Market Overview:

-

European stock indices, including the pan-European STOXX 600, are mostly down, whilst the main US index futures are also falling due to renewed concerns about rising inflation.

-

However, the German DE40 contract has managed to buck this market weakness and is up by around 0.36%.

-

The main factor driving current sentiment remains the war between the US and Iran, which has been ongoing for over two months and has led to the blockage of the Strait of Hormuz, a key shipping route.

-

This conflict is fuelling market fears of a sharp rise in energy prices, which in turn is forcing major central banks to maintain a hawkish stance and keep interest rates higher.

-

As a result of these geopolitical tensions, oil prices continue to rise, with Brent crude surpassing the $110 mark, gaining over 0.5%.

-

The US dollar, meanwhile, is trading slightly lower today (the USDIDX index is down 0.14%), which opens the way for a slight rise in the EUR/USD exchange rate.

-

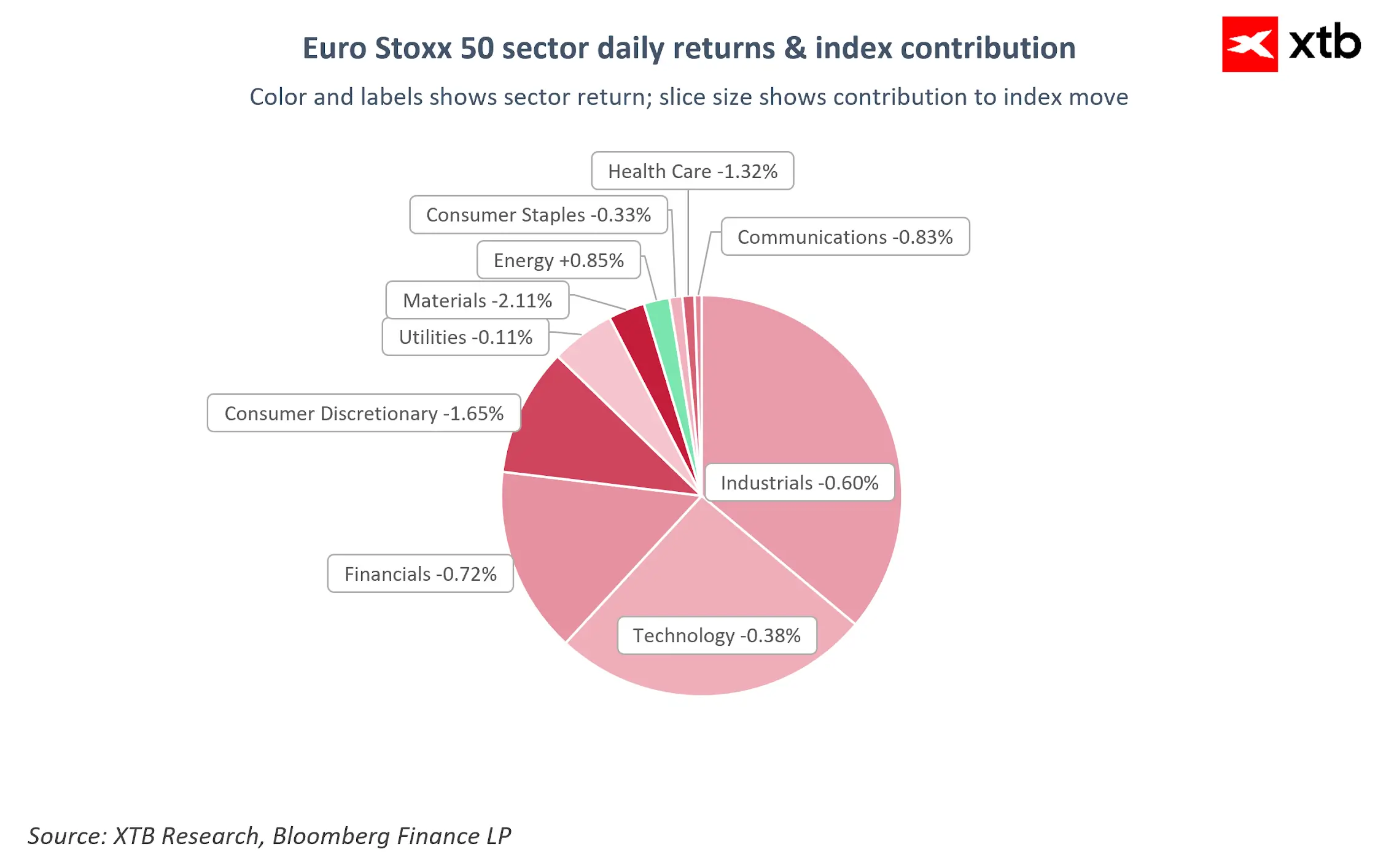

Turning back to the stock markets, the energy sector is by far the best performer in the current climate; it is the only sector in the eurozone currently showing solid growth momentum, driven by rising commodity prices.

