- US equity indices extend gains, led by another strong rally in technology stocks, while European stocks lag on higher oil prices

- US producer inflation (PPI) came in below expectations, with producer prices unexpectedly falling 0.3% month over month.

- The US dollar is edging slightly lower, although the USD Index continues to hold above the key 100 level.

- US equity indices extend gains, led by another strong rally in technology stocks, while European stocks lag on higher oil prices

- US producer inflation (PPI) came in below expectations, with producer prices unexpectedly falling 0.3% month over month.

- The US dollar is edging slightly lower, although the USD Index continues to hold above the key 100 level.

The technology sector is once again driving gains across global equity markets, as investors try to reconcile a very strong earnings season with rising geopolitical risks in the Middle East. Market attention is focused simultaneously on AI-related corporate results, oil prices, and the outlook for Federal Reserve policy following weaker-than-expected US CPI data. The latest US PPI report reinforced yesterday’s CPI signal, with producer prices falling 0.3% month over month and the annual increase coming in below expectations.

- European stocks lag with lower weight of technology stocks. Euro Stoxx 50 is traded mostly flat, while German DAX drops 0.5%

- Nasdaq 100 futures are up 0.5%, while S&P 500 futures gain 0.25%, supported by very strong results from semiconductor companies.

- ASML shares are rising nearly 8% after the company raised its sales outlook and announced plans to increase production of chipmaking equipment used in AI infrastructure.

- SK Hynix is gaining 9%, catching up with the earlier rise in the memory producer’s US-listed ADRs.

- Brent crude is advancing for a third consecutive session and is trading at around $85.60 per barrel following another wave of US strikes on targets in Iran and Donald Trump’s pledge to intensify military action.

- Despite the geopolitical tensions, oil prices remain well below the earlier highs above $100 per barrel, while investors are increasingly turning their attention to the corporate earnings season.

- The yield on the 10-year US Treasury is edging 1 basis point higher to 4.60%, with a similar move also visible across European bond markets.

- The US dollar remains relatively stable, while markets have largely ruled out a Fed rate hike at the next meeting but continue to price in a high probability of a move in September.

US producer price inflation unexpectedly fell by 0.3% month over month, compared with expectations for a 0.1% increase, while the annual rate came in at 5.6%, below the 6.2% forecast. Core PPI also slowed more sharply than expected, to 4.7% year over year versus a 5.1% forecast, while the NY Empire State index delivered a clear positive surprise, rising to 15 compared with expectations of 9.

