At 1:30 PM BST, the latest Consumer Price Index (CPI) reading for the United States for June will be released. The U.S. dollar is slipping ahead of the publication, although the market’s expectation of rising inflationary pressure may support the greenback through hawkish Fed policy speculation.

What to Expect from U.S. Inflation:

-

In June, prices are expected to rise 0.3% month-over-month (vs. +0.1% in May) and 2.6% year-over-year (vs. +2.4% in May).

-

Core inflation is also expected to rise: +0.3% m/m (May: 0.1%) and +2.9% y/y (May: 2.8%).

-

Tariffs are expected to drive up prices of products like furniture, toys, recreational goods (e.g., sports equipment), clothing, and audio equipment. Companies are less able to absorb tariff costs, as stockpiles have been depleted, which will negatively impact margins.

-

Food prices are expected to rise moderately (+0.4% m/m), mainly due to meat and imported goods.

-

Energy prices are likely to remain stable: gasoline may rebound +0.8% m/m after a -2.6% drop, electricity is forecast to rise +1%, while natural gas prices may fall -1%.

-

Service-sector price pressure is expected to ease, driven by deflationary trends in airfares, lodging (hotels), and leisure services.

Can the Macro Data Clear Up the Uncertainty?

Fed officials believe the full effects of the trade war may only be visible from August or even year-end. Meanwhile, many economists expect tariffs to impact prices already in today’s inflation report.

