Key Takeaways

- Goldman Sachs raised its 12-month USD/JPY forecast from 155 to 165.

- The bank also lifted its 3-month forecast from 160 to 162 and its 6-month target from 158 to 163.

- The yen remains close to its weakest levels in four decades, with USD/JPY currently trading around 162.

- According to Bloomberg's survey, Goldman is now among the most bearish institutions on the Japanese currency.

- Options markets imply roughly a 72% probability that USD/JPY reaches 165 by June next year.

- Hedge funds are holding their largest net short positions in the yen since 2017.

Why Does Goldman Expect Further Yen Weakness?

According to Goldman Sachs FX strategist Karen Reichgott Fishman, three key factors are driving the bank's revised outlook:

- persistently high U.S. Treasury yields,

- mounting fiscal pressures in Japan,

- and the Bank of Japan's very gradual pace of interest rate hikes.

At the same time, Goldman acknowledges that the yen already appears significantly undervalued based on its fundamental valuation models. However, that alone is not enough to trigger a sustained recovery. The bank argues that the wide interest rate differential between the United States and Japan, together with the divergence in monetary policy, continues to strongly favor the U.S. dollar.

Carry Trades Remain a Major Driver

Goldman Sachs continues to favor using the yen as the preferred funding currency for carry trades.

The strategy is straightforward:

- investors borrow low-cost yen,

- sell the currency in the FX market,

- and invest the proceeds in higher-yielding assets such as U.S. bonds or emerging-market currencies.

As long as the Bank of Japan maintains relatively accommodative financial conditions, carry trades are likely to remain attractive, adding further depreciation pressure on the yen.

Can Japan Stop USD/JPY From Rising?

Goldman remains skeptical about the effectiveness of future currency interventions.

Although Japan's Ministry of Finance has hinted that future interventions could become less predictable, the bank believes even direct yen-buying operations would likely generate only a temporary correction.

Unless there is a meaningful decline in U.S. Treasury yields, a more hawkish Bank of Japan, or a significant narrowing of the U.S.-Japan interest rate gap, the fundamental drivers of yen weakness are likely to remain firmly in place.

Markets Are Increasingly Pricing in USD/JPY at 165

One notable aspect of Goldman's outlook is how closely it aligns with broader market positioning.

Currently:

- hedge funds hold their largest net short yen positions in eight years,

- FX derivatives imply roughly a 72% probability of USD/JPY reaching 165 by the middle of next year,

- and an increasing number of investors view shorting the yen as one of the most crowded trades in global currency markets.

While this reinforces the prevailing uptrend, it also increases the risk of sharp corrections should expectations for the Federal Reserve or the Bank of Japan change unexpectedly.

What Could Change the Outlook?

The key near-term event will be the release of this week's Federal Reserve meeting minutes.

Investors will focus primarily on:

- signals regarding future Fed rate cuts,

- the direction of U.S. Treasury yields,

- upcoming Bank of Japan policy decisions,

- and the possibility of intervention by Japanese authorities.

A hawkish set of Fed minutes could strengthen the U.S. dollar further, putting renewed pressure on both the yen and the euro. Conversely, weaker U.S. economic data could lower Treasury yields and provide temporary relief for non-dollar currencies.

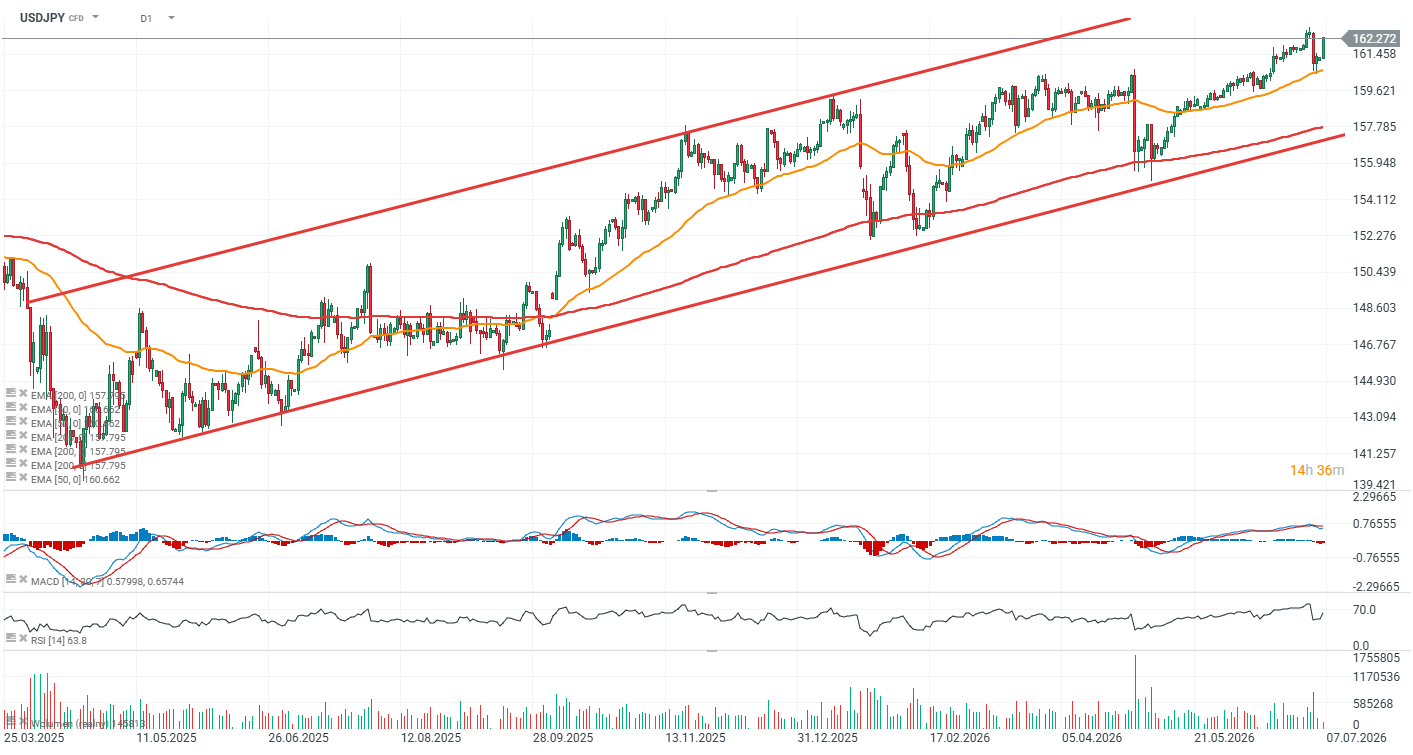

USD/JPY Technical Analysis (D1)

USD/JPY remains in a strong uptrend and continues to trade within a well-defined ascending price channel. The lower boundary of the channel is currently located near 158, a level that was last tested in May. In the short term, resistance is seen around 162.8, corresponding to the pair's recent swing highs. A sustained break above this level could reinforce bullish momentum, while a rejection may trigger another pullback toward the lower boundary of the ascending channel. 165 level i now probably the strongest resistance zone.

Source: xStation5

Daily Summary: Chip War Weighs on Wall Street as Oil Plunges After US–Iran Ceasefire ⭐

Nasdaq-100 under pressure after chip sell-off

China Is Building Its Own Chip-Making Machines. ASML Under Pressure as the Technology War Enters a New Phase

US Open: Wall Street Rebounds After US Iran Ceasefire

The content of this report has been created by XTB S.A., with its registered office in Warsaw, at Prosta 67, 00-838 Warsaw, Poland, (KRS number 0000217580) and supervised by Polish Supervision Authority ( No. DDM-M-4021-57-1/2005). This material is a marketing communication within the meaning of Art. 24 (3) of Directive 2014/65/EU of the European Parliament and of the Council of 15 May 2014 on markets in financial instruments and amending Directive 2002/92/EC and Directive 2011/61/EU (MiFID II). Marketing communication is not an investment recommendation or information recommending or suggesting an investment strategy within the meaning of Regulation (EU) No 596/2014 of the European Parliament and of the Council of 16 April 2014 on market abuse (market abuse regulation) and repealing Directive 2003/6/EC of the European Parliament and of the Council and Commission Directives 2003/124/EC, 2003/125/EC and 2004/72/EC and Commission Delegated Regulation (EU) 2016/958 of 9 March 2016 supplementing Regulation (EU) No 596/2014 of the European Parliament and of the Council with regard to regulatory technical standards for the technical arrangements for objective presentation of investment recommendations or other information recommending or suggesting an investment strategy and for disclosure of particular interests or indications of conflicts of interest or any other advice, including in the area of investment advisory, within the meaning of the Trading in Financial Instruments Act of 29 July 2005 (i.e. Journal of Laws 2019, item 875, as amended). The marketing communication is prepared with the highest diligence, objectivity, presents the facts known to the author on the date of preparation and is devoid of any evaluation elements. The marketing communication is prepared without considering the client’s needs, his individual financial situation and does not present any investment strategy in any way. The marketing communication does not constitute an offer of sale, offering, subscription, invitation to purchase, advertisement or promotion of any financial instruments. XTB S.A. is not liable for any client’s actions or omissions, in particular for the acquisition or disposal of financial instruments, undertaken on the basis of the information contained in this marketing communication. In the event that the marketing communication contains any information about any results regarding the financial instruments indicated therein, these do not constitute any guarantee or forecast regarding the future results.