The pre-holiday closure of equity markets allows investors to catch their breath and step away from the relentless shifts in sentiment, currently rattled by the latest twists in the Iranian war. U.S. index futures are seeing a slight correction following yesterday’s highly volatile session, which—despite the panic triggered by Donald Trump’s address—ended with modest gains.

Paradoxically, despite the "holiday" on the stock market, volatility will not be in short supply. At 2:30 PM CET, the most critical report from the U.S. labour market, the Non-Farm Payrolls (NFP), will be released. This will be the "dot over the i" for the sentiment Federal Reserve members carry into their month-end interest rate meeting. With Wall Street closed, investor focus on the data will be heightened, potentially leading to significant swings in major, currently dormant currency pairs like EURUSD.

Source: XTB Research

What can we expect from today’s NFP report?

-

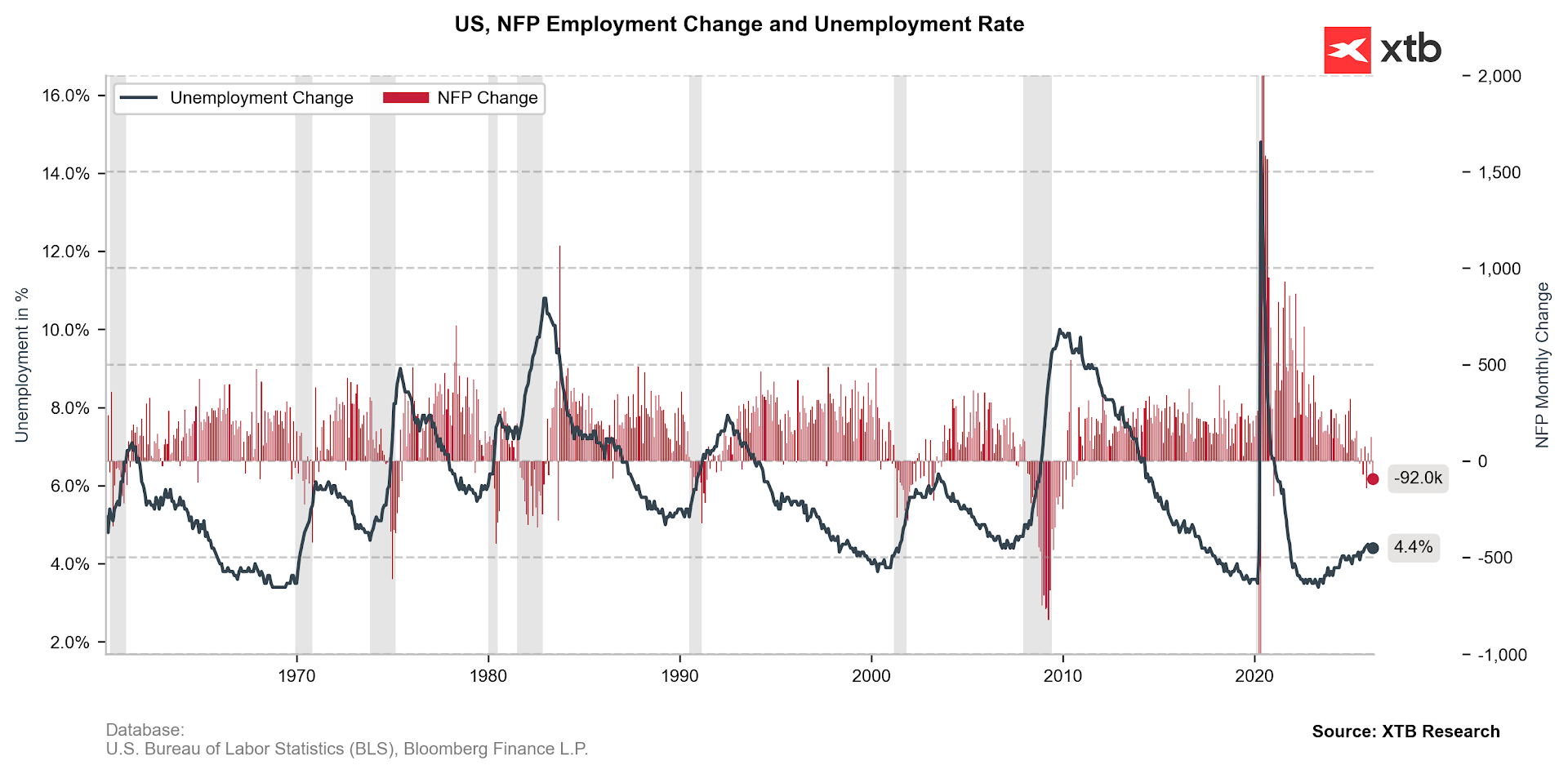

Payrolls: According to the Bloomberg consensus, U.S. payrolls are expected to increase by 65k in March, marking a rebound from the 92k decline in the previous month. In the private sector alone, employment is projected to bounce back by 70k, nearly erasing February’s 86k drop.

-

Unemployment Rate: Expected to remain unchanged at 4.4% following a surprise jump from 4.3%.

-

Average Hourly Earnings: Growth is expected to slow marginally from 0.3% to 0.2% (m/m) and from 3.8% to 3.7% (y/y).

The best surprise is no surprise

While the recent data was among the worst since the 2007-2008 crisis, it did not trigger panic due to its "one-off" nature. The correction primarily affected sectors that had previously seen massive gains (healthcare, education, construction), and the net effect in many categories remained positive. Mass strikes in healthcare also weighed on the numbers. Furthermore, unemployment remains at a historically low 4.4%, supported by stable jobless claims and steady ISM Employment readings despite surging price pressures.

Labour market stability highlights price concerns

Today’s data is particularly vital given the war in Iran and materializing fears of a long-term inflationary shock driven by energy prices. Following Donald Trump’s hawkish address, thin hopes for a quick de-escalation have evaporated. Risks of significant damage to energy infrastructure in the Persian Gulf and the murky status of the Strait of Hormuz have risen once again.

Labour stability will sharpen the Fed's focus on inflation. While U.S. CPI is certain to spike in the near term, the question remains whether the shock will be a one-time event or a persistent pressure that "eats into" food and service prices.

