- BoE is expected to cut interest rates third time in current cycle

- The GBP/USD remains elevated due to the weakening of the U.S. dollar, driven by the partial removal of tariffs by the U.S. However, in recent weeks, Donald Trump has not mentioned the UK in the context of tariffs.

- At the same time, the UK economy is struggling, which could work against the pound.

Central Banks in Times of Uncertainty

Tariffs imposed by Donald Trump significantly increase uncertainty among all central bankers worldwide. Tariffs—whether direct or indirect—pose a threat in the form of rising inflation and economic slowdown. As a result, central banks adopt a stance of uncertainty, as seen in the case of the Bank of Canada, the Fed, or even the ECB. A similar situation may occur with the BoE. Although the weakness of the economy suggests a continuation of interest rate cuts and today’s move is priced in almost 100%, we still cannot be certain about the future.

However, today interest rates should be cut by 25 basis points. This means that after today’s move, the main interest rate will drop from the current 4.75% to 4.5%.

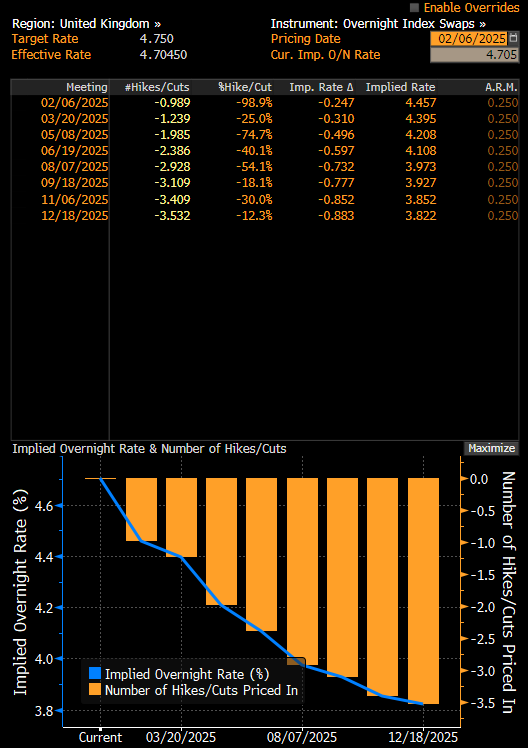

Today, the market is almost fully pricing in a move from the Bank of England. However, the key issue is what path British bankers expect in the coming months. Source: Bloomberg Finance LP

A Mixed Economic Picture

The British economy has not been in good shape for a long time. Although the beginning of 2024 was promising, we have essentially been observing flat economic growth recently. This indicates that some bankers are in favor of more aggressive cuts, while others still see significant inflationary risks. It is worth mentioning that today we will also receive the latest inflation projections, which may give us a better idea of the Bank of England’s plans. Most likely, the BoE will raise inflation expectations for the future and lower growth forecasts, putting future decisions into question. Nevertheless, we expect that at least for now, the BoE will stick to its plan of continuing quarterly interest rate cuts.

