- Micron shares have surged more than 1,800% since ChatGPT's launch in November 2022, outperforming Nvidia over the same period.

- The company is experiencing a period of rapid expansion in margins, earnings, and revenue following the memory market downturn.

- Like Nvidia, Micron has become one of the key beneficiaries of the global AI infrastructure investment cycle.

- Micron is currently valued at approximately $1.1 trillion, compared with more than $5 trillion for Nvidia.

- Micron shares have surged more than 1,800% since ChatGPT's launch in November 2022, outperforming Nvidia over the same period.

- The company is experiencing a period of rapid expansion in margins, earnings, and revenue following the memory market downturn.

- Like Nvidia, Micron has become one of the key beneficiaries of the global AI infrastructure investment cycle.

- Micron is currently valued at approximately $1.1 trillion, compared with more than $5 trillion for Nvidia.

Micron is the largest U.S. memory chip manufacturer, and although the company has rapidly climbed into the ranks of the world's largest businesses, dethroning Nvidia as Wall Street's most valuable company would likely take years. Such an outcome would probably require two conditions to occur simultaneously: a structural shortage in the memory chip market and sustained long-term demand for AI infrastructure, particularly high-performance memory.

- Over the past few quarters, Micron has become one of Wall Street's biggest success stories. The company has evolved from a large semiconductor manufacturer into a trillion-dollar technology giant, currently ranking as the world's 13th most valuable publicly traded company with a market capitalization of approximately $1.1 trillion. Nvidia, however, still leads the global rankings by selling AI computing power, while Micron provides the memory that makes that computing power possible.

- To surpass Nvidia in market value, Micron's stock would have to rise roughly fivefold from current levels, assuming Nvidia's market capitalization remained unchanged at around $5 trillion. Such a scenario is difficult to imagine, however, because both companies benefit from the same AI megatrend. If Micron continues to grow, Nvidia would likely continue expanding as well, making it extremely challenging for Micron to take over the title of the world's most valuable company.

- That does not mean Micron lacks upside potential—quite the opposite. In its latest earnings report, the company delivered nearly 350% year-over-year revenue growth to approximately $41.5 billion, while GAAP net income increased 85-fold to $28.24 billion from just $330 million in the same quarter a year earlier. These are extraordinary growth rates, and many investors believe the company could continue reporting exceptional financial performance as demand for AI memory remains strong.

Nvidia and Micron: Two Businesses Riding the Same AI Wave

Micron and Nvidia are among the biggest beneficiaries of the artificial intelligence boom, but they generate profits from entirely different parts of the same AI value chain. Hyperscalers are expected to invest roughly $800 billion in AI infrastructure this year alone, while BlackRock estimates cumulative investment could exceed $3 trillion before the end of the decade. These unprecedented capital expenditures directly support the growth of both companies, although investors should remember that strong business performance does not always translate into rising share prices.

Both companies are fundamental pillars of AI infrastructure and benefit from growing investments by hyperscalers such as Microsoft, Amazon, Meta, Google, and Oracle.

Demand for their products is primarily driven by the construction of AI data centers and the rapid expansion of generative AI models.

Both companies are currently generating record revenue, margins, and cash flows thanks to hundreds of billions of dollars in AI-related capital spending.

Nvidia sells AI GPUs, complete server systems, InfiniBand networking solutions, and the CUDA software ecosystem. It provides the computing platform powering modern artificial intelligence and enjoys a substantial technological and ecosystem advantage.

Micron, meanwhile, manufactures DRAM, HBM, and NAND memory. For AI applications, High Bandwidth Memory (HBM) is the most critical product, as it works alongside processors developed by Nvidia, AMD, Google, Amazon, and other AI chip designers.

In simple terms, Nvidia supplies the "brain" of an AI server—the processors that perform the computations together with the accompanying software stack. Micron provides the "working memory" that allows those GPUs to process massive AI models at extremely high bandwidth.

Nvidia is widely viewed as the higher-quality business thanks to its technological leadership, consistently high margins, and the competitive moat created by its CUDA ecosystem, all of which justify premium valuation multiples.