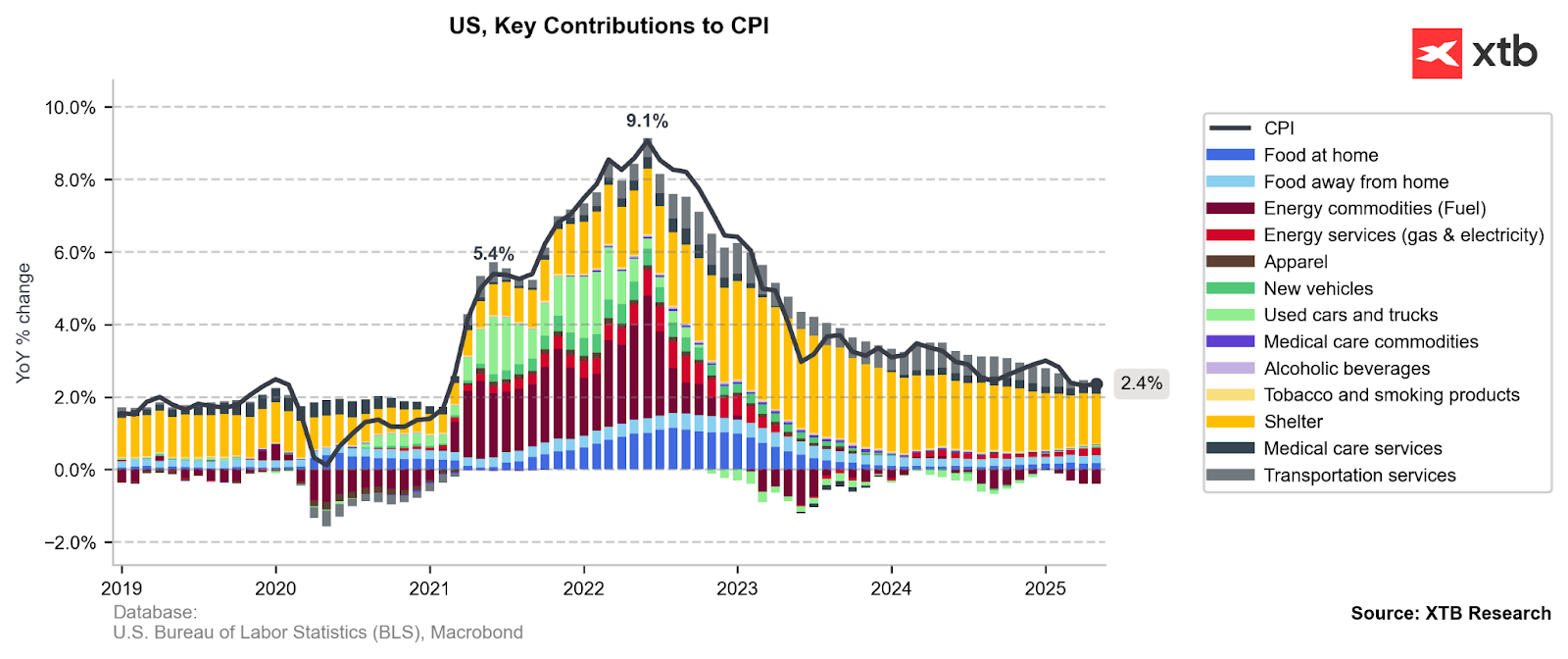

Rent prices remain the main contributor to U.S. inflation, and the trade war may affect the prices of imported goods, which will be in the spotlight today. That implies possible increases in other segments like used cars, new vehicles, alcoholic beverages, food products, and tobacco.