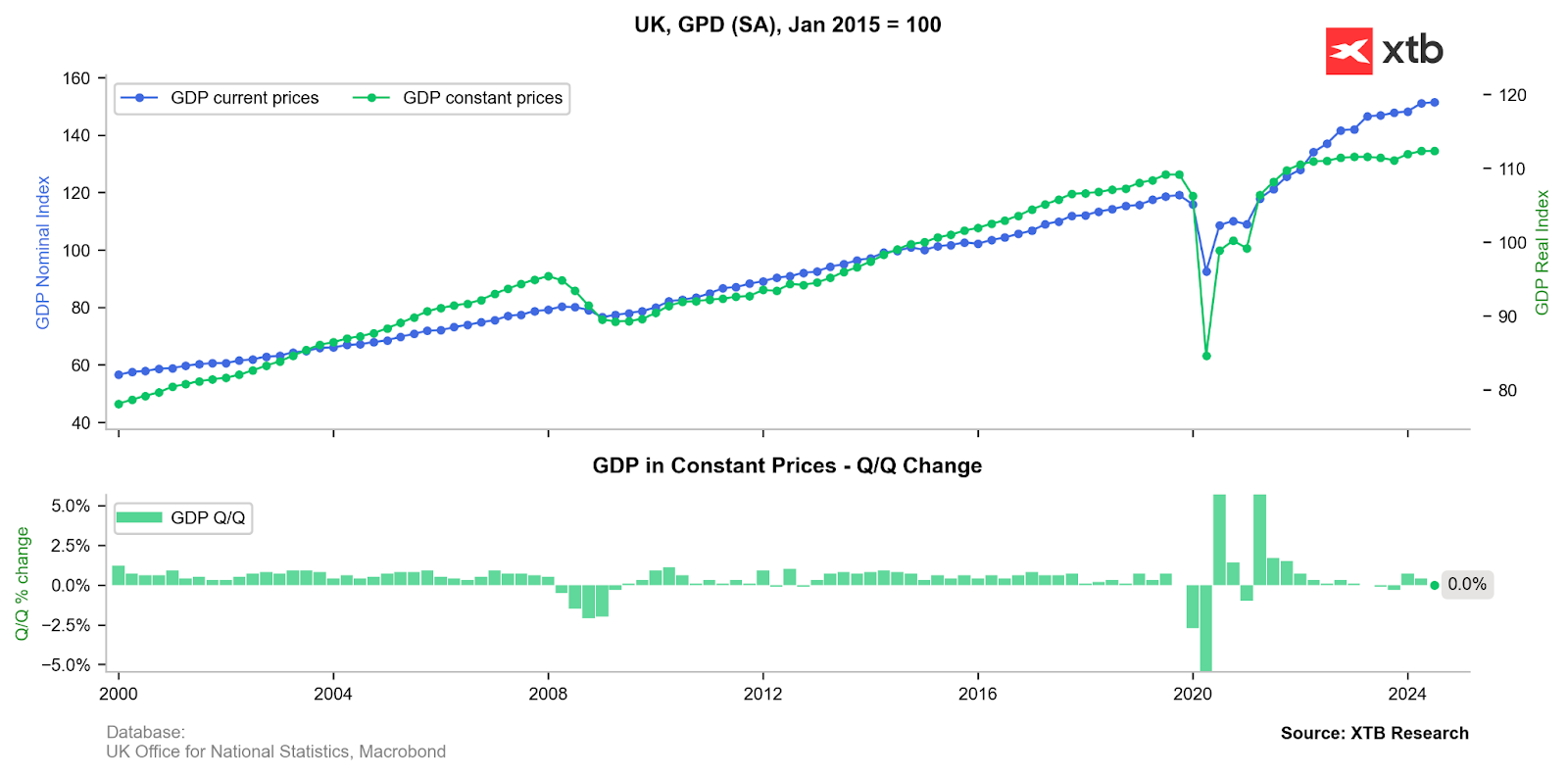

Economic growth in the United Kingdom looks very weak. Looking at key economic components, the situation does not appear optimistic. Source: Bloomberg Finance LP, XTB

