Goldman Sachs has published an insightful report indicating that US stock purchases have increased at their fastest pace in 6 months. Does this signify unequivocal enthusiasm among institutional investors for the US stock market?

Market sentiment is deeply uneven; market purchases are primarily ETFs and stocks. However, an important detail not easily found in the report, as Bloomberg analyses indicate, is that stock purchases are largely "short cover" trades, meaning buying shares to limit losses from short positions (selling).

The local peak for long positions (open interest) among asset managers (according to TFF) occurred in 2024, when it stood at approximately 27%. A few months ago, it was still nearly 25%, but today it has fallen to around 15%.

Based on Goldman Sachs data, three negative trends are visible across three different sectors.

- Finance - Allocation has increased sixfold, yet total allocation remains at 5-year lows. Importantly, almost the entire exposure to the sector consists of banks.

- Industry - Pessimism persists regarding American industry. Net declines were seen in 7 out of the last 8 weeks, and short positions in this sector are at their highest since 2024.

- Semiconductors - Following fantastic gains, many institutions (including Goldman) declared they were liquidating a large portion of their positions in this industry.

Does this mean inevitable declines?

No, although it points to a clear problem. The properties and conditions present in today's derivatives market ensure that corrections are shallow and gains are pronounced.

Low "paper" volatility masks real risks. Fund managers remain positive, but this sentiment is running out of fuel. Currently, the market lives on increasingly unrealistic dreams of a swift end to the conflict in Iran and increasingly esoteric returns on AI investments.

Given the indicators and current levels, the market is currently exposing itself to a devastating correction the moment the target macroeconomic scenario clearly changes.

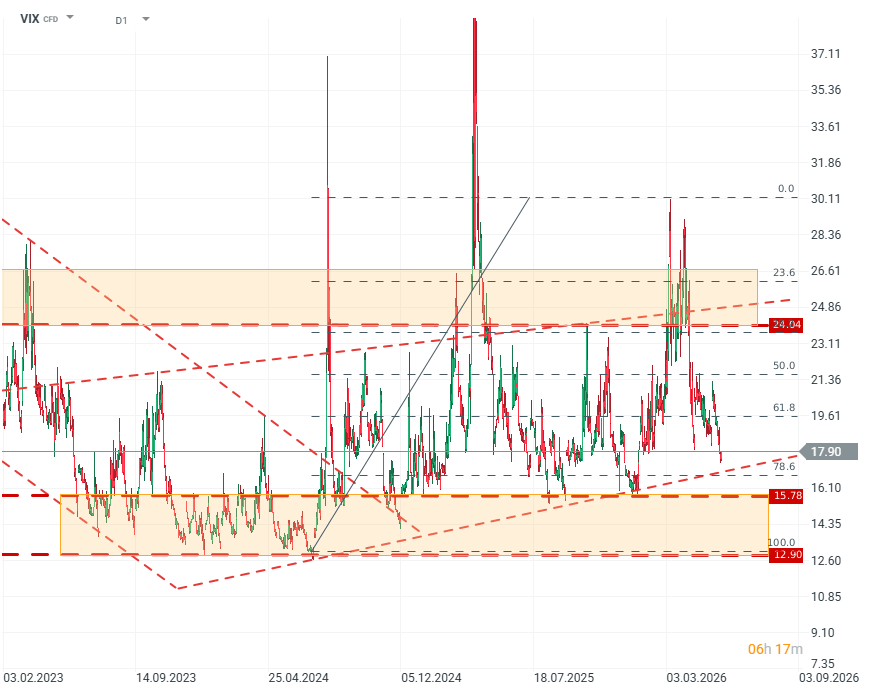

VIX (D1)

The volatility index (VIX) is currently indicating the lower limit of the channel in which it has been moving since around 2024. Source: xStation5

Chart of the day: DE40 hold near ATH! Siemens and Deutsche Telekom shine with earnings!

Economic Calendar: Could Smaller Job Reports Pressure Fed to Hike?

Morning Wrap: Equities under pressure after Wall Street took profits, FX frozen (06.08.2026)

Daily Summary: Dow Jones hits record highs, while gold and silver rally on hopes for a US–Iran deal

The content of this report has been created by XTB S.A., with its registered office in Warsaw, at Prosta 67, 00-838 Warsaw, Poland, (KRS number 0000217580) and supervised by Polish Supervision Authority ( No. DDM-M-4021-57-1/2005). This material is a marketing communication within the meaning of Art. 24 (3) of Directive 2014/65/EU of the European Parliament and of the Council of 15 May 2014 on markets in financial instruments and amending Directive 2002/92/EC and Directive 2011/61/EU (MiFID II). Marketing communication is not an investment recommendation or information recommending or suggesting an investment strategy within the meaning of Regulation (EU) No 596/2014 of the European Parliament and of the Council of 16 April 2014 on market abuse (market abuse regulation) and repealing Directive 2003/6/EC of the European Parliament and of the Council and Commission Directives 2003/124/EC, 2003/125/EC and 2004/72/EC and Commission Delegated Regulation (EU) 2016/958 of 9 March 2016 supplementing Regulation (EU) No 596/2014 of the European Parliament and of the Council with regard to regulatory technical standards for the technical arrangements for objective presentation of investment recommendations or other information recommending or suggesting an investment strategy and for disclosure of particular interests or indications of conflicts of interest or any other advice, including in the area of investment advisory, within the meaning of the Trading in Financial Instruments Act of 29 July 2005 (i.e. Journal of Laws 2019, item 875, as amended). The marketing communication is prepared with the highest diligence, objectivity, presents the facts known to the author on the date of preparation and is devoid of any evaluation elements. The marketing communication is prepared without considering the client’s needs, his individual financial situation and does not present any investment strategy in any way. The marketing communication does not constitute an offer of sale, offering, subscription, invitation to purchase, advertisement or promotion of any financial instruments. XTB S.A. is not liable for any client’s actions or omissions, in particular for the acquisition or disposal of financial instruments, undertaken on the basis of the information contained in this marketing communication. In the event that the marketing communication contains any information about any results regarding the financial instruments indicated therein, these do not constitute any guarantee or forecast regarding the future results.