-

By far the worst-performing sectors, however, are materials, consumer discretionary and healthcare, which are most heavily weighed down by concerns over a slowdown in demand and high financing costs.

Index and sector chart – What drives the market?

The sectoral breakdown of the Euro Stoxx 50 index highlights the broad scope of today’s sell-off, from which only the energy sector—up by a fraction of a per cent—managed to emerge unscathed. Source: XTB

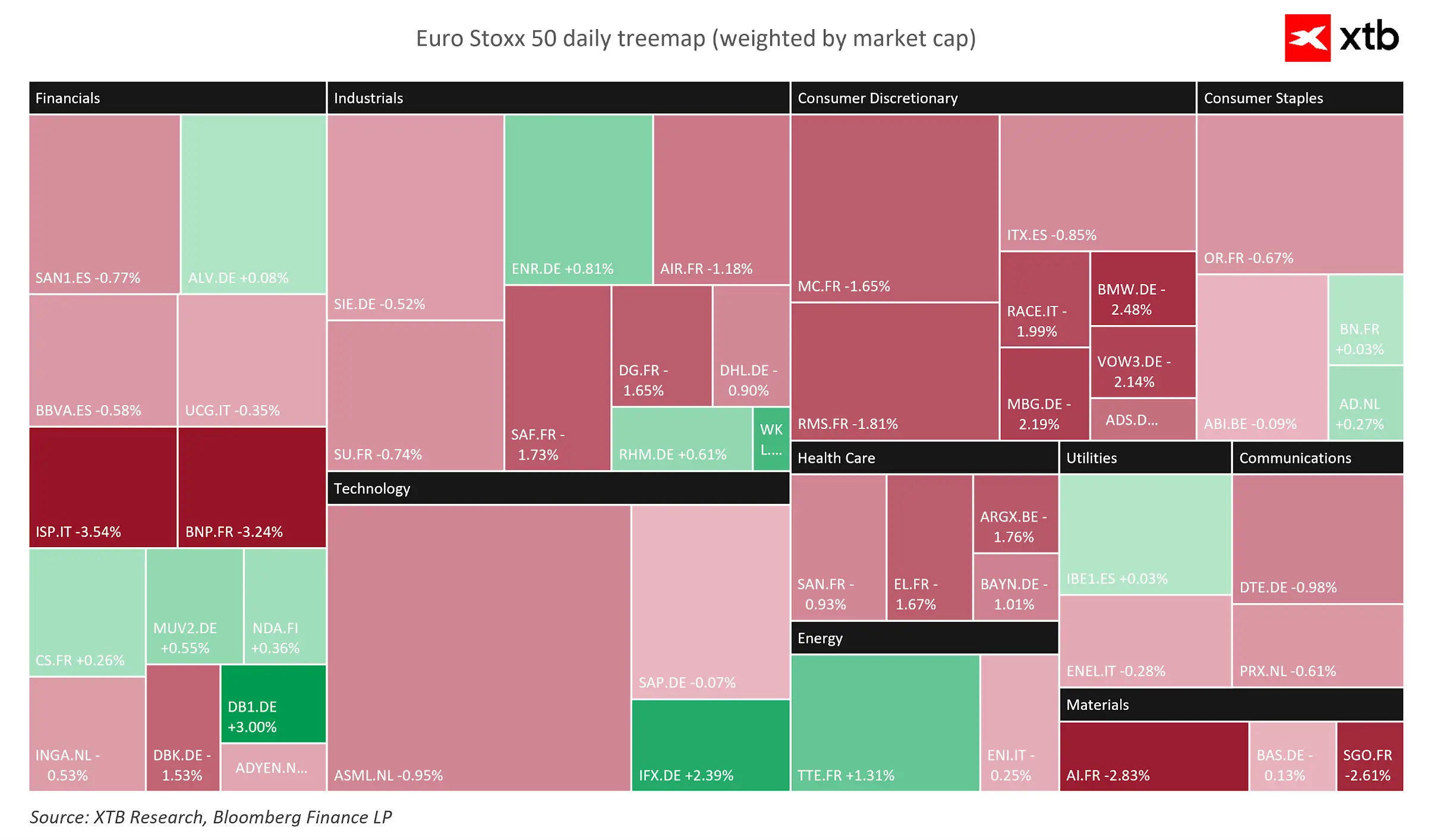

The sentiment map for major European blue chips shows a clear advantage for sellers, who have dominated key market sectors today, including finance and industry, leaving room for only a few isolated pockets of green. Source: XTB