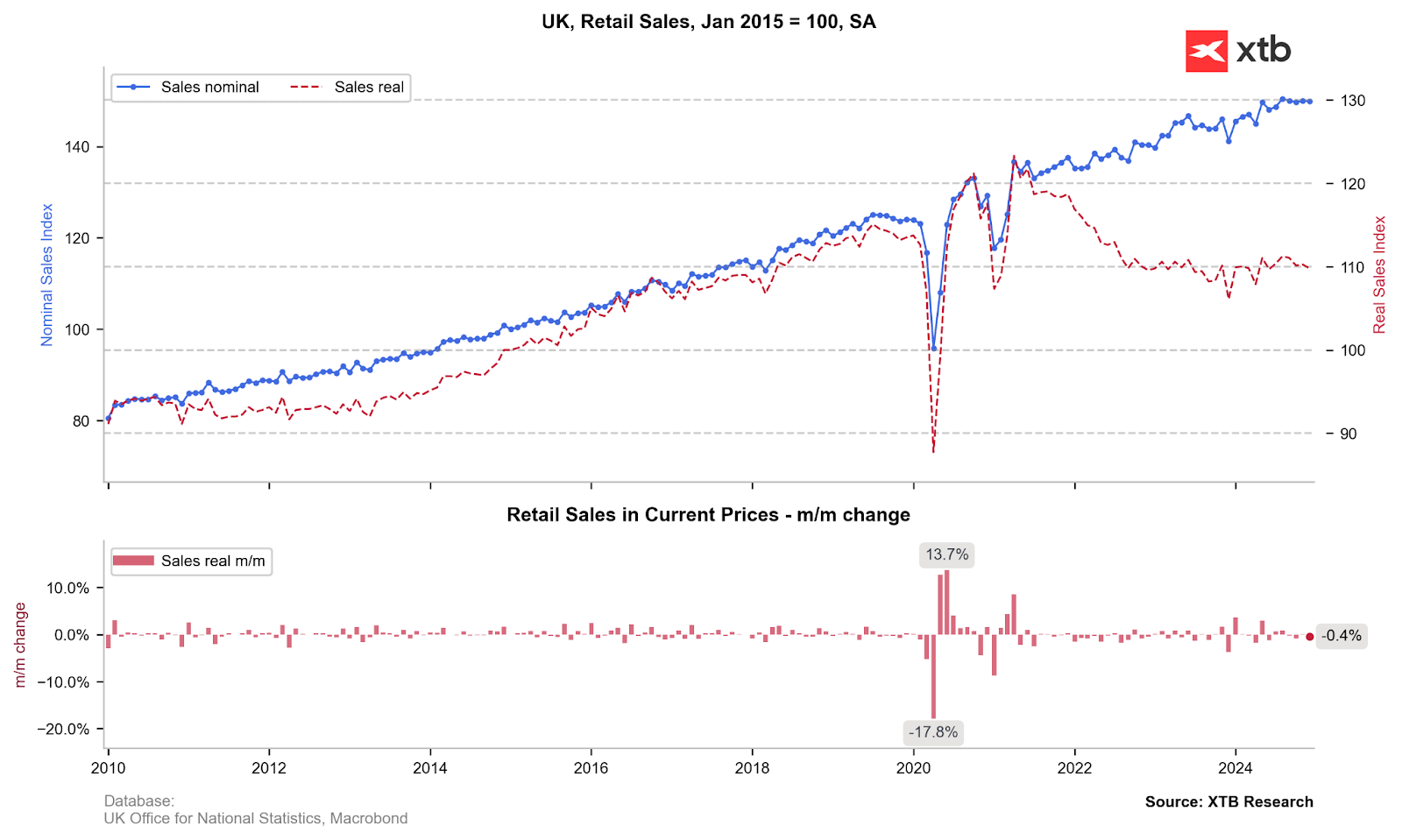

Retail sales have been struggling with growth for several months and remain flat. In real terms, we are observing a decline. Source: Bloomberg Finance LP, XTB

