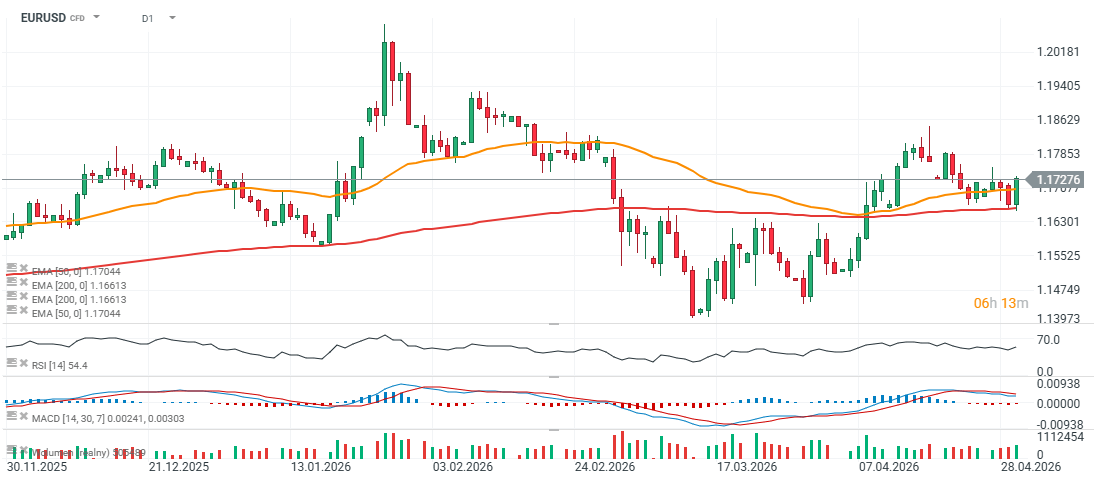

EURUSD pair is surging almost 0.5% today rising to almost 1.173 amid weakeing US dollar, falling treasuries yields and strong risk appetite on Wall Street. ECB holded interest rates unchanged on today meeting, signalling that price pressure from the energy markets may lead to rising and destabilized energy markets even with the Iran conflict will end. Of course, this adds more uncertainty and may slow the European economy. The bank will watch not only inflation itself but rather markets and consumer respons to that, which make further interest rate hikes in eurozone highly uncertaint. However, todays US macro data were not very strong.

Growth disappointed slightly, with GDP at 2.0% vs 2.3% expected, but the consumer remains firm: nominal spending rose 0.9% MoM, while income growth surprised to the upside. The labor market also looks tight, with jobless claims clearly below expectations. The bigger issue is inflation. Headline PCE remains elevated, core PCE was firmer than expected on the advance measure, and the Employment Cost Index accelerated to 0.9%, suggesting wage pressure has not fully cooled. Overall, this is not a recessionary print, but it is also not clearly disinflationary. For the Fed, the data support a cautious stance and reduce the urgency for near-term rate cuts.

US macro data for today

- US GDP Growth (QoQ, annualized): 2.0% vs 2.3% expected, 0.5% prior

- US GDP Price Index: 3.6% vs 3.9% expected, 3.7% prior

- US GDP Deflator SA Advance: 3.6% vs 3.6% expected, 3.7% prior

- US PCE Prices Advance: 4.5% vs 4.5% expected, 2.9% prior

- US Core PCE Prices Advance: 4.3% vs 4.1% expected, 2.7% prior

- US PCE Price Index YoY: 3.5% vs 3.5% expected, 2.8% prior

- US PCE Price Index MoM: 0.7% vs 0.7% expected, 0.4% prior

- US Core PCE Price Index YoY: 3.2% vs 3.2% expected, 3.0% prior

- US Core PCE Price Index MoM: 0.3% vs 0.3% expected, 0.4% prior

- US Consumer Spending MoM: 0.9% vs 0.9% expected, 0.5% prior

- US Personal Income MoM: 0.6% vs 0.3% expected, -0.1% prior

- US Real Personal Consumption MoM: 0.2% vs 0.3% expected, 0.1% prior

- US Initial Jobless Claims: 189K vs 212K expected, 214K prior

- US Continuing Jobless Claims: 1.785M vs 1.815M expected, 1.821M prior

- US Employment Cost Index: 0.9% vs 0.8% expected, 0.7% prior

EURUSD (D1 interval)

