🌍 Geopolitical Situation & Diplomacy

-

The United States has conducted another round of airstrikes on Iran, and Tehran has responded with missile and drone attacks on targets in the region, leading to a further escalation of the conflict.

-

The Iranian Ministry of Foreign Affairs reports that talks with the US regarding the memorandum of understanding are in a "crisis phase", and Tehran announces that it will not fulfill its obligations until the other side complies with its agreements.

-

Iran also reports that attempts to establish a joint mechanism regarding the Strait of Hormuz involving Oman are being hindered by US pressure on that country, which further complicates the diplomatic situation.

-

Tensions are causing an increase in oil prices, pressure on financial markets, and the risk of further economic deterioration if the conflict continues to expand.

-

The international community is appealing for a return to negotiations; however, military actions between the US and Iran currently continue to intensify.

-

The Iranian news agency Mehr News Agency reports that explosions were heard in the vicinity of the Iranian port of Bandar Abbas and Qeshm island.

🛢️ Commodities & Energy

-

Crude oil is gaining approximately 2.5% at this moment, reacting to rising geopolitical risks and potential constraints in commodity supply.

-

The growing risk of disruptions to oil flows through the Strait of Hormuz increases investor concerns over global energy supplies, supporting the rise in commodity prices and stoking inflation fears.