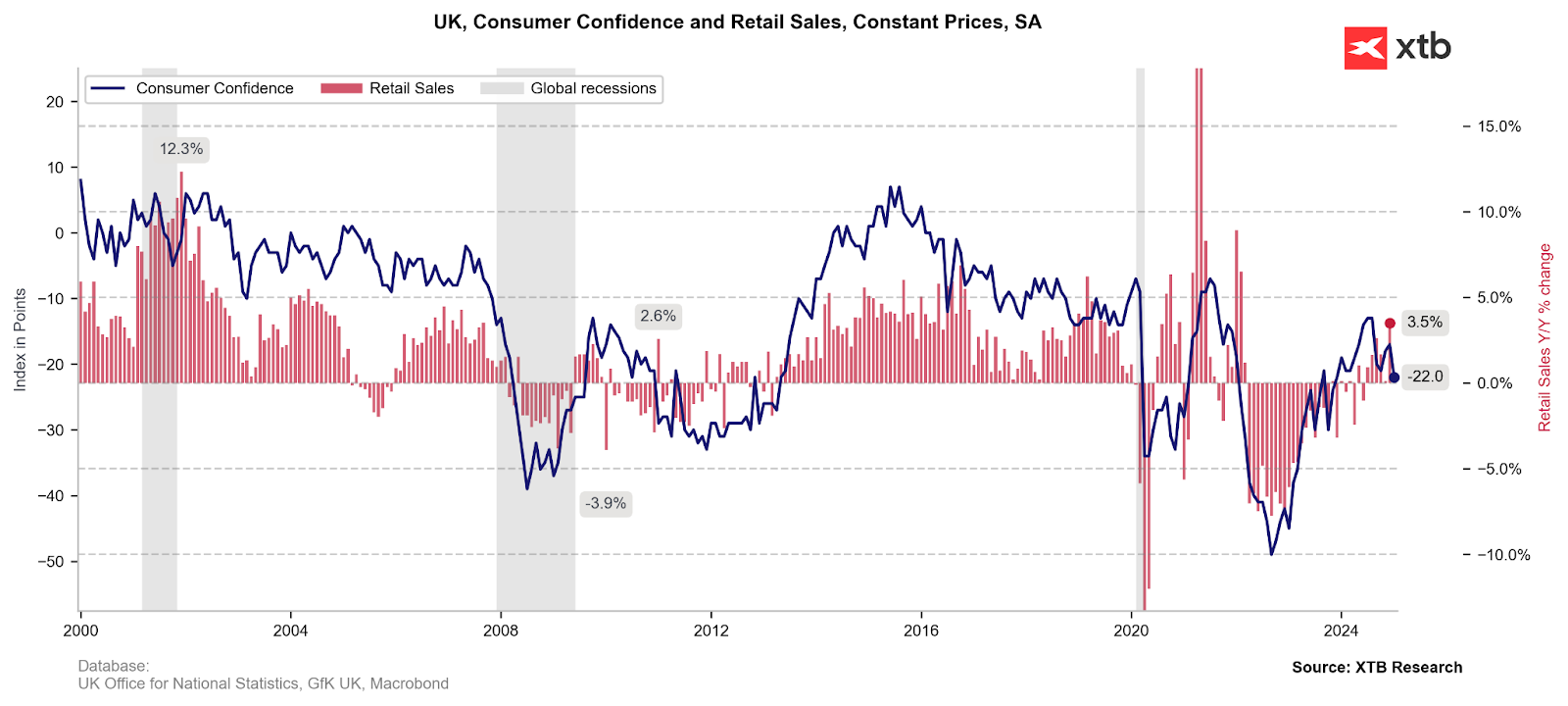

Although retail sales saw a strong year-over-year increase, this was due to a low base effect. Consumer sentiment is the worst it has been in several months. Source: Bloomberg Finance LP, XTB

Industrial production is returning to declines, and leading indicators suggest an even worse outlook. Source: Bloomberg Finance LP, XTB