Source: xStation5

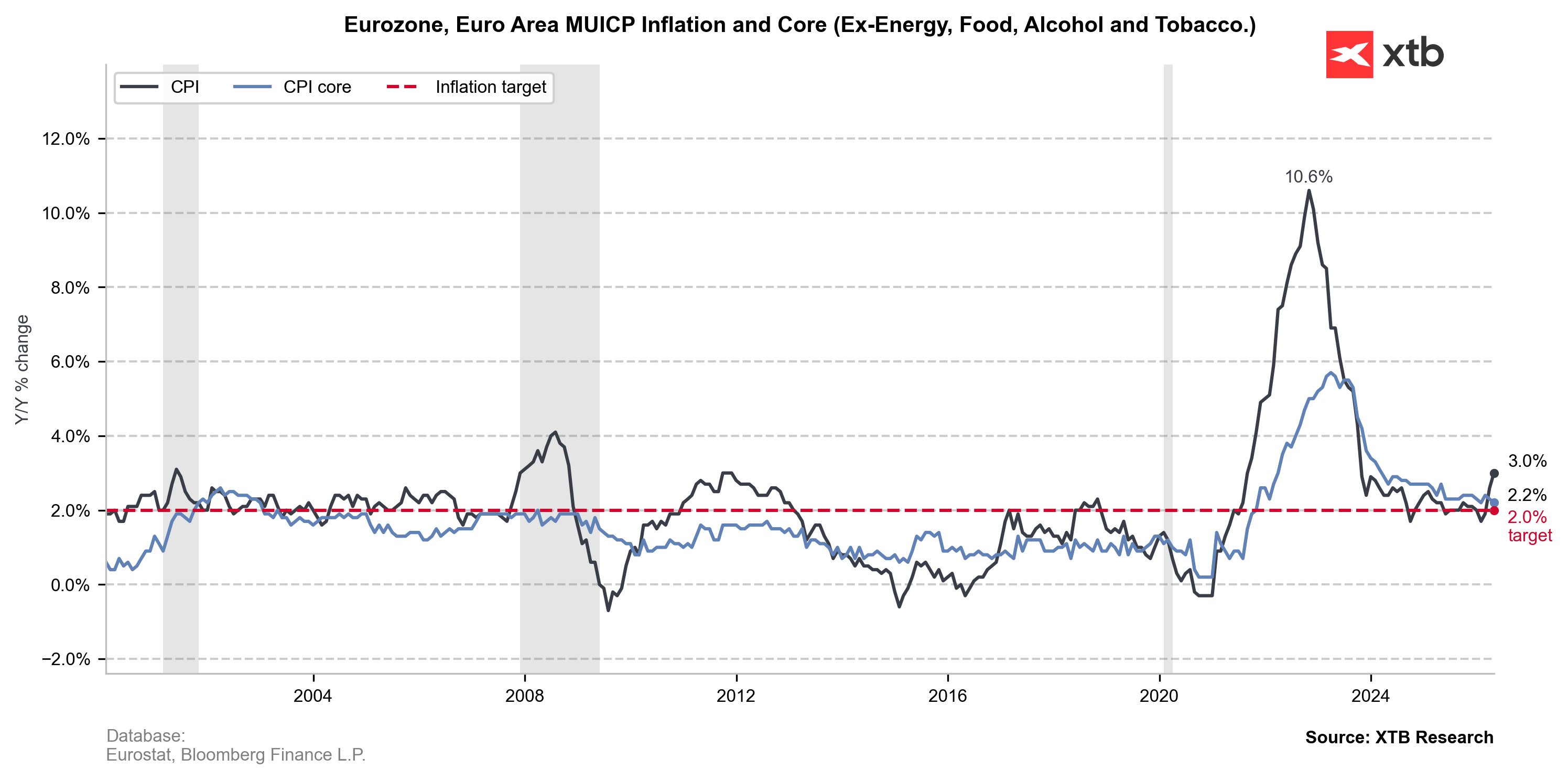

Eurozone inflation is rising again and if European consumers will show resilience - ECB interest rate hikes are not "off the table".

Source: XTB Research, ECB, Macrobond

China Is Building Its Own Chip-Making Machines. ASML Under Pressure as the Technology War Enters a New Phase

US Open: Wall Street Rebounds After US Iran Ceasefire

🔴European TTF gas prices fall by 7.5%

Economic Calendar: What you need to watch closely this week❓ (27.07.2026)

The content of this report has been created by XTB S.A., with its registered office in Warsaw, at Prosta 67, 00-838 Warsaw, Poland, (KRS number 0000217580) and supervised by Polish Supervision Authority ( No. DDM-M-4021-57-1/2005). This material is a marketing communication within the meaning of Art. 24 (3) of Directive 2014/65/EU of the European Parliament and of the Council of 15 May 2014 on markets in financial instruments and amending Directive 2002/92/EC and Directive 2011/61/EU (MiFID II). Marketing communication is not an investment recommendation or information recommending or suggesting an investment strategy within the meaning of Regulation (EU) No 596/2014 of the European Parliament and of the Council of 16 April 2014 on market abuse (market abuse regulation) and repealing Directive 2003/6/EC of the European Parliament and of the Council and Commission Directives 2003/124/EC, 2003/125/EC and 2004/72/EC and Commission Delegated Regulation (EU) 2016/958 of 9 March 2016 supplementing Regulation (EU) No 596/2014 of the European Parliament and of the Council with regard to regulatory technical standards for the technical arrangements for objective presentation of investment recommendations or other information recommending or suggesting an investment strategy and for disclosure of particular interests or indications of conflicts of interest or any other advice, including in the area of investment advisory, within the meaning of the Trading in Financial Instruments Act of 29 July 2005 (i.e. Journal of Laws 2019, item 875, as amended). The marketing communication is prepared with the highest diligence, objectivity, presents the facts known to the author on the date of preparation and is devoid of any evaluation elements. The marketing communication is prepared without considering the client’s needs, his individual financial situation and does not present any investment strategy in any way. The marketing communication does not constitute an offer of sale, offering, subscription, invitation to purchase, advertisement or promotion of any financial instruments. XTB S.A. is not liable for any client’s actions or omissions, in particular for the acquisition or disposal of financial instruments, undertaken on the basis of the information contained in this marketing communication. In the event that the marketing communication contains any information about any results regarding the financial instruments indicated therein, these do not constitute any guarantee or forecast regarding the future results.