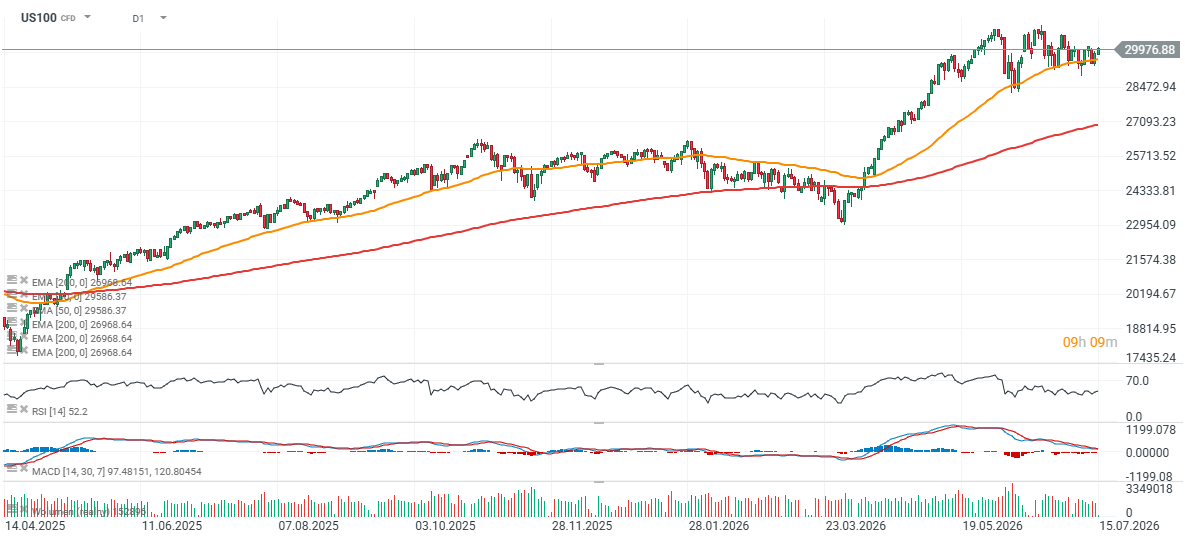

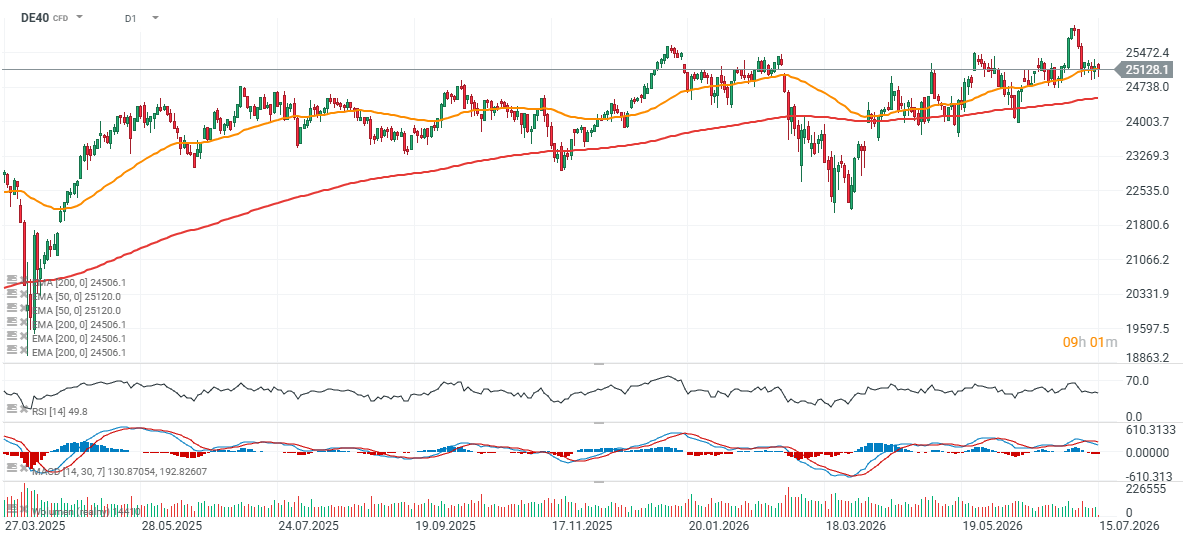

US100, DE40 (D1 interval)

The US100 contract is moving toward the 30,000-point level and is trading above the 50-day exponential moving average, marked by the orange line, at around 29,960 points. Investors continue to buy stocks linked to AI infrastructure, supporting overall market sentiment.

Source: xStation5

Futures on German DAX are slightly down today, testing the 25,000 - 25,1000 pts level, near to the support from EMA50 (the orange line).

Source: xStation5

Daily Summary 🗽 Wall Street Holds Firm Despite Weakness in Memory Stocks, Rising Oil Price

Moderna shares slide despite mFlusiva success 📉 What's next for the mRNA vaccines market giant?

Stock of the Week: Arista Networks—A Second-Tier Technology with Top-Tier Results

US Open: S&P 500 shows strength as semiconductor lags 🚩 Western Digital down 12%

The content of this report has been created by XTB S.A., with its registered office in Warsaw, at Prosta 67, 00-838 Warsaw, Poland, (KRS number 0000217580) and supervised by Polish Supervision Authority ( No. DDM-M-4021-57-1/2005). This material is a marketing communication within the meaning of Art. 24 (3) of Directive 2014/65/EU of the European Parliament and of the Council of 15 May 2014 on markets in financial instruments and amending Directive 2002/92/EC and Directive 2011/61/EU (MiFID II). Marketing communication is not an investment recommendation or information recommending or suggesting an investment strategy within the meaning of Regulation (EU) No 596/2014 of the European Parliament and of the Council of 16 April 2014 on market abuse (market abuse regulation) and repealing Directive 2003/6/EC of the European Parliament and of the Council and Commission Directives 2003/124/EC, 2003/125/EC and 2004/72/EC and Commission Delegated Regulation (EU) 2016/958 of 9 March 2016 supplementing Regulation (EU) No 596/2014 of the European Parliament and of the Council with regard to regulatory technical standards for the technical arrangements for objective presentation of investment recommendations or other information recommending or suggesting an investment strategy and for disclosure of particular interests or indications of conflicts of interest or any other advice, including in the area of investment advisory, within the meaning of the Trading in Financial Instruments Act of 29 July 2005 (i.e. Journal of Laws 2019, item 875, as amended). The marketing communication is prepared with the highest diligence, objectivity, presents the facts known to the author on the date of preparation and is devoid of any evaluation elements. The marketing communication is prepared without considering the client’s needs, his individual financial situation and does not present any investment strategy in any way. The marketing communication does not constitute an offer of sale, offering, subscription, invitation to purchase, advertisement or promotion of any financial instruments. XTB S.A. is not liable for any client’s actions or omissions, in particular for the acquisition or disposal of financial instruments, undertaken on the basis of the information contained in this marketing communication. In the event that the marketing communication contains any information about any results regarding the financial instruments indicated therein, these do not constitute any guarantee or forecast regarding the future results.