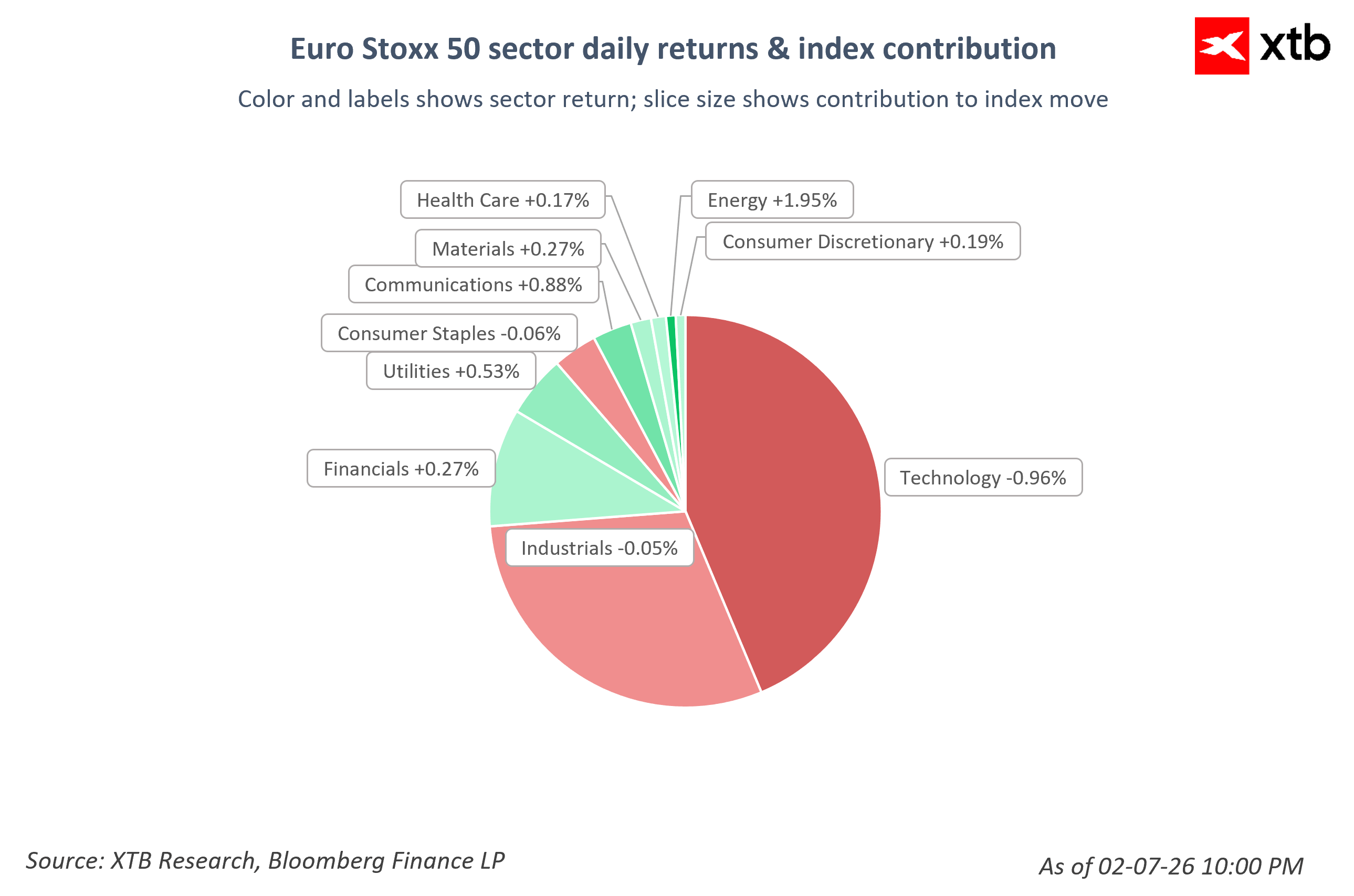

📈 Stock Market

-

The deterioration in market sentiment translates into pressure on risky assets, including semiconductor equities, despite sustained strong interest in the artificial intelligence sector.

-

Investors remain focused on the further development of the Middle East conflict and the upcoming quarterly earnings of mega-cap tech companies, which will reveal the health of the AI sector and its growth prospects.

-

The session on European trading floors is progressing mostly in slight positive territory, demonstrating the relative resilience of investors despite ongoing geopolitical tensions and rising energy market concerns.

-

The strongest performance is seen in indices from Germany and Spain, where the DAX is gaining around 0.1% and the IBEX 35 is rising by about 0.2%, supported by positive sentiment surrounding certain industrial and financial companies.

-

France's CAC 40, similarly to the broad European Euro Stoxx 50, remains symbolically in the green.

-

The British FTSE 100 is holding close to its opening level with a minor loss.

-

Investors in Europe remain cautious, analyzing the impact of Middle East tensions, the situation around the Strait of Hormuz, and a potential rise in oil prices on the economic outlook and central bank policies.

-

Despite the uncertainty, equity markets remain stable, and investor attention outside of geopolitics is drawn to upcoming corporate quarterly results and the further growth prospects of the technology sector.

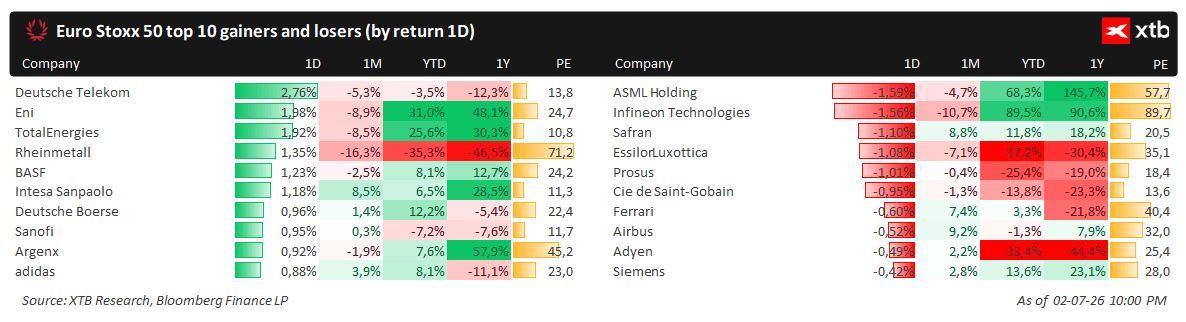

🏭 Sectors & Companies

-

Volkswagen is considering the reduction of another 50,000 jobs, as the current austerity program may not be sufficient to improve the company's competitiveness.

