- What’s behind the strong earnings?

- Does investment banking indicate the direction of the markets?

- What are the dangers of excessive capital concentration?

- What’s behind the strong earnings?

- Does investment banking indicate the direction of the markets?

- What are the dangers of excessive capital concentration?

BlackRock, a well-known and sometimes controversial giant in the investment and asset-management industry, has published its results. Beating already optimistic investor expectations has pushed the company’s valuation close to all-time highs.

BlackRock’s 2025 earnings, however, are more than just a successful year-end for the world’s largest asset manager. They provide a reference point for understanding how the centre of gravity in financial markets and the economy is shifting: where growth is concentrating, what is driving strong performance, and why an increasing part of the economy is starting to operate according to the logic of wealthy clients rather than the mass market.

BlackRock ended the year with assets under management exceeding $14 trillion. EPS for Q4 2025 exceeded investor expectations by 5%, coming in at $13.16, while revenue reached a round $7 billion versus expectations of $6.75 billion.

What might superficially be a cause for concern is a year-on-year, decline in net revenue of more than 30%. This is, however, a signal of growth rather than deteriorating operational metrics. The company is benefiting from the ongoing M&A boom and has itself acquired a number of platforms and investment firms, which improves its growth outlook but puts short-term pressure on profitability.

BLK.US (D1)

Source: xStation5

What matters most, however, is not the numbers themselves but their composition. Record fund inflows, rapid growth in the wealth-management market, and the expansion of offerings aimed at affluent individual clients show that a business model based on scale, data, and access to capital is gaining an advantage that is effectively impossible to compete with.

Particularly noteworthy is the shift in growth toward higher-margin products. Private credit funds, trading infrastructure, and active strategies sold in fund form allow BlackRock to partly escape the long-standing pressure to cut fees in passive management.

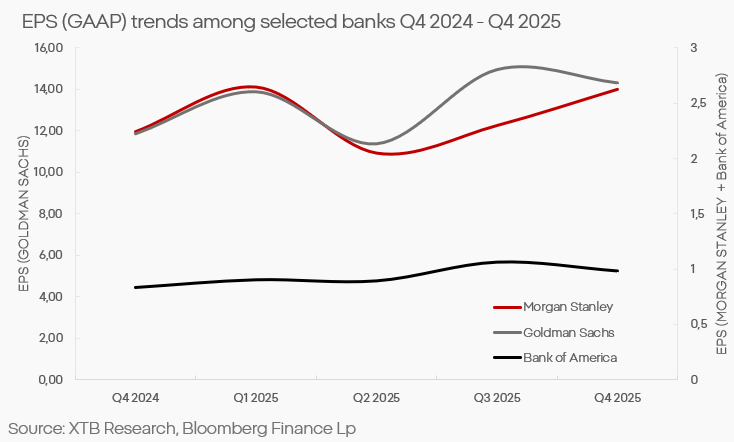

Investment banking beats commercial banking

Where can we see the systemic turn in the economy and markets mentioned above? Both Goldman Sachs and Morgan Stanley have shown relative resilience in recent quarters, and in some areas, a clear rebound. Investment banking, asset management, and services for affluent private clients have performed better than traditional deposit-and-loan banking.

The contrast with commercial banks is striking. Margins that not long ago benefited from high interest rates are starting to shrink. At the same time, credit risk is rising markedly among customers with lower financial capacity. These factors mean that banks built around the mass-market customer are lagging behind.

Investment banks operate in a different world. Their revenues depend more on market activity, advisory services, securities issuance, and wealth management. Wealthy clients and institutions benefit from the “wealth effect”: asset valuations inflate, corporate margins rise, and lower interest rates enable ever larger and increasingly risky investments.

Top 6 (Market cap) Capital Markets Companies, average return ~34% Source: xStation5

Top 6 (Market cap) Consumer Finance Companies, average return ~28% Source: xStation5

The sector divergence in results is a consequence of an increasingly extreme shift and concentration of resources in the economy. A growing share of financial assets is held by a narrow group of entities and households. This group is now generating not only the vast majority of investment demand but increasingly consumer demand as well—something also visible in the results of companies outside the financial sector.

The race for affluent customers

A textbook example is airlines. For years, they competed on price and volume; now they are increasingly shifting their business model toward maximizing revenue per passenger. Premium segments, loyalty programs, and the sale of ancillary services now determine the profitability of entire fleets.