Micron remains the largest memory manufacturer in the United States, operating in a much more cyclical and competitive segment of the semiconductor industry. Although AI has dramatically improved the company's outlook, its financial performance still depends far more on memory pricing and supply-demand dynamics than on proprietary software or network effects.

Both companies remain exposed to the risk of an eventual slowdown in AI spending or a cyclical downturn in semiconductor demand. However, neither company currently expects such a scenario, and it would be a mistake to assume Nvidia would be significantly more resilient than Micron if AI investment slowed materially. Should investor sentiment toward AI reverse, both companies would likely face meaningful pressure. At the same time, Micron may continue to outperform Nvidia during this phase of the AI cycle, as Nvidia was the primary beneficiary of the first wave of AI infrastructure spending. If the current earnings forecasts prove accurate and the structural shortage of advanced memory persists for years, Micron has a realistic opportunity to join the ranks of America's very largest companies.

Morgan Stanley's Bull Case for Micron: What Does the Bank See?

Morgan Stanley recently presented an exceptionally bullish scenario for Micron, forecasting an unprecedented expansion in both the company's scale and profitability between 2026 and 2027. According to the bank's model, Micron could generate nearly $400 billion in cumulative non-GAAP operating income over the two-year period—an amount equivalent to roughly 40% of the company's current market capitalization.

The forecasts include:

- Revenue of $172.9 billion in 2026

- Operating income of $140.7 billion

- Operating margin of 81.4%

- Revenue increasing to $285.9 billion in 2027

- Operating income rising to $248.7 billion

- Further expansion of operating margin to 87%

Morgan Stanley also expects gross margins to reach 85%–89.5%, an extraordinary level for what has historically been one of the semiconductor industry's most cyclical businesses. Such profitability would likely trigger a significant re-rating of Micron's valuation.

The foundation of this aggressive scenario is explosive demand for High Bandwidth Memory (HBM), which has become an essential component of AI accelerators. As hyperscalers continue expanding AI data centers, advanced memory has emerged as one of the industry's most critical supply bottlenecks, allowing Micron to benefit from both rising shipment volumes and exceptionally strong pricing.

A New Cycle for the Memory Industry

Morgan Stanley's key investment thesis is that the current memory cycle differs fundamentally from previous ones because demand is now being driven by the structural expansion of artificial intelligence. If demand for HBM remains elevated for years rather than quarters, Micron could gradually stop being viewed as a traditional cyclical memory manufacturer and instead be valued as one of the primary infrastructure beneficiaries of the AI revolution.

At the same time, this represents an extremely demanding scenario. The biggest risks include increasing competition from SK Hynix and Samsung—both now among the world's largest technology companies—higher industry supply, pricing pressure, execution risks, and the eventual return of the traditional memory cycle. Even partial realization of Morgan Stanley's assumptions, however, could still translate into substantial earnings growth and further upside for Micron shares.

Morgan Stanley's model assumes Micron will achieve operating margins exceeding 80%, significantly higher than Nvidia currently generates, despite Nvidia being widely regarded as the most profitable AI infrastructure company in the world. Achieving such margins would require memory prices to remain exceptionally high for many years.

Based on Morgan Stanley's forecasts, Micron's revenue this year would still be roughly 50% lower than Nvidia's expected sales, while operating income would be approximately 40% lower. By next year, however, the gap could narrow considerably, with Micron's revenue projected to be only about 40% below Nvidia's and operating income approximately 30% lower.