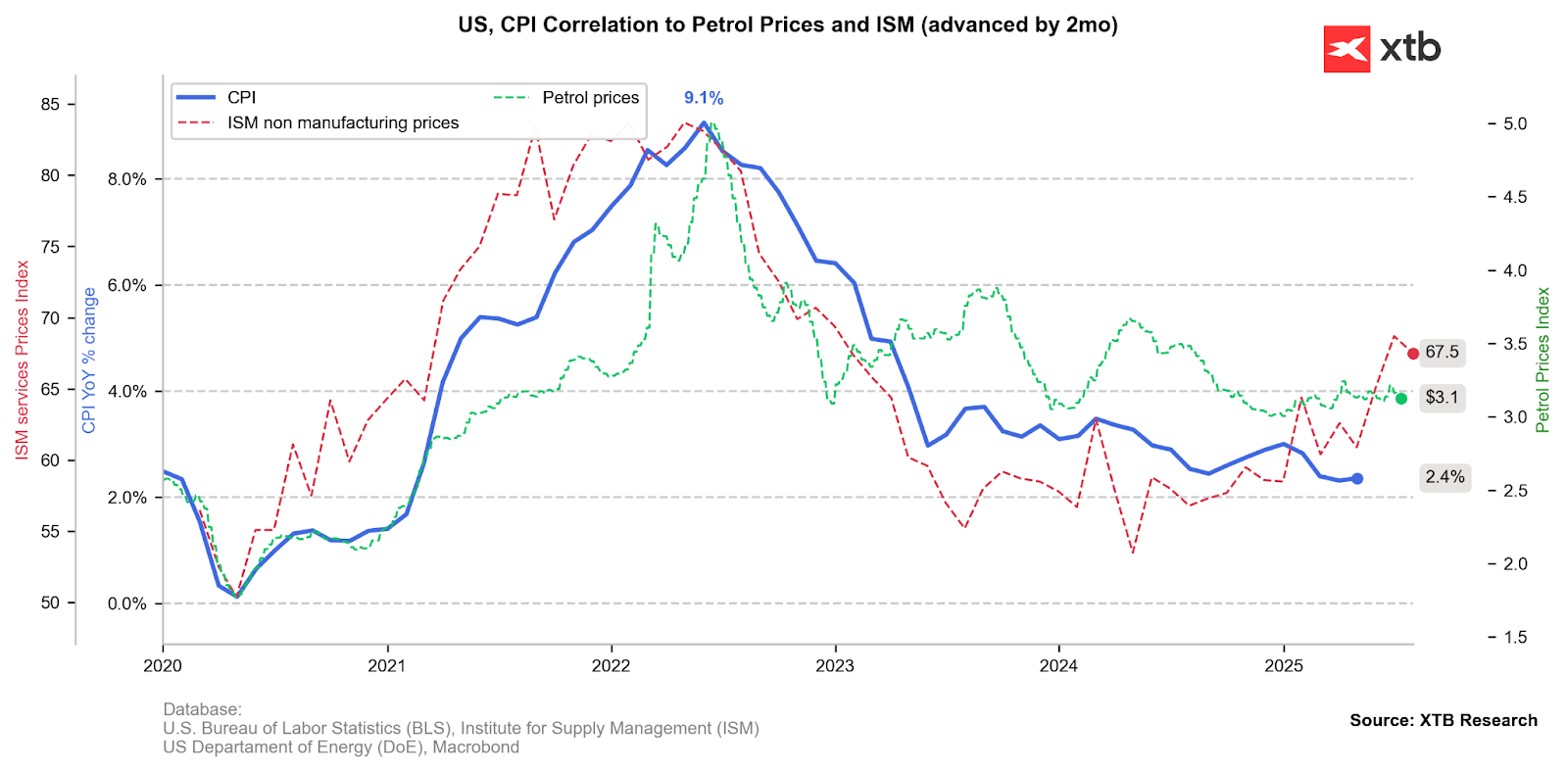

Even though fuel prices remain low and aren't currently a source of inflationary pressure, tariffs present a visible risk. In the latest ISM Services report, companies cited the trade war as the main factor behind elevated prices and costlier supply chain components. The price subindex remains high, though still significantly lower than during the COVID period.

