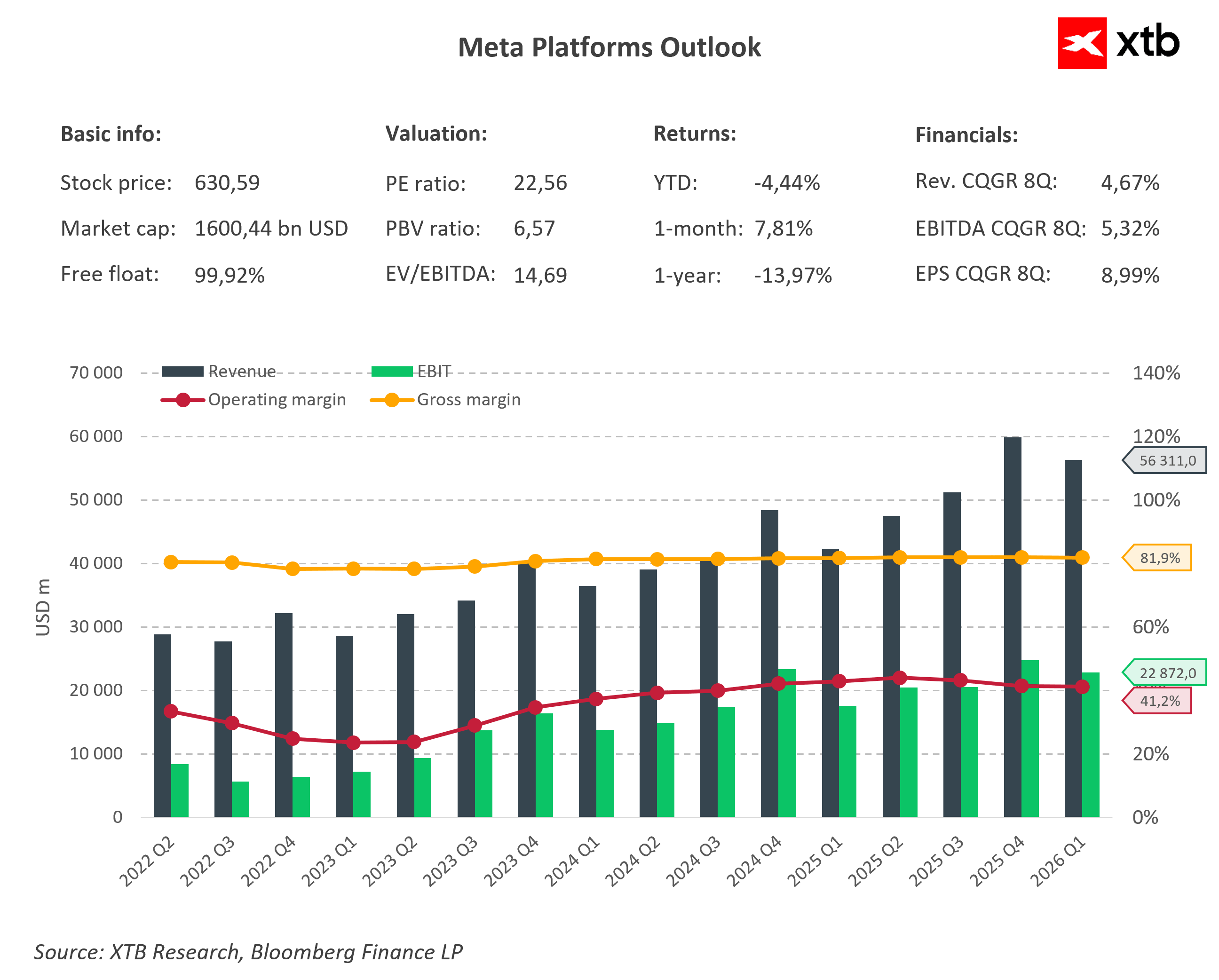

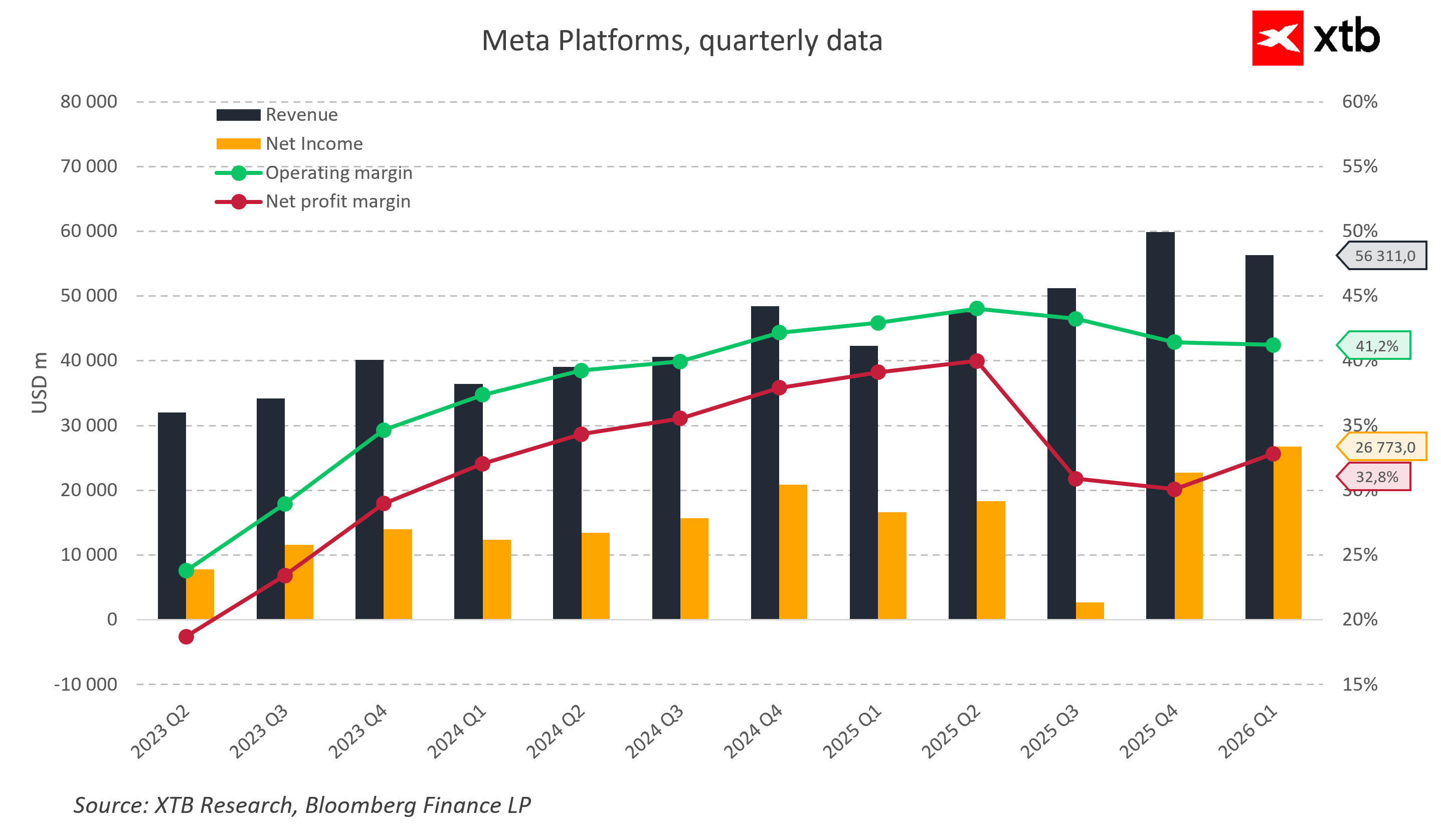

Meta is once again attracting market attention, this time not because of another artificial intelligence model, but because of a strategic decision regarding its own computing infrastructure. The company announced yesterday that it will begin producing its own AI chips as early as September, a move aimed at increasing control over costs and reducing dependence on external suppliers of the most advanced processors. At the same time, reports emerging in early July suggested that Meta is exploring options to commercialize part of its unused computing capacity.

The combination of these two moves highlights a significant shift in how the largest technology companies are approaching artificial intelligence. The race to build AI infrastructure is far from over, but the focus is increasingly moving beyond the scale of investment toward the efficiency and utilization of the resources being deployed.

One of the biggest constraints on AI development has been access to sufficient computing power. Demand for Nvidia’s most advanced chips has, for a long time, exceeded the production capacity of the broader ecosystem, forcing major technology companies to compete for access to accelerators required to train and operate increasingly sophisticated AI models.

The market is now beginning to ask a different question: will simply building more infrastructure remain the main source of competitive advantage, or will the ability to manage and optimize massive AI investments become increasingly important?

Meta’s own AI chip initiative is a key part of this strategy. The company is developing chips from the MTIA family, designed for specific applications such as recommendation systems, advertising and the operation of its own artificial intelligence models. The goal is not to completely replace Nvidia’s solutions, but rather to gain greater control over infrastructure and potentially reduce computing costs.

According to available reports, production of the new chips is expected to begin in September, with Meta working alongside semiconductor industry partners, including Broadcom and TSMC. The company is also planning a significant expansion of its computing resources, highlighting that AI infrastructure remains one of its highest strategic priorities.

It is important to note that Meta’s move into custom AI chips is only one part of a much broader technological offensive. The company is simultaneously accelerating the development of its own artificial intelligence models, with one of the latest examples being Muse Spark 1.1, which is expected to represent another step in its competition with solutions developed by the leading players in the AI industry.