Not all sectors, however, can adapt to this logic. Commercial real estate depends on real economic activity and demand from businesses. Office-building owners are stuck in a macroeconomic trap of remote work, unprecedented employment cuts, and offshoring. The commercial real-estate sector remains a millstone for many smaller banks, which will only deepen the gap between players in the industry.

Low-margin retail also has little room to “select” customers or raise prices without losing volume. Despite the inflation surge—which the sector used to increase not only profits but also margins—those margins proved temporary. Today many companies in this sector are finding it increasingly difficult to deliver results.

It is precisely in these sectors that the dissonance between good macroeconomic data and weaker conditions in the real economy shows up fastest. Financial indices rise while a large part of business operates under stagnation or recession conditions.

Capital concentration and systemic risk

Structural capital accumulation leads to concentration that increasingly distorts macroeconomic data. Growth in financial assets and in the profits of institutions serving wealthy clients does not have to translate into broad-based economic growth; more often than not, it produces the opposite tendency. At the same time, concentrating investment decisions in the hands of a few global players raises systemic risks to unacceptable levels. This is especially important given the growing role of “private” markets, which control an ever larger share of global assets, have a much more aggressive risk profile, and at the same time lack regulatory oversight.

A two-speed market

The results of BlackRock and the investment banks are now a barometer of the financial system’s condition and show the direction in which the market and the economy are heading. The affluent part of society and institutional investors have concentrated capital to a degree that motivates them to seek increasingly exotic assets, increases risk tolerance, and distorts the perception of risk.

Companies unwilling or unable to pivot toward high-margin services for affluent customers suffer from declining demand and investment, creating a self-reinforcing spiral. At the same time, distorted data on consumption and demand in the economy feed models lacking nuance and cause monetary policymakers to operate with an ever greater disconnect from real economic conditions—amplifying risk.

Daily Summary: Wall Street Regains Ground; Another Intervention in the Yen Market❓

Three Markets to Watch Next Week (July 31, 2026)

Market Wrap: European equities at 3-week highs! Apple dips in US premarket!

Euro Area core inflation above estiamtes! EURUSD under key resistance!

The content of this report has been created by XTB S.A., with its registered office in Warsaw, at Prosta 67, 00-838 Warsaw, Poland, (KRS number 0000217580) and supervised by Polish Supervision Authority ( No. DDM-M-4021-57-1/2005). This material is a marketing communication within the meaning of Art. 24 (3) of Directive 2014/65/EU of the European Parliament and of the Council of 15 May 2014 on markets in financial instruments and amending Directive 2002/92/EC and Directive 2011/61/EU (MiFID II). Marketing communication is not an investment recommendation or information recommending or suggesting an investment strategy within the meaning of Regulation (EU) No 596/2014 of the European Parliament and of the Council of 16 April 2014 on market abuse (market abuse regulation) and repealing Directive 2003/6/EC of the European Parliament and of the Council and Commission Directives 2003/124/EC, 2003/125/EC and 2004/72/EC and Commission Delegated Regulation (EU) 2016/958 of 9 March 2016 supplementing Regulation (EU) No 596/2014 of the European Parliament and of the Council with regard to regulatory technical standards for the technical arrangements for objective presentation of investment recommendations or other information recommending or suggesting an investment strategy and for disclosure of particular interests or indications of conflicts of interest or any other advice, including in the area of investment advisory, within the meaning of the Trading in Financial Instruments Act of 29 July 2005 (i.e. Journal of Laws 2019, item 875, as amended). The marketing communication is prepared with the highest diligence, objectivity, presents the facts known to the author on the date of preparation and is devoid of any evaluation elements. The marketing communication is prepared without considering the client’s needs, his individual financial situation and does not present any investment strategy in any way. The marketing communication does not constitute an offer of sale, offering, subscription, invitation to purchase, advertisement or promotion of any financial instruments. XTB S.A. is not liable for any client’s actions or omissions, in particular for the acquisition or disposal of financial instruments, undertaken on the basis of the information contained in this marketing communication. In the event that the marketing communication contains any information about any results regarding the financial instruments indicated therein, these do not constitute any guarantee or forecast regarding the future results.