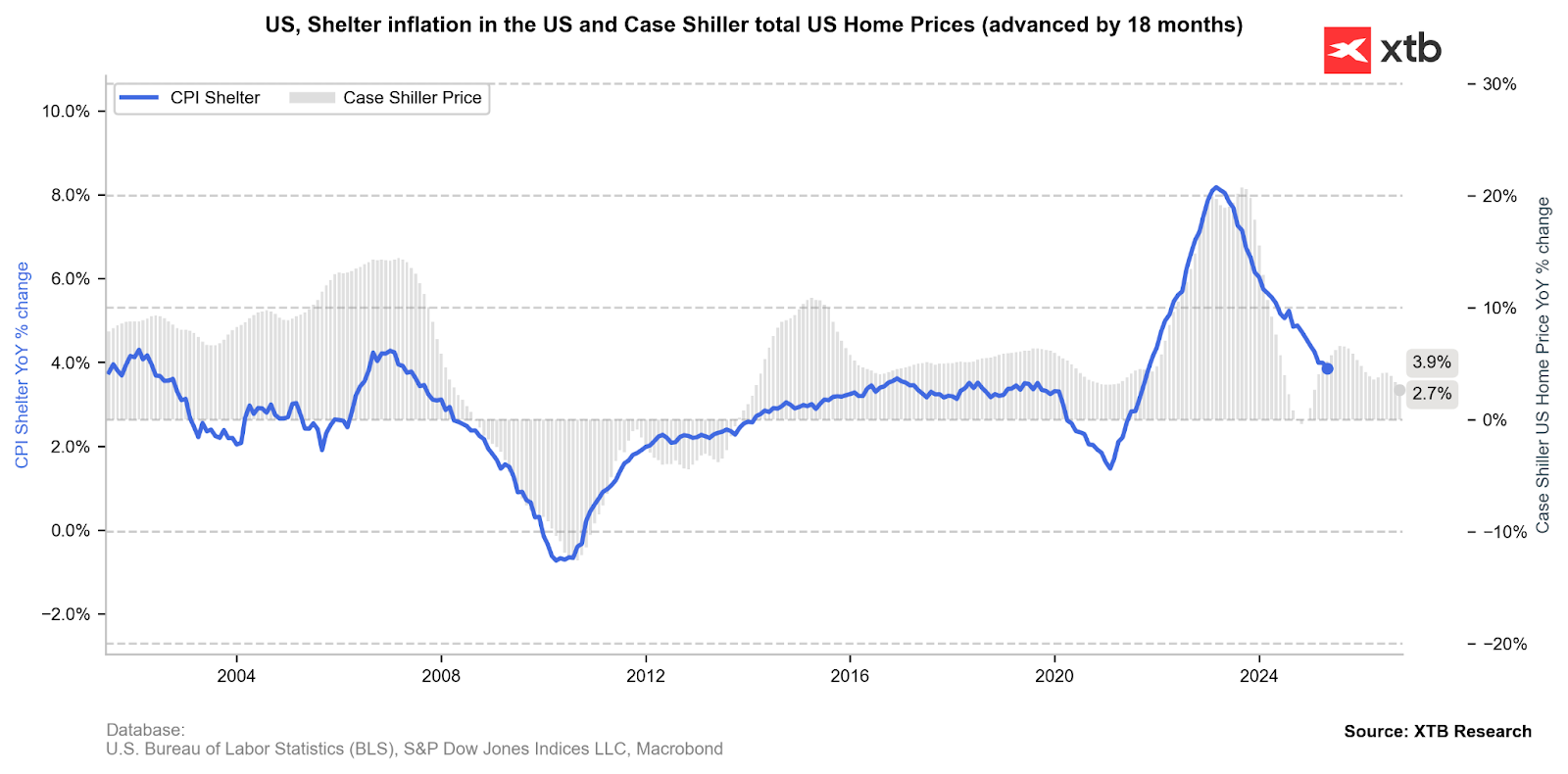

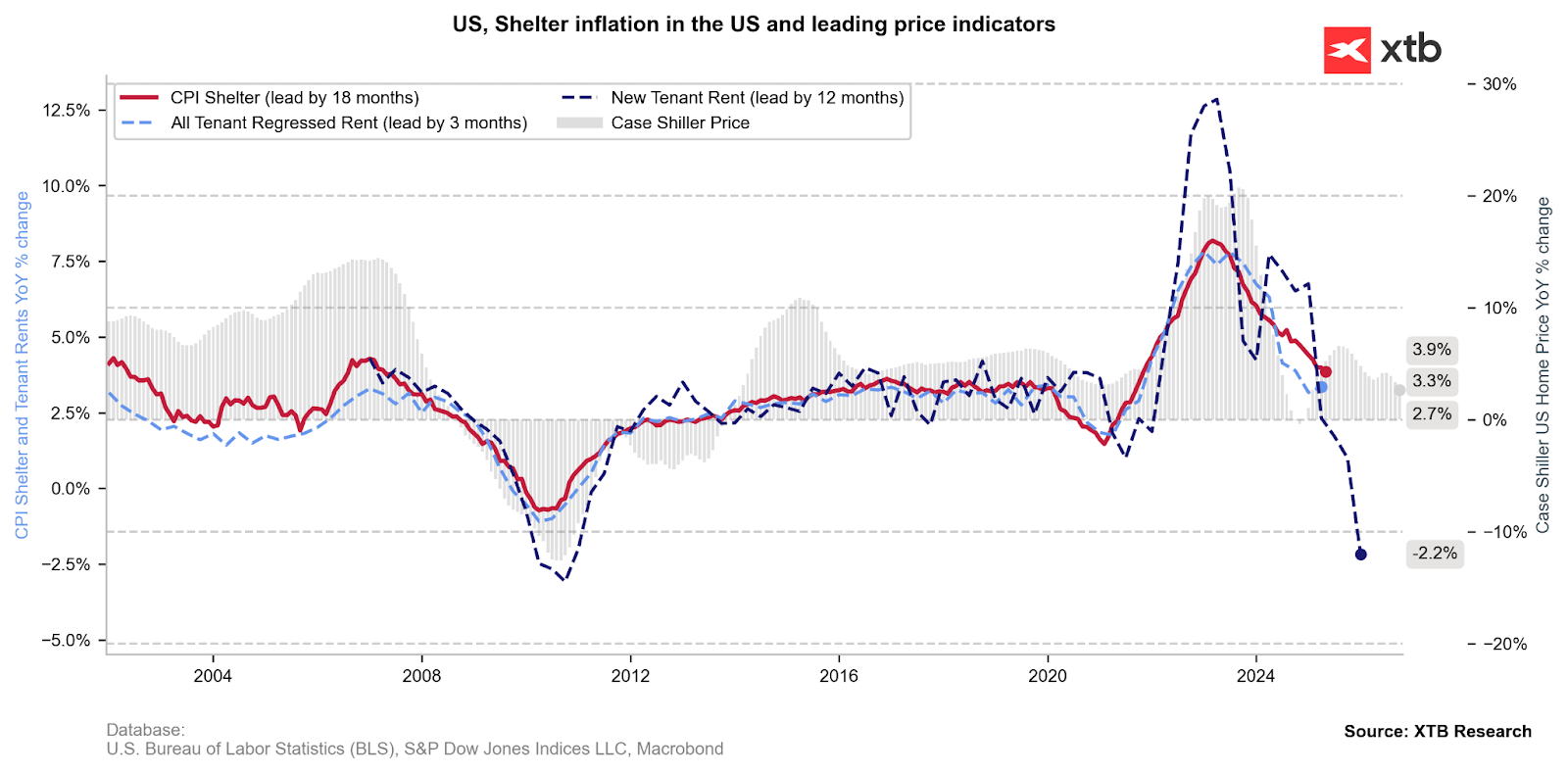

The largest contributor to inflation – shelter (rent) prices – is on a downward path, which should help deliver lower CPI prints in the coming months. New home price dynamics have also slowed and are now in neutral territory.

Rent prices for new leases are falling sharply. As the share of new leases grows, the CPI shelter component is expected to follow this trend.

EURUSD (H1 Chart)

The U.S. dollar is clearly weakening ahead of the CPI report. EURUSD gains are also supported by euro strength, with the pair up 0.18% today. However, given the local high near 1.18120, the current rate is still 1.25% below that level. A CPI surprise to the upside would reduce expectations of Fed rate cuts this year and could strengthen the dollar. But this would require a bigger upside surprise, as the move to 2.9% core inflation is already priced into consensus.

Source: xStation 5

Daily Summary: Wall Street Regains Ground; Another Intervention in the Yen Market❓

Three Markets to Watch Next Week (July 31, 2026)

Market Wrap: European equities at 3-week highs! Apple dips in US premarket!

Euro Area core inflation above estiamtes! EURUSD under key resistance!

The content of this report has been created by XTB S.A., with its registered office in Warsaw, at Prosta 67, 00-838 Warsaw, Poland, (KRS number 0000217580) and supervised by Polish Supervision Authority ( No. DDM-M-4021-57-1/2005). This material is a marketing communication within the meaning of Art. 24 (3) of Directive 2014/65/EU of the European Parliament and of the Council of 15 May 2014 on markets in financial instruments and amending Directive 2002/92/EC and Directive 2011/61/EU (MiFID II). Marketing communication is not an investment recommendation or information recommending or suggesting an investment strategy within the meaning of