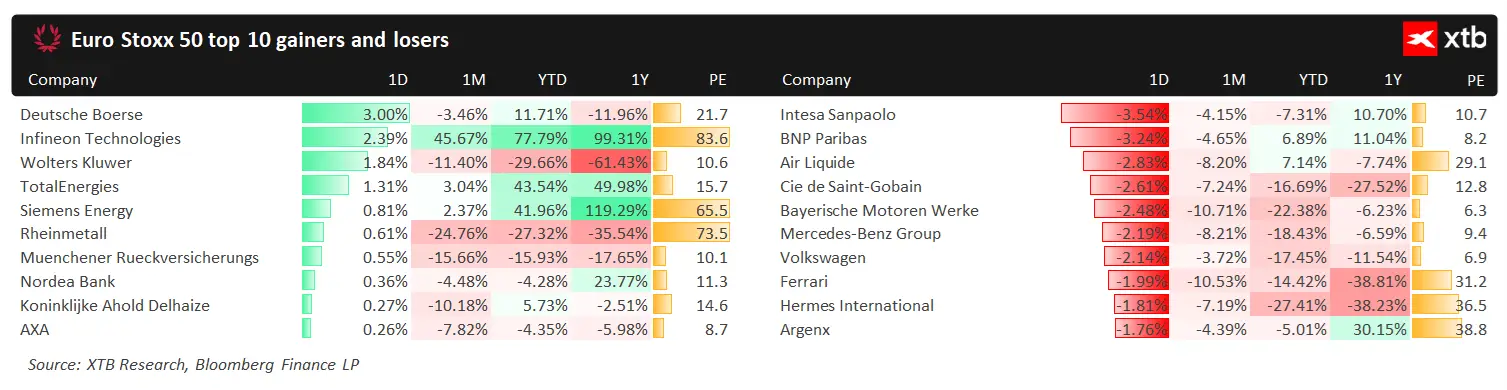

A look at the session’s top performers and laggards confirms that, whilst Intesa Sanpaolo and BNP Paribas are leading the declines with losses of over 3 per cent, at the other end of the spectrum, Deutsche Boerse and Infineon Technologies are proving most resilient against selling pressure. Source: XTB

Company information:

-

Investors’ attention is largely focused today on Samsung Electronics (SMSN.UK), whose shares are rebounding strongly, thereby preventing the Korean index from entering deep correction territory. This rally in the tech giant’s shares is the result of the resumption of negotiations with the main trade union; investors have welcomed with relief the willingness to compromise and the court’s decision limiting the possibility of a strike, which reduces the risk of a disruption to global memory chip supplies.

-

Ryanair is standing out for all the wrong reasons on the European market, with its shares falling by over 4% following warnings of higher operating and fuel costs, as well as worse-than-expected forecasts for ticket prices during the summer holiday season.

-

At the other end of the spectrum is Deutsche Boerse (DB1.DE), up 3% following the market’s positive reaction to the news that the well-known fund TCI has acquired a stake of over 5% in the German stock exchange operator.

-

French advertising giant Publicis (PUB.FR) also had a successful day, gaining around 2.7% following the announcement of a $2.2 billion takeover of the US data analytics firm LiveRamp.

Cocoa loses 4% amid news from Ghana 🚩 What's next for the market?

Oil Pulls Back After Strong Gains 🚩 Markets Assess the Strait of Hormuz Impasse

Intel Raises the Stakes: $20 Billion for a Major Comeback

Market Wrap: Energy Leads Gains in Europe, ASML Rebounds 🔼 Alcon Rises 4% After Earnings

The content of this report has been created by XTB S.A., with its registered office in Warsaw, at Prosta 67, 00-838 Warsaw, Poland, (KRS number 0000217580) and supervised by Polish Supervision Authority ( No. DDM-M-4021-57-1/2005). This material is a marketing communication within the meaning of Art. 24 (3) of Directive 2014/65/EU of the European Parliament and of the Council of 15 May 2014 on markets in financial instruments and amending Directive 2002/92/EC and Directive 2011/61/EU (MiFID II). Marketing communication is not an investment recommendation or information recommending or suggesting an investment strategy within the meaning of Regulation (EU) No 596/2014 of the European Parliament and of the Council of 16 April 2014 on market abuse (market abuse regulation) and repealing Directive 2003/6/EC of the European Parliament and of the Council and Commission Directives 2003/124/EC, 2003/125/EC and 2004/72/EC and Commission Delegated Regulation (EU) 2016/958 of 9 March 2016 supplementing Regulation (EU) No 596/2014 of the European Parliament and of the Council with regard to regulatory technical standards for the technical arrangements for objective presentation of investment recommendations or other information recommending or suggesting an investment strategy and for disclosure of particular interests or indications of conflicts of interest or any other advice, including in the area of investment advisory, within the meaning of the Trading in Financial Instruments Act of 29 July 2005 (i.e. Journal of Laws 2019, item 875, as amended). The marketing communication is prepared with the highest diligence, objectivity, presents the facts known to the author on the date of preparation and is devoid of any evaluation elements. The marketing communication is prepared without considering the client’s needs, his individual financial situation and does not present any investment strategy in any way. The marketing communication does not constitute an offer of sale, offering, subscription, invitation to purchase, advertisement or promotion of any financial instruments. XTB S.A. is not liable for any client’s actions or omissions, in particular for the acquisition or disposal of financial instruments, undertaken on the basis of the information contained in this marketing communication. In the event that the marketing communication contains any information about any results regarding the financial instruments indicated therein, these do not constitute any guarantee or forecast regarding the future results.