By Friday afternoon, market sentiment is dominated by fears of further military escalation in Iran. The concentration of U.S. forces in the Persian Gulf is expected to increase, and markets are increasingly concerned that any potential offensive by the U.S. and Israel could also involve Saudi Arabia. Such a scenario would represent an extreme escalation, potentially leading to reciprocal strikes on critical infrastructure across the region—from power plants to desalination facilities. Markets have largely ignored yesterday’s statement from Donald Trump, who announced overnight that the period of non-aggression toward Iran’s energy infrastructure had been extended by another 10 days, until April 4.

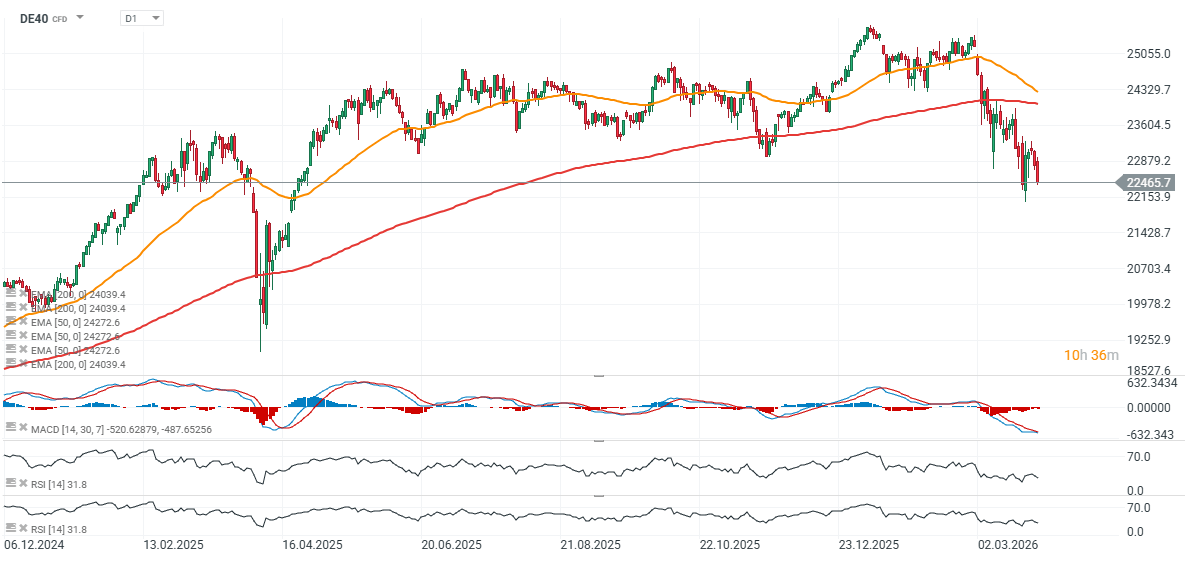

European equities are under pressure, with broad-based declines across major indices. The Euro Stoxx 50 is down more than 1.3%, while Germany’s DAX is falling over 1.5%. ECB President Christine Lagarde warned yesterday that markets may be underestimating the scale of the energy shock gradually feeding into the global economy. She highlighted that Europe could be particularly exposed through energy markets, supply chains, and critical inputs such as helium, which is essential for semiconductor production. Lagarde also noted that the shock could persist for years, with the economic adjustment unfolding gradually. European heavy industry, as well as sectors such as chemicals and logistics, appear especially vulnerable to a potential downturn driven by elevated oil and gas prices.

- The cyclical media sector is among the worst performers today, with European companies in the segment down around 3% on average. CTS Eventim is in focus, with shares plunging 16% following a disappointing full-year outlook.

- Markets remain highly sensitive to headlines regarding further military escalation, including the possibility of increased U.S. ground troop involvement in the region. Ahead of the weekend, investors are clearly reducing risk exposure.

- The Strait of Hormuz remains a key focal point for global markets. In the view of market participants, only tangible progress toward reopening the strait would provide a more durable improvement in sentiment.

- The economic impact of the conflict is increasingly visible in macro data, with recent readings pointing to a sharp slowdown in private sector activity in March. This reinforces concerns about a mix of weaker growth and rising inflationary pressures.

- Interest rate markets have also repriced expectations for the ECB. The probability of a rate hike in April has risen to around 71%, compared to expectations of no hikes for most of the year prior to the outbreak of the conflict.

- Rising bond yields are adding further pressure to equities, with the German 10-year Bund yield climbing to its highest level since 2011, reducing the relative attractiveness of stocks and increasing the cost of capital.

- Against the broader market weakness, Pernod Ricard stands out, gaining around 3% after confirming discussions regarding a potential merger with Brown-Forman, the owner of Jack Daniel’s.

- AstraZeneca is also outperforming, with shares up 3.4% after its experimental respiratory treatment Tozorakimab met primary endpoints in two late-stage trials, supporting the broader healthcare sector.