Regulation (EU) No 596/2014 of the European Parliament and of the Council of 16 April 2014 on market abuse (market abuse regulation) and repealing Directive 2003/6/EC of the European Parliament and of the Council and Commission Directives 2003/124/EC, 2003/125/EC and 2004/72/EC and Commission Delegated Regulation (EU) 2016/958 of 9 March 2016 supplementing Regulation (EU) No 596/2014 of the European Parliament and of the Council with regard to regulatory technical standards for the technical arrangements for objective presentation of investment recommendations or other information recommending or suggesting an investment strategy and for disclosure of particular interests or indications of conflicts of interest or any other advice, including in the area of investment advisory, within the meaning of the Trading in Financial Instruments Act of 29 July 2005 (i.e. Journal of Laws 2019, item 875, as amended). The marketing communication is prepared with the highest diligence, objectivity, presents the facts known to the author on the date of preparation and is devoid of any evaluation elements. The marketing communication is prepared without considering the client’s needs, his individual financial situation and does not present any investment strategy in any way. The marketing communication does not constitute an offer of sale, offering, subscription, invitation to purchase, advertisement or promotion of any financial instruments. XTB S.A. is not liable for any client’s actions or omissions, in particular for the acquisition or disposal of financial instruments, undertaken on the basis of the information contained in this marketing communication. In the event that the marketing communication contains any information about any results regarding the financial instruments indicated therein, these do not constitute any guarantee or forecast regarding the future results.