-

The German manufacturer is struggling with high production costs, pressure from Chinese automotive brands, and slower demand for electric vehicles in Europe.

-

Additional cutbacks would complement already planned layoffs, which could mean up to approximately 100,000 job reductions across the entire group.

-

The restructuring is intended to help Volkswagen lower costs, but it may spark strong opposition from trade unions and employees.

-

European airlines are under pressure following the rise in oil prices triggered by escalating Middle East tensions.

-

Higher fuel costs could compress the margins of carriers, who are already facing cost pressures and uncertainty regarding travel demand.

-

Shares of companies such as Lufthansa, Ryanair, and TUI are falling, as investors fear a further increase in operating expenses.

-

European oil companies are gaining on stock exchanges following the escalation of the US-Iran conflict, which is driving up oil prices.

-

Investors fear disruptions to commodity supplies from the Middle East, which increases the valuation of energy giants such as BP, Shell, and TotalEnergies.

-

Higher oil prices improve the revenue outlook for fuel producers, but simultaneously increase inflation risks and pressure on other economic sectors.

🪙 Precious Metals

-

The precious metals market is experiencing declines, the foundation of which lies in the escalation of the conflict in the Middle East.

-

Gold is retracing by about 0.1% and falling below $4,100 per ounce.

-

Silver is dropping by over 2% and pulling back below $59 per ounce.

💻 Cryptocurrencies

-

Cryptocurrencies also remain under pressure.

-

Bitcoin is falling by over 1.3% and testing the $63,000 level.

-

Ethereum is losing around 0.1% and sliding below $1,800.

Daily Summary: Wall Street Regains Ground; Another Intervention in the Yen Market❓

Three Markets to Watch Next Week (July 31, 2026)

Market Wrap: European equities at 3-week highs! Apple dips in US premarket!

Euro Area core inflation above estiamtes! EURUSD under key resistance!

The content of this report has been created by XTB S.A., with its registered office in Warsaw, at Prosta 67, 00-838 Warsaw, Poland, (KRS number 0000217580) and supervised by Polish Supervision Authority ( No. DDM-M-4021-57-1/2005). This material is a marketing communication within the meaning of Art. 24 (3) of Directive 2014/65/EU of the European Parliament and of the Council of 15 May 2014 on markets in financial instruments and amending Directive 2002/92/EC and Directive 2011/61/EU (MiFID II). Marketing communication is not an investment recommendation or information recommending or suggesting an investment strategy within the meaning of Regulation (EU) No 596/2014 of the European Parliament and of the Council of 16 April 2014 on market abuse (market abuse regulation) and repealing Directive 2003/6/EC of the European Parliament and of the Council and Commission Directives 2003/124/EC, 2003/125/EC and 2004/72/EC and Commission Delegated Regulation (EU) 2016/958 of 9 March 2016 supplementing Regulation (EU) No 596/2014 of the European Parliament and of the Council with regard to regulatory technical standards for the technical arrangements for objective presentation of investment recommendations or other information recommending or suggesting an investment strategy and for disclosure of particular interests or indications of conflicts of interest or any other advice, including in the area of investment advisory, within the meaning of the Trading in Financial Instruments Act of 29 July 2005 (i.e. Journal of Laws 2019, item 875, as amended). The marketing communication is prepared with the highest diligence, objectivity, presents the facts known to the author on the date of preparation and is devoid of any evaluation elements. The marketing communication is prepared without considering the client’s needs, his individual financial situation and does not present any investment strategy in any way. The marketing communication does not constitute an offer of sale, offering, subscription, invitation to purchase, advertisement or promotion of any financial instruments. XTB S.A. is not liable for any client’s actions or omissions, in particular for the acquisition or disposal of financial instruments, undertaken on the basis of the information contained in this marketing communication. In the event that the marketing communication contains any information about any results regarding the financial instruments indicated therein, these do not constitute any guarantee or forecast regarding the future results.