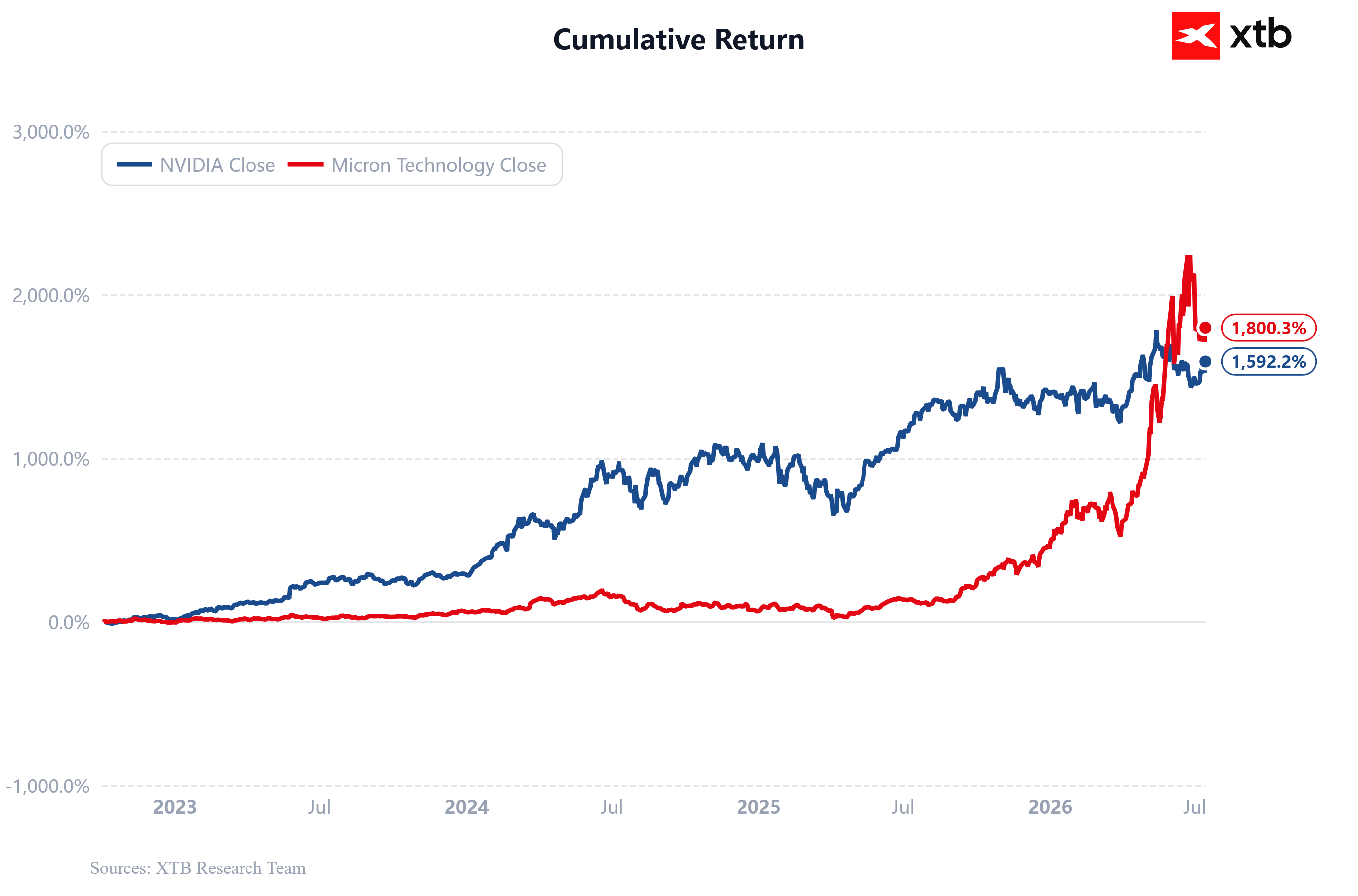

Micron Shares Have Outperformed Nvidia Since ChatGPT

Micron shares have already risen more than 18-fold since the launch of ChatGPT in November 2022, compared with approximately a 15-fold gain for Nvidia over the same period. Micron's outperformance has accelerated during the past several quarters as the market for advanced memory chips has become increasingly supply-constrained.

Source: XTB Research

Micron Trades at a Lower Valuation Than Nvidia. What Do the Charts Suggest?

While investors currently value Nvidia at approximately 21 times expected earnings over the next 12 months, Micron trades at a much lower forward earnings multiple of around 13. For a company of Micron's size and growth profile, this valuation appears unusually modest and may indicate meaningful upside potential if earnings growth proves sustainable.

