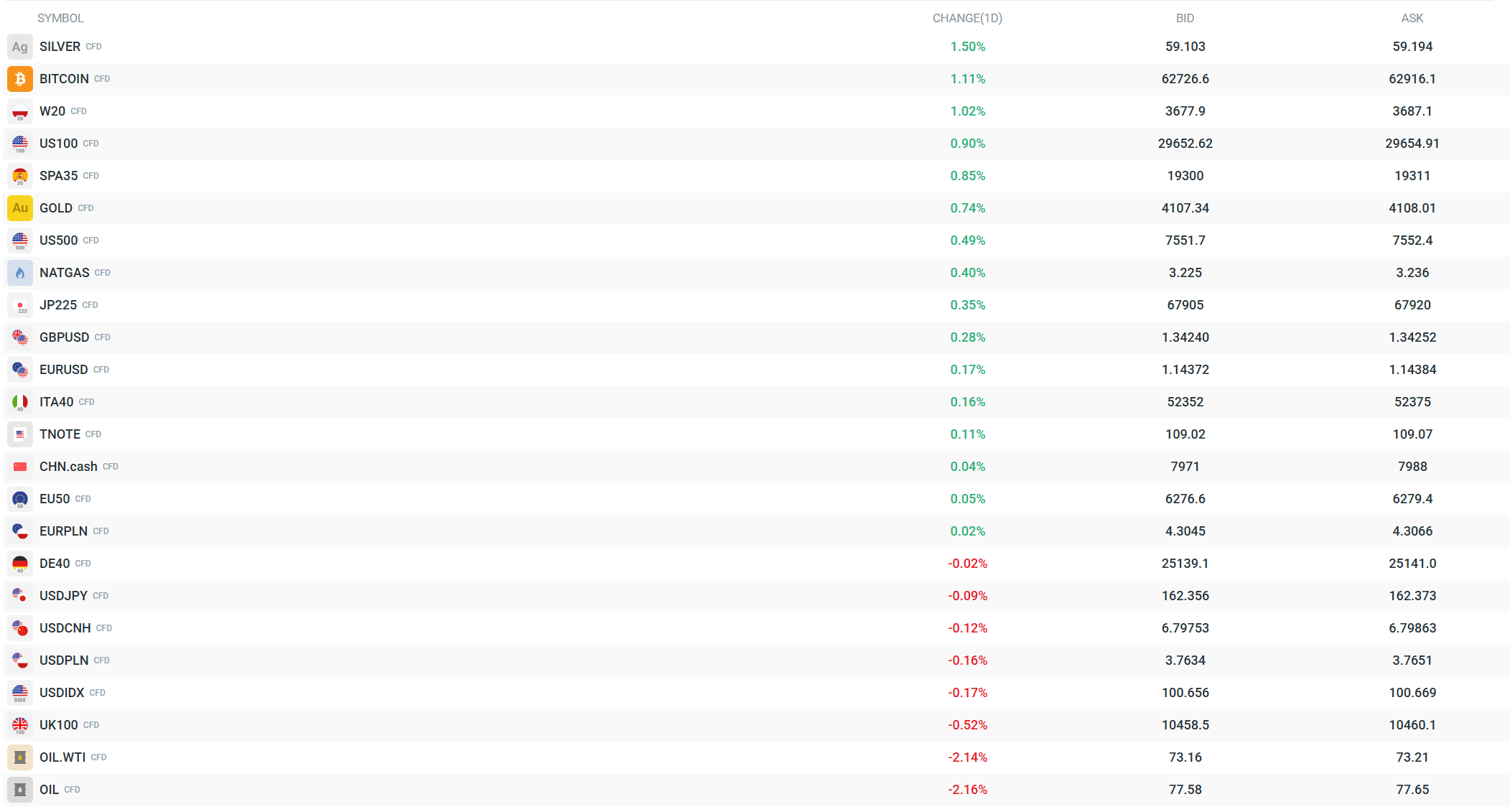

The markets are performing very well this morning. Spanish shares are up 0.8%, whilst oil is down by over 2%. Source: xStation

Apple is still impressive, but the market is no longer impressed

Amazon’s massive AI bet is starting to pay off

Daily Summary: Equities rally on not-so-hawkish Fed and AI trade revival, Yen dominates FX, oil retreats (30.07.2026)

Unexpected FX intervention? USDJPY plummets more than 2%! 🇯🇵

The content of this report has been created by XTB S.A., with its registered office in Warsaw, at Prosta 67, 00-838 Warsaw, Poland, (KRS number 0000217580) and supervised by Polish Supervision Authority ( No. DDM-M-4021-57-1/2005). This material is a marketing communication within the meaning of Art. 24 (3) of Directive 2014/65/EU of the European Parliament and of the Council of 15 May 2014 on markets in financial instruments and amending Directive 2002/92/EC and Directive 2011/61/EU (MiFID II). Marketing communication is not an investment recommendation or information recommending or suggesting an investment strategy within the meaning of Regulation (EU) No 596/2014 of the European Parliament and of the Council of 16 April 2014 on market abuse (market abuse regulation) and repealing Directive 2003/6/EC of the European Parliament and of the Council and Commission Directives 2003/124/EC, 2003/125/EC and 2004/72/EC and Commission Delegated Regulation (EU) 2016/958 of 9 March 2016 supplementing Regulation (EU) No 596/2014 of the European Parliament and of the Council with regard to regulatory technical standards for the technical arrangements for objective presentation of investment recommendations or other information recommending or suggesting an investment strategy and for disclosure of particular interests or indications of conflicts of interest or any other advice, including in the area of investment advisory, within the meaning of the Trading in Financial Instruments Act of 29 July 2005 (i.e. Journal of Laws 2019, item 875, as amended). The marketing communication is prepared with the highest diligence, objectivity, presents the facts known to the author on the date of preparation and is devoid of any evaluation elements. The marketing communication is prepared without considering the client’s needs, his individual financial situation and does not present any investment strategy in any way. The marketing communication does not constitute an offer of sale, offering, subscription, invitation to purchase, advertisement or promotion of any financial instruments. XTB S.A. is not liable for any client’s actions or omissions, in particular for the acquisition or disposal of financial instruments, undertaken on the basis of the information contained in this marketing communication. In the event that the marketing communication contains any information about any results regarding the financial instruments indicated therein, these do not constitute any guarantee or forecast regarding the future results.