The development of proprietary models shows that Meta does not want to remain only a consumer of technology provided by external partners. Instead, the company is attempting to build a complete AI ecosystem covering models, software and hardware infrastructure.

This is why the decision to produce its own chips should not be viewed solely as an attempt to reduce dependence on Nvidia. Meta is seeking greater control over the entire AI value chain, from designing models and training them, through deployment, all the way to the hardware powering these systems. Such a strategy could allow the company to better manage costs and adapt its infrastructure more quickly to its own requirements.

For Nvidia, this does not necessarily represent an immediate threat. Demand for the most advanced AI accelerators remains extremely strong, and Nvidia’s solutions continue to serve as the industry standard for the most demanding applications. Custom chips developed by hyperscalers should be viewed primarily as an effort to optimize costs and increase strategic independence rather than as a complete shift away from the current model.

At the same time, Meta’s move shows that the AI market is entering another stage of development. The initial phase was focused primarily on securing access to hardware and rapidly expanding data center capacity. The next challenge is increasingly about converting this infrastructure into measurable business value.

In this context, reports regarding Meta’s potential commercialization of unused computing capacity are particularly interesting. If the company decides to make part of its resources available to external users, it would signal that AI infrastructure is beginning to be viewed not only as internal technological support, but also as an asset that can generate additional revenue.

Such a development would have broader implications for the entire sector. The market could gradually move from a phase where the key priority was simply securing computing capacity into a stage where utilization rates and efficiency become the main focus. For the largest technology companies, this means greater pressure to optimize spending and demonstrate stronger returns on AI investments.

In the short term, Meta’s announcements create a mixed picture for the semiconductor sector. On one hand, they confirm that the largest technology companies continue to increase AI spending and remain committed to expanding infrastructure. Meta’s planned increase in computing capacity remains a positive signal for the broader supply chain.

On the other hand, the development of proprietary chips could gradually reduce demand for some externally supplied solutions from companies such as Nvidia and AMD in the coming years. The largest customers of these companies are increasingly attempting to design specialized chips tailored to their own applications, which could reshape parts of the semiconductor market.

Over the medium term, the key question will be how quickly hyperscalers’ custom solutions can reach the required level of performance. If companies such as Meta, Google and Amazon succeed in creating specialized chips that are better optimized for their own workloads, this could influence the future structure of the AI market.

This does not mean the end of Nvidia’s dominance. The company still holds a significant technological advantage, a powerful CUDA ecosystem and a broad customer base. A more likely scenario is the emergence of a market where Nvidia remains the leading provider of general-purpose AI infrastructure, while certain specialized workloads are increasingly handled by internally developed chips from the largest technology companies.

Without a doubt, the biggest risk for the entire AI ecosystem remains the pace of monetization of current investments. Spending on data centers has reached unprecedented levels, and the market is increasingly analyzing whether these enormous expenditures are translating into proportional revenue growth. More efficient AI models, the expansion of lower-cost open-source solutions and pressure to reduce computing expenses could reshape the economics of the entire sector.

Meta is therefore at a very interesting point. The company is simultaneously expanding its computing resources, developing proprietary chips and looking for ways to better utilize existing infrastructure. This is not a signal that the AI boom is ending, but rather that the market is moving into a new phase where the winners will be those capable of combining investment scale with operational efficiency.

Market Wrap: European equities at 3-week highs! Apple dips in US premarket!