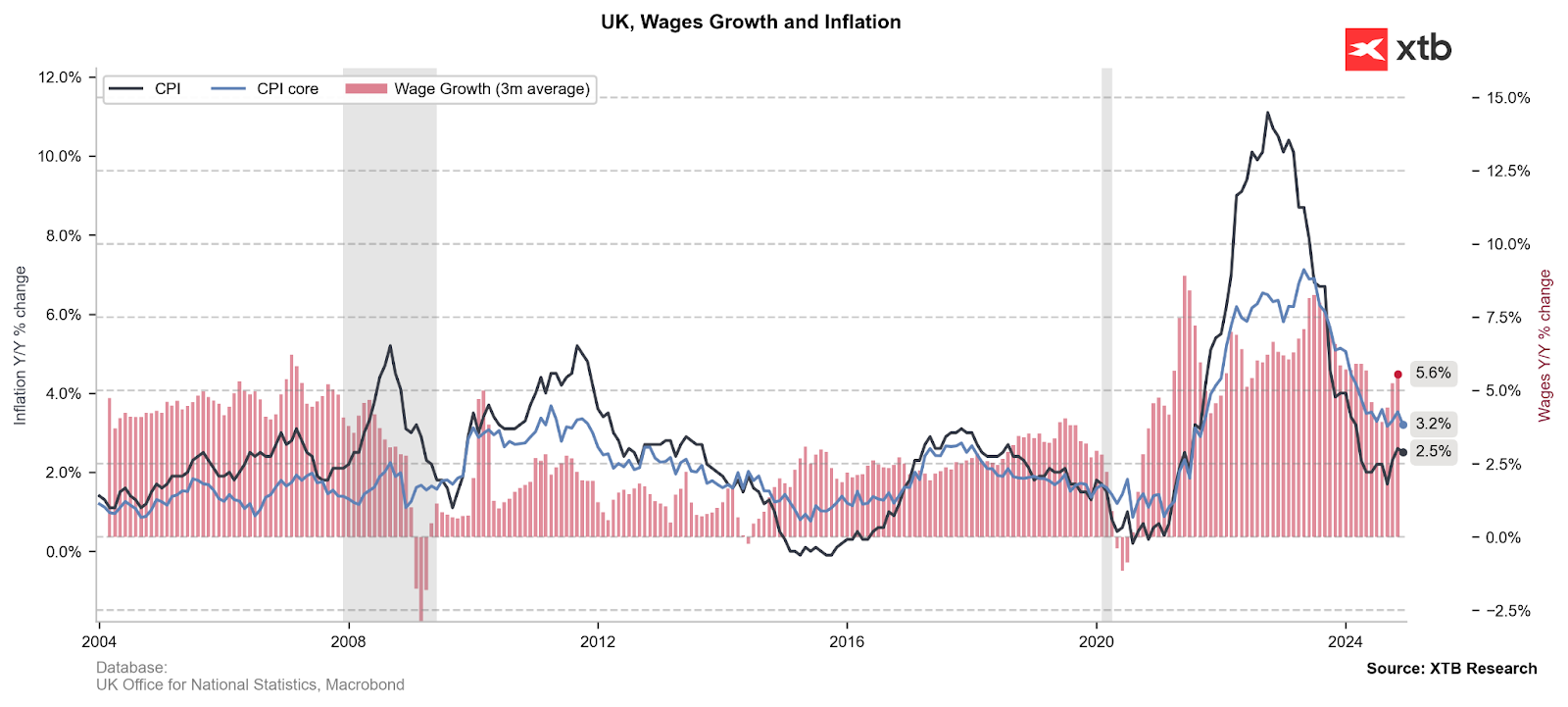

Inflation will most likely rebound in January, not only due to higher energy costs but also wage factors. The BoE is expected to raise its inflation projections. Source: Bloomberg Finance LP, XTB