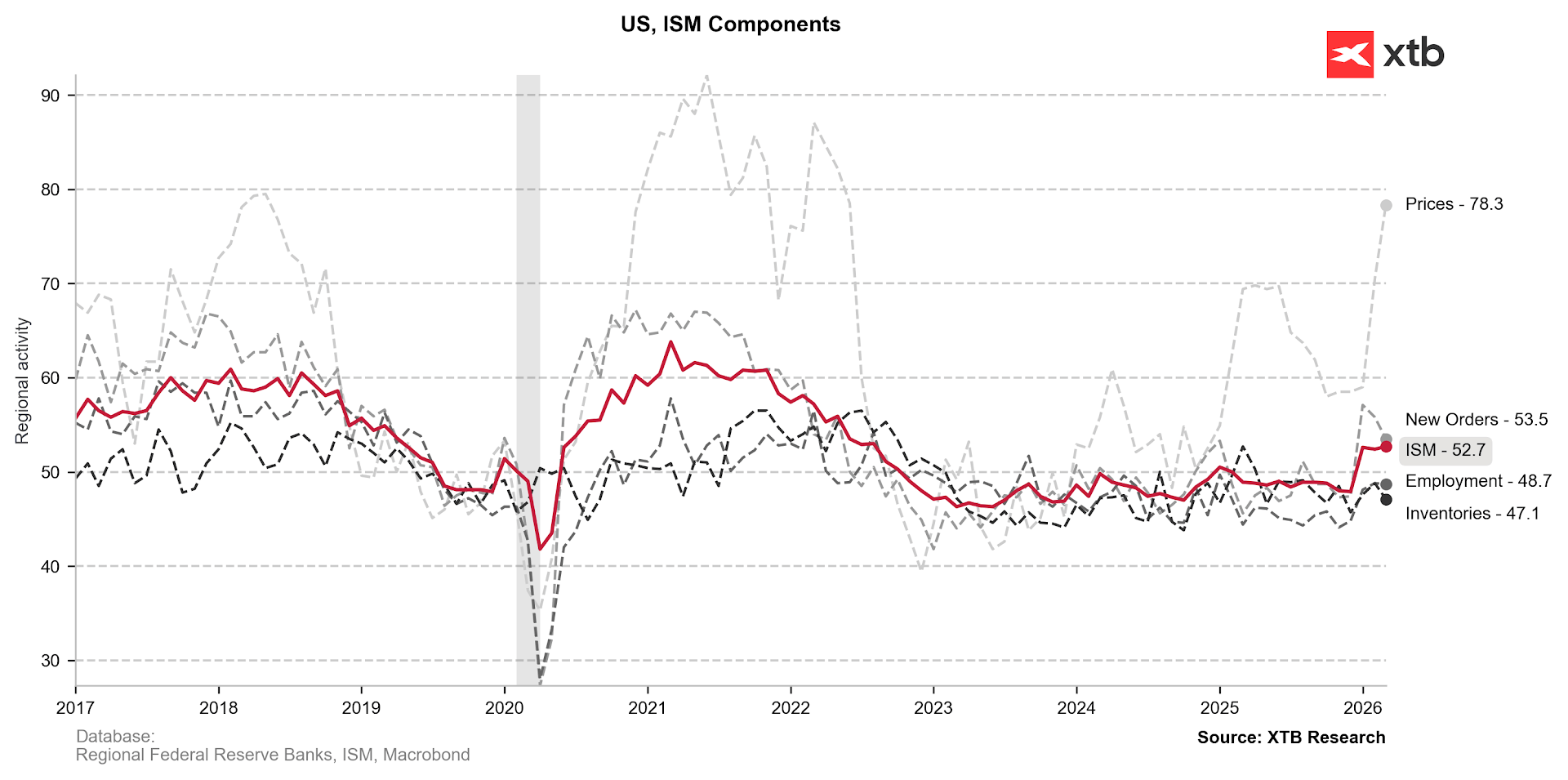

Recent ISM data primarily showed a drastic increase in price pressure. Source: XTB Research

Several FOMC members have already signaled heightened vigilance:

-

Alberto Musalem (St. Louis Fed): Sees potential for both cuts and hikes, suggesting the current policy is well-balanced (hinting at a prolonged pause).

-

Lorie Logan (Dallas Fed): Believes U.S. oil majors won't sacrifice margins to save consumers, and Iranian risks could force the Fed to pivot in the opposite direction (hinting at readiness for hikes).

-

Michelle Bowman (Governor): Remains dovish, still eyeing three cuts by the end of 2026. However, her argument relies on labour market concerns. If NFP aligns with the recently strong ADP report, labour worries may take a backseat during the April FOMC meeting.