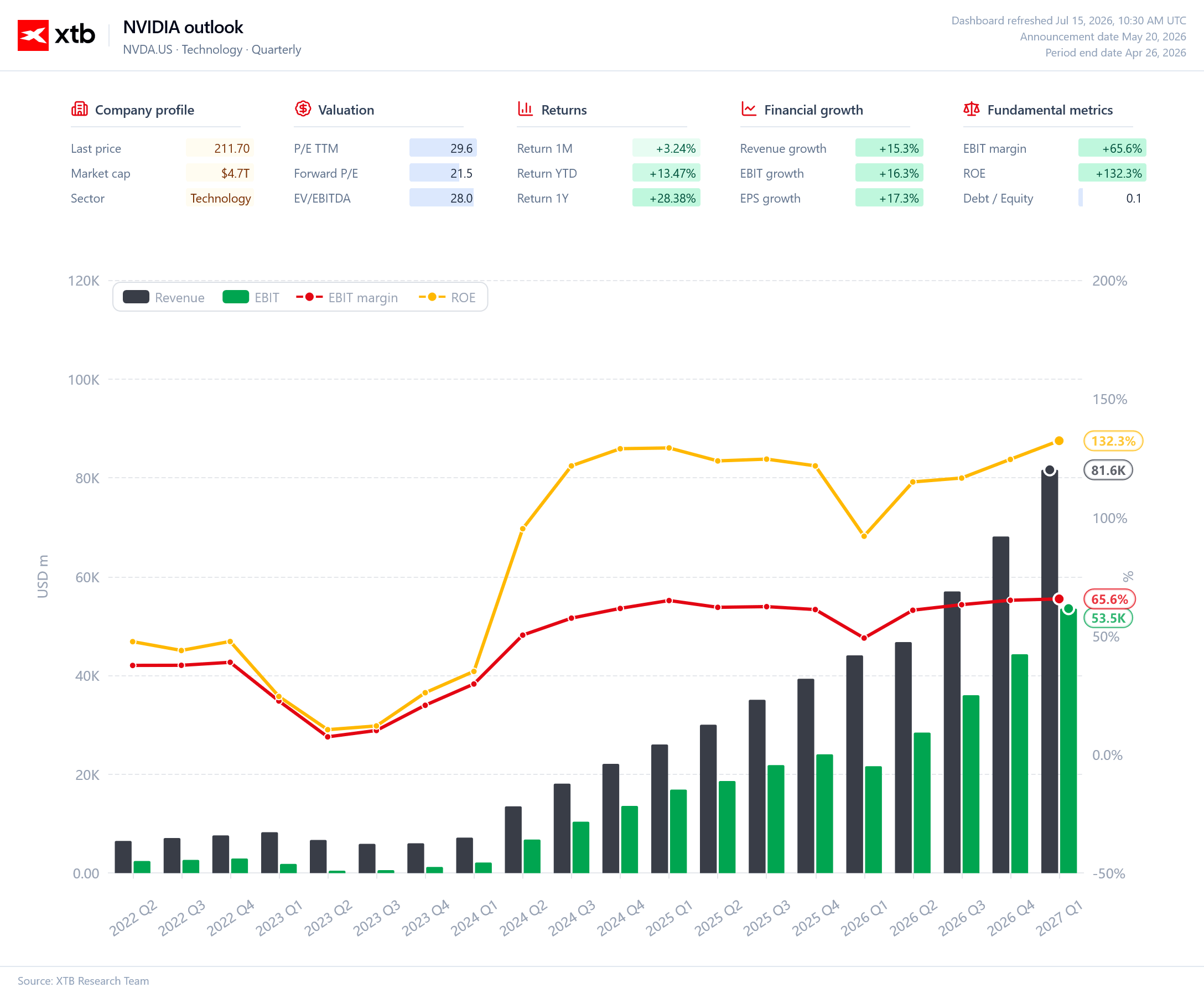