Morning Wrap: AI Fuels the Rebound. Technology Makes a Strong Comeback

Apple is still impressive, but the market is no longer impressed

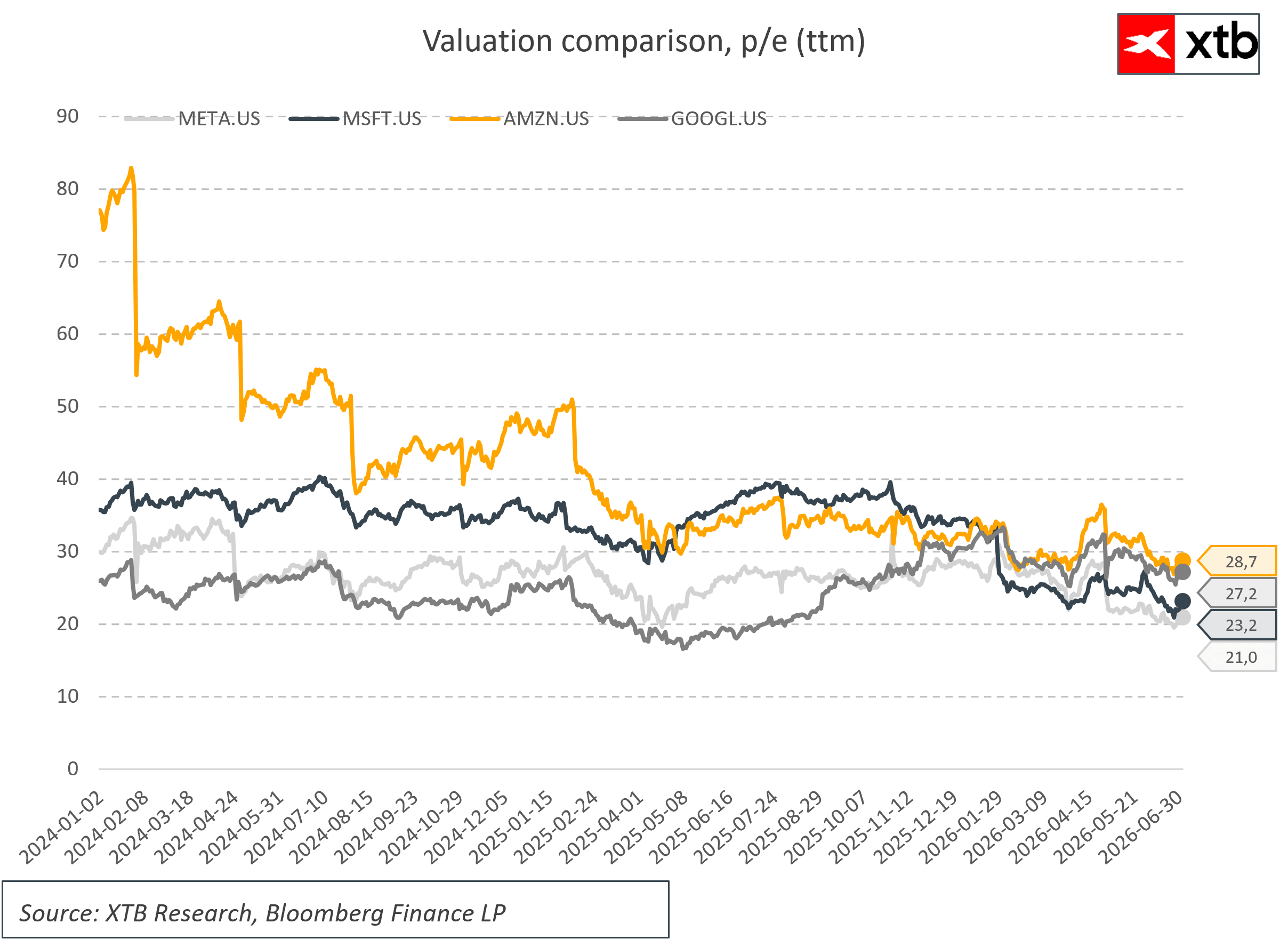

Amazon’s massive AI bet is starting to pay off

The content of this report has been created by XTB S.A., with its registered office in Warsaw, at Prosta 67, 00-838 Warsaw, Poland, (KRS number 0000217580) and supervised by Polish Supervision Authority ( No. DDM-M-4021-57-1/2005). This material is a marketing communication within the meaning of Art. 24 (3) of Directive 2014/65/EU of the European Parliament and of the Council of 15 May 2014 on markets in financial instruments and amending Directive 2002/92/EC and Directive 2011/61/EU (MiFID II). Marketing communication is not an investment recommendation or information recommending or suggesting an investment strategy within the meaning of Regulation (EU) No 596/2014 of the European Parliament and of the Council of 16 April 2014 on market abuse (market abuse regulation) and repealing Directive 2003/6/EC of the European Parliament and of the Council and Commission Directives 2003/124/EC, 2003/125/EC and 2004/72/EC and Commission Delegated Regulation (EU) 2016/958 of 9 March 2016 supplementing Regulation (EU) No 596/2014 of the European Parliament and of the Council with regard to regulatory technical standards for the technical arrangements for objective presentation of investment recommendations or other information recommending or suggesting an investment strategy and for disclosure of particular interests or indications of conflicts of interest or any other advice, including in the area of investment advisory, within the meaning of the Trading in Financial Instruments Act of 29 July 2005 (i.e. Journal of Laws 2019, item 875, as amended). The marketing communication is prepared with the highest diligence, objectivity, presents the facts known to the author on the date of preparation and is devoid of any evaluation elements. The marketing communication is prepared without considering the client’s needs, his individual financial situation and does not present any investment strategy in any way. The marketing communication does not constitute an offer of sale, offering, subscription, invitation to purchase, advertisement or promotion of any financial instruments. XTB S.A. is not liable for any client’s actions or omissions, in particular for the acquisition or disposal of financial instruments, undertaken on the basis of the information contained in this marketing communication. In the event that the marketing communication contains any information about any results regarding the financial instruments indicated therein, these do not constitute any guarantee or forecast regarding the future results.