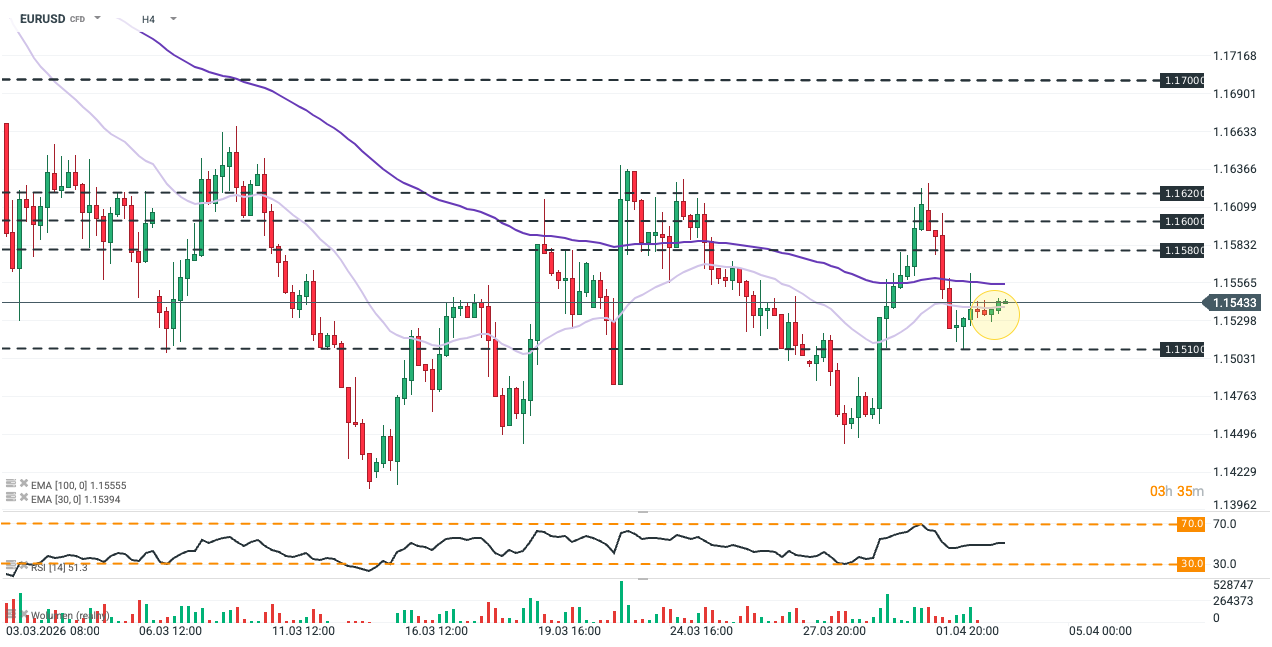

EURUSD (H4)

Since the outbreak of the war in Iran, EURUSD has remained clearly capped at the 1.162 level. Friday’s calm is helping the pair recover some ground lost after Trump’s speech, but a return to local highs is unlikely given NFP expectations. Only significantly weaker data could lead to a test of 1.1580, though a breach of the broader consolidation remains improbable.

Source: xStation5

The semiconductors sell-off continues 📉

US OPEN: Deeper sell-off and a SaaS rebound

The coffee market in the grip of weather and empty warehouses: The paradox of record Brazil harvests

Chart of the Day: Who suffers from the oil price drop? (28.07.2026)

The content of this report has been created by XTB S.A., with its registered office in Warsaw, at Prosta 67, 00-838 Warsaw, Poland, (KRS number 0000217580) and supervised by Polish Supervision Authority ( No. DDM-M-4021-57-1/2005). This material is a marketing communication within the meaning of Art. 24 (3) of Directive 2014/65/EU of the European Parliament and of the Council of 15 May 2014 on markets in financial instruments and amending Directive 2002/92/EC and Directive 2011/61/EU (MiFID II). Marketing communication is not an investment recommendation or information recommending or suggesting an investment strategy within the meaning of Regulation (EU) No 596/2014 of the European Parliament and of the Council of 16 April 2014 on market abuse (market abuse regulation) and repealing Directive 2003/6/EC of the European Parliament and of the Council and Commission Directives 2003/124/EC, 2003/125/EC and 2004/72/EC and Commission Delegated Regulation (EU) 2016/958 of 9 March 2016 supplementing Regulation (EU) No 596/2014 of the European Parliament and of the Council with regard to regulatory technical standards for the technical arrangements for objective presentation of investment recommendations or other information recommending or suggesting an investment strategy and for disclosure of particular interests or indications of conflicts of interest or any other advice, including in the area of investment advisory, within the meaning of the Trading in Financial Instruments Act of 29 July 2005 (i.e. Journal of Laws 2019, item 875, as amended). The marketing communication is prepared with the highest diligence, objectivity, presents the facts known to the author on the date of preparation and is devoid of any evaluation elements. The marketing communication is prepared without considering the client’s needs, his individual financial situation and does not present any investment strategy in any way. The marketing communication does not constitute an offer of sale, offering, subscription, invitation to purchase, advertisement or promotion of any financial instruments. XTB S.A. is not liable for any client’s actions or omissions, in particular for the acquisition or disposal of financial instruments, undertaken on the basis of the information contained in this marketing communication. In the event that the marketing communication contains any information about any results regarding the financial instruments indicated therein, these do not constitute any guarantee or forecast regarding the future results.