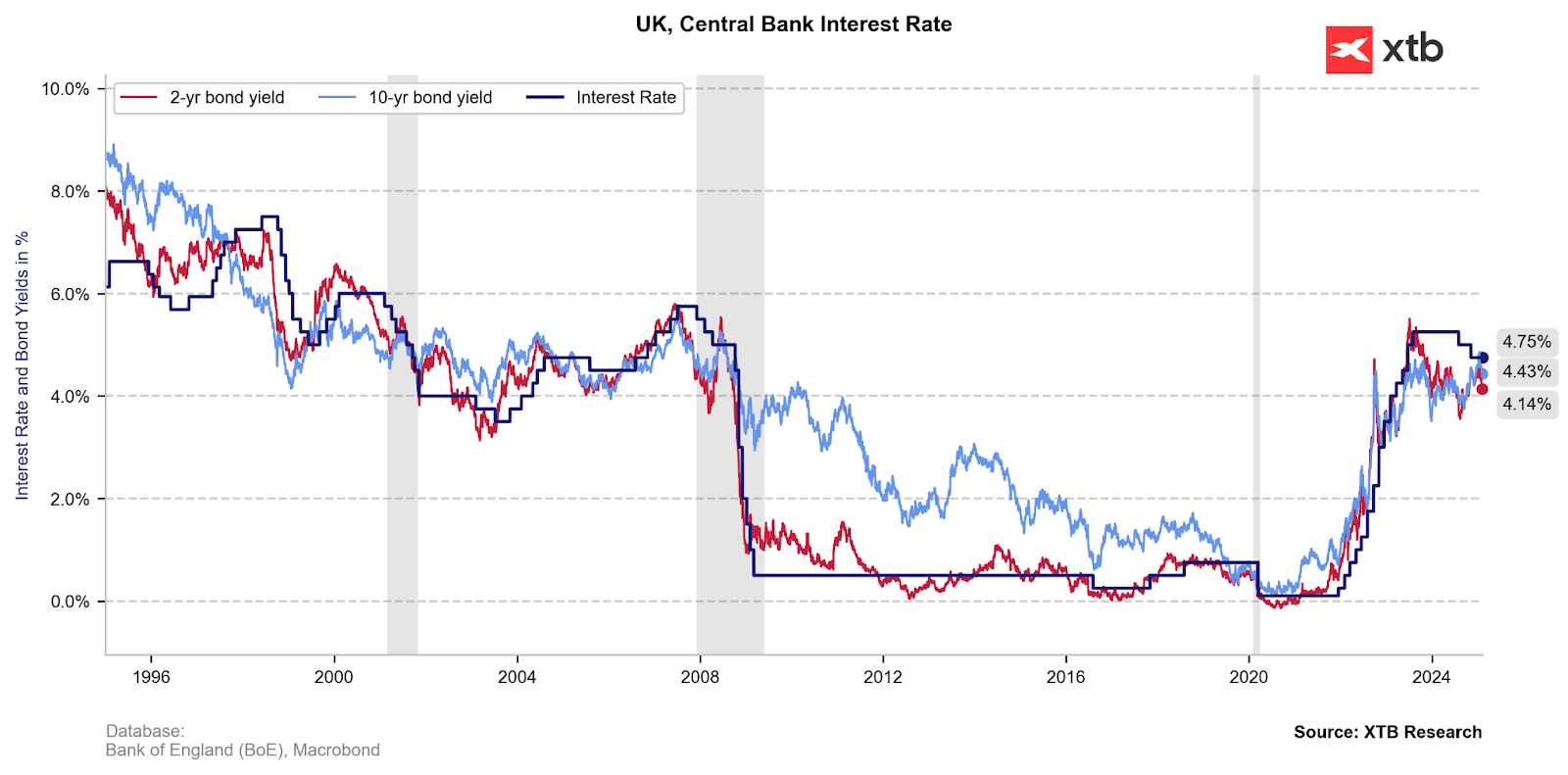

Bond yields have fallen slightly recently, which may no longer provide strong support for the pound. Source: Bloomberg Finance LP, XTB

How Will the Market React?

The British pound is retreating today ahead of the decision. The economy appears to be in weak condition, potentially increasing the chances of a more dovish stance from the bank. At the same time, however, there are significant inflation risks. Projections may ultimately determine the next moves for the British pound. Additionally, tariff-related risks will contribute to the highest volatility. Even if Trump does not impose tariffs on the UK but decides to implement tariffs on the EU, it will have an even greater impact on the UK economy. As a result, the GBP/USD pair remains vulnerable to potential declines. On the other hand, if the bank indicates that it is pausing further cuts due to uncertainty, it is not out of the question that the GBP/USD pair could attempt to test the 1.2575 area in the near future.

Source: xStation5

Eurozone PMIs: German Factory Revival Masks Underlying Stagnation 🇪🇺

Chart of the Day: Yen Falls From 40-Year Highs – What’s Next? (03.08.2026)

Economic Calendar: What Could Move the Market This Week? (03.08.2026)

Morning Wrap: USA Halts Strikes – Oil Down, Stocks Up (03.08.2026)

The content of this report has been created by XTB S.A., with its registered office in Warsaw, at Prosta 67, 00-838 Warsaw, Poland, (KRS number 0000217580) and supervised by Polish Supervision Authority ( No. DDM-M-4021-57-1/2005). This material is a marketing communication within the meaning of Art. 24 (3) of Directive 2014/65/EU of the European Parliament and of the Council of 15 May 2014 on markets in financial instruments and amending Directive 2002/92/EC and Directive 2011/61/EU (MiFID II). Marketing communication is not an investment recommendation or information recommending or suggesting an investment strategy within the meaning of Regulation (EU) No 596/2014 of the European Parliament and of the Council of 16 April 2014 on market abuse (market abuse regulation) and repealing Directive 2003/6/EC of the European Parliament and of the Council and Commission Directives 2003/124/EC, 2003/125/EC and 2004/72/EC and Commission Delegated Regulation (EU) 2016/958 of 9 March 2016 supplementing Regulation (EU) No 596/2014 of the European Parliament and of the Council with regard to regulatory technical standards for the technical arrangements for objective presentation of investment recommendations or other information recommending or suggesting an investment strategy and for disclosure of particular interests or indications of conflicts of interest or any other advice, including in the area of investment advisory, within the meaning of the Trading in Financial Instruments Act of 29 July 2005 (i.e. Journal of Laws 2019, item 875, as amended). The marketing communication is prepared with the highest diligence, objectivity, presents the facts known to the author on the date of preparation and is devoid of any evaluation elements. The marketing communication is prepared without considering the client’s needs, his individual financial situation and does not present any investment strategy in any way. The marketing communication does not constitute an offer of sale, offering, subscription, invitation to purchase, advertisement or promotion of any financial instruments. XTB S.A. is not liable for any client’s actions or omissions, in particular for the acquisition or disposal of financial instruments, undertaken on the basis of the information contained in this marketing communication. In the event that the marketing communication contains any information about any results regarding the financial instruments indicated therein, these do not constitute any guarantee or forecast regarding the future results.