- Overall, the session reflects a consistent pattern: investors are reducing risk, bond yields are rising, and the main transmission channels of geopolitical tensions into markets remain energy prices, inflation expectations, and central bank policy.

- Earlier this week, the STOXX 600 briefly approached correction territory, falling around 10% from its February peak. However, subsequent comments from Donald Trump regarding a potential extension of the deadline for reopening the Strait of Hormuz helped to partially stabilize market sentiment.

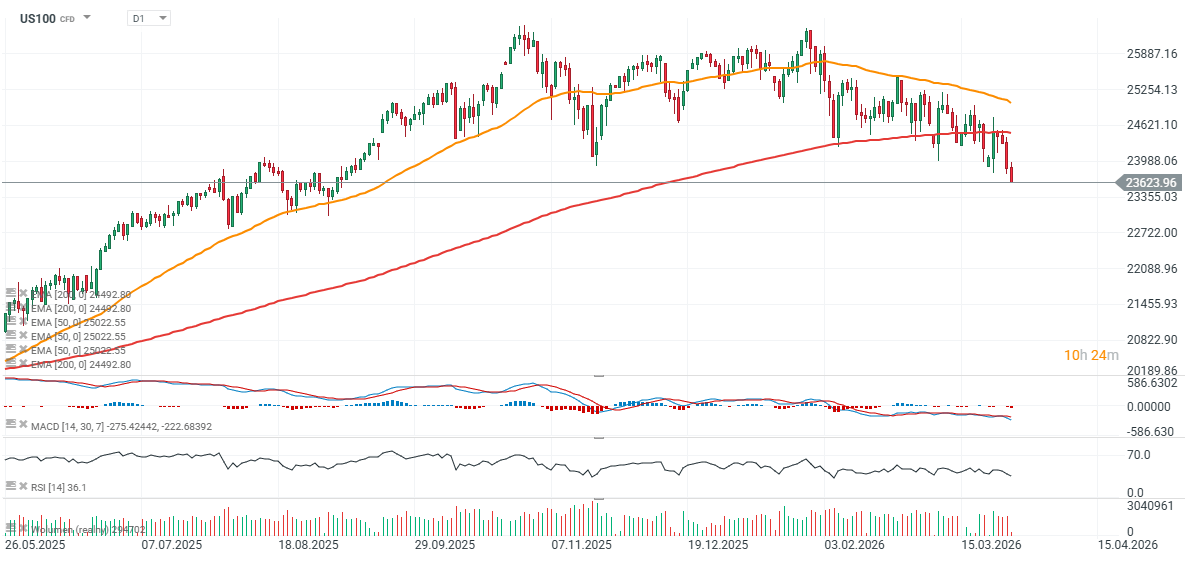

Charts: DE40 and US100 (D1 interval)

Source: xStation5

Source: xStation5

Daily summary: Dollar rout after NFP, Gold back on the rise

Three markets to watch next week (07.08.2026)

Who Will Surprise With Earnings Next Week? (07.08.2026)

US OPEN: Shallow rebound in the shadow of a weak labor market

The content of this report has been created by XTB S.A., with its registered office in Warsaw, at Prosta 67, 00-838 Warsaw, Poland, (KRS number 0000217580) and supervised by Polish Supervision Authority ( No. DDM-M-4021-57-1/2005). This material is a marketing communication within the meaning of Art. 24 (3) of Directive 2014/65/EU of the European Parliament and of the Council of 15 May 2014 on markets in financial instruments and amending Directive 2002/92/EC and Directive 2011/61/EU (MiFID II). Marketing communication is not an investment recommendation or information recommending or suggesting an investment strategy within the meaning of Regulation (EU) No 596/2014 of the European Parliament and of the Council of 16 April 2014 on market abuse (market abuse regulation) and repealing Directive 2003/6/EC of the European Parliament and of the Council and Commission Directives 2003/124/EC, 2003/125/EC and 2004/72/EC and Commission Delegated Regulation (EU) 2016/958 of 9 March 2016 supplementing Regulation (EU) No 596/2014 of the European Parliament and of the Council with regard to regulatory technical standards for the technical arrangements for objective presentation of investment recommendations or other information recommending or suggesting an investment strategy and for disclosure of particular interests or indications of conflicts of interest or any other advice, including in the area of investment advisory, within the meaning of the Trading in Financial Instruments Act of 29 July 2005 (i.e. Journal of Laws 2019, item 875, as amended). The marketing communication is prepared with the highest diligence, objectivity, presents the facts known to the author on the date of preparation and is devoid of any evaluation elements. The marketing communication is prepared without considering the client’s needs, his individual financial situation and does not present any investment strategy in any way. The marketing communication does not constitute an offer of sale, offering, subscription, invitation to purchase, advertisement or promotion of any financial instruments. XTB S.A. is not liable for any client’s actions or omissions, in particular for the acquisition or disposal of financial instruments, undertaken on the basis of the information contained in this marketing communication. In the event that the marketing communication contains any information about any results regarding the financial instruments indicated therein, these do not constitute any guarantee or forecast regarding the future results.