In market terms, airlines are among the most obvious losers of the war in Iran. This conflict has not only shut down an extremely important air corridor through the Middle East, but has also triggered an explosion in jet fuel prices.

Jet fuel is a far more scarce energy carrier than other petroleum products. This is clearly visible in airlines’ financial statements, fuel accounts for roughly 30% of their operating costs on average.

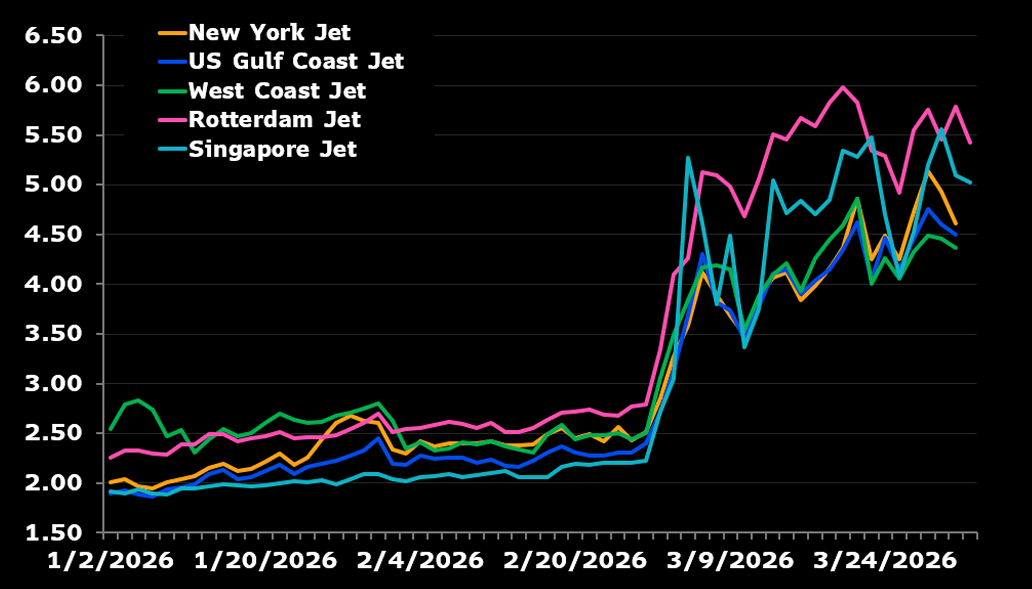

Source: Bloomberg Finance

Given that the Middle East had accounted for a disproportionately large share of global jet fuel supply, the blockade of the strait and attacks on infrastructure pushed jet fuel prices up by 100% to as much as 200%, depending on the region. The natural consequence would be strong cost pressure on airlines—i.e., a cost increase of around 30–60%.

But is that really the case?

Airlines do not rely solely on the whims of the market and producers when planning budgets. They use financial instruments that allow them to eliminate 70–80% of fuel price volatility. This means that an increase of several dozen percent, in real terms, may shrink to just a few percent.

This is positive from the perspective of potential airline results; however, such a strategy makes price and demand less tightly linked, and in the context of persistently reduced supply, this can imply a physical shortage.

Analysts at Cirium and Bloomberg indicate that, for now, major airline operators in Europe are not showing signs of a supply/fuel shock.

It is not possible, however, to determine to what extent these entities are anticipating political decisions and market reactions, and to what extent this is simply “putting on a brave face.”

What cannot be hedged against, though, is physical congestion in air corridors. The wars in Ukraine and Iran leave a very narrow belt over the Caucasus through which aircraft can travel from East Asia to Europe and vice versa. Here too, the market may still be caught off guard. An escalation of the conflict in the Middle East does not have to eliminate demand for travel, but it may shift it elsewhere—something that will be reflected in travel volumes.

The analyst consensus on companies’ results is deeply negative. For example, following Lufthansa’s Q1 results, a net loss and a nearly 10% decline in revenue are expected. A more plausible scenario is that airlines, especially those in Europe, may defy the market’s grim expectations and positively surprise with results for a difficult quarter. If, however, results for some reason turn out worse than pessimistic expectations, it could trigger a genuine flight of capital from the sector.

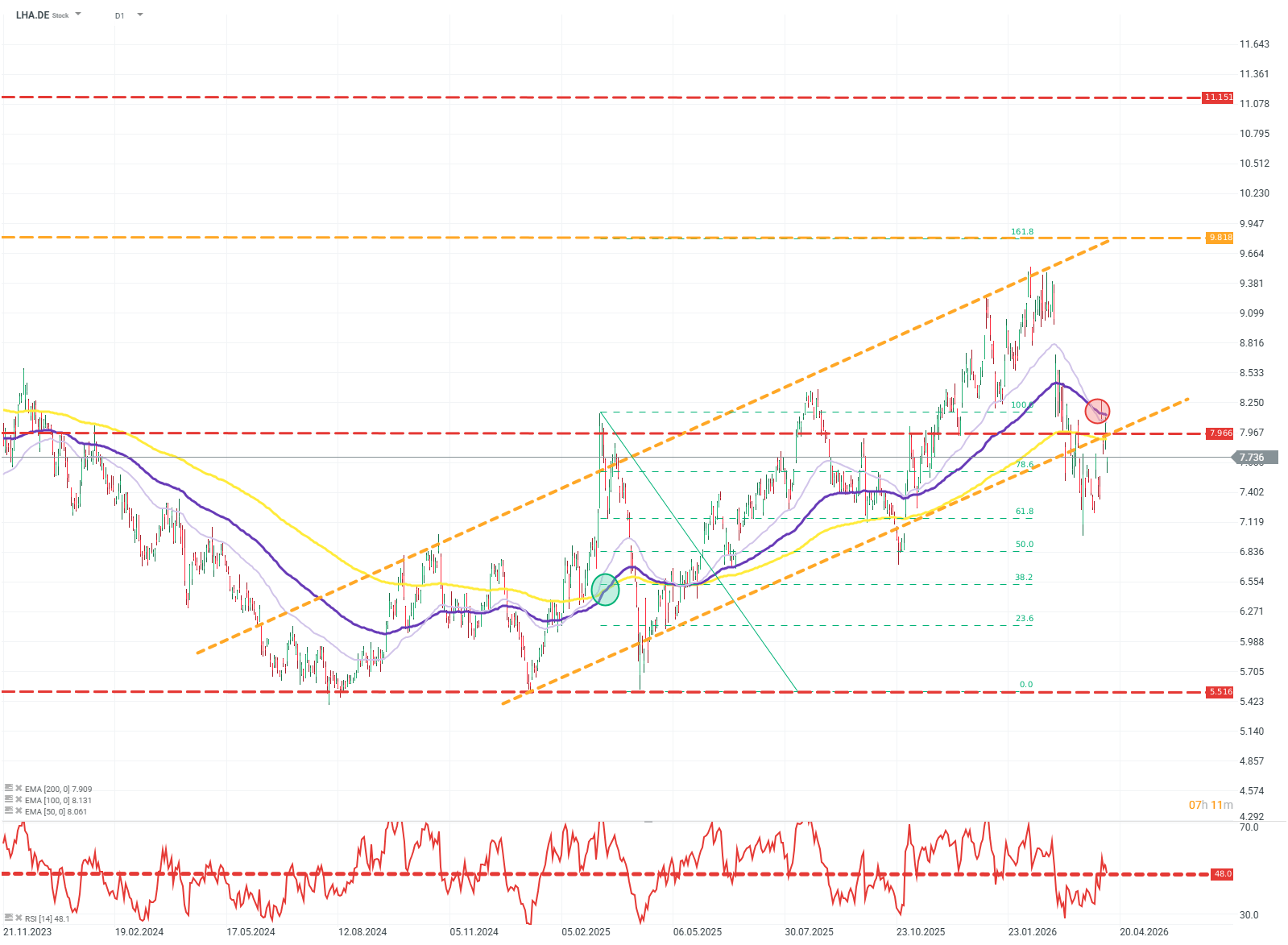

LHA.DE (D1)

The share price continues to maintain a shallow uptrend. The momentum of EMA100 and EMA200 remains bullish, but the crossover of EMA50 and EMA100 points to clear short-term pressure. Defending the trendline will be crucial to sustaining the uptrend and potentially recouping losses. If sellers take control, the target level for further correction is around €7.1. Source: xStation5

Daily Summary: Markets limit the pullback while awaiting the Fed

France Challenges Palantir, Market Reacts.

The semiconductors sell-off continues 📉

US OPEN: Deeper sell-off and a SaaS rebound

The content of this report has been created by XTB S.A., with its registered office in Warsaw, at Prosta 67, 00-838 Warsaw, Poland, (KRS number 0000217580) and supervised by Polish Supervision Authority ( No. DDM-M-4021-57-1/2005). This material is a marketing communication within the meaning of Art. 24 (3) of Directive 2014/65/EU of the European Parliament and of the Council of 15 May 2014 on markets in financial instruments and amending Directive 2002/92/EC and Directive 2011/61/EU (MiFID II). Marketing communication is not an investment recommendation or information recommending or suggesting an investment strategy within the meaning of Regulation (EU) No 596/2014 of the European Parliament and of the Council of 16 April 2014 on market abuse (market abuse regulation) and repealing Directive 2003/6/EC of the European Parliament and of the Council and Commission Directives 2003/124/EC, 2003/125/EC and 2004/72/EC and Commission Delegated Regulation (EU) 2016/958 of 9 March 2016 supplementing Regulation (EU) No 596/2014 of the European Parliament and of the Council with regard to regulatory technical standards for the technical arrangements for objective presentation of investment recommendations or other information recommending or suggesting an investment strategy and for disclosure of particular interests or indications of conflicts of interest or any other advice, including in the area of investment advisory, within the meaning of the Trading in Financial Instruments Act of 29 July 2005 (i.e. Journal of Laws 2019, item 875, as amended). The marketing communication is prepared with the highest diligence, objectivity, presents the facts known to the author on the date of preparation and is devoid of any evaluation elements. The marketing communication is prepared without considering the client’s needs, his individual financial situation and does not present any investment strategy in any way. The marketing communication does not constitute an offer of sale, offering, subscription, invitation to purchase, advertisement or promotion of any financial instruments. XTB S.A. is not liable for any client’s actions or omissions, in particular for the acquisition or disposal of financial instruments, undertaken on the basis of the information contained in this marketing communication. In the event that the marketing communication contains any information about any results regarding the financial instruments indicated therein, these do not constitute any guarantee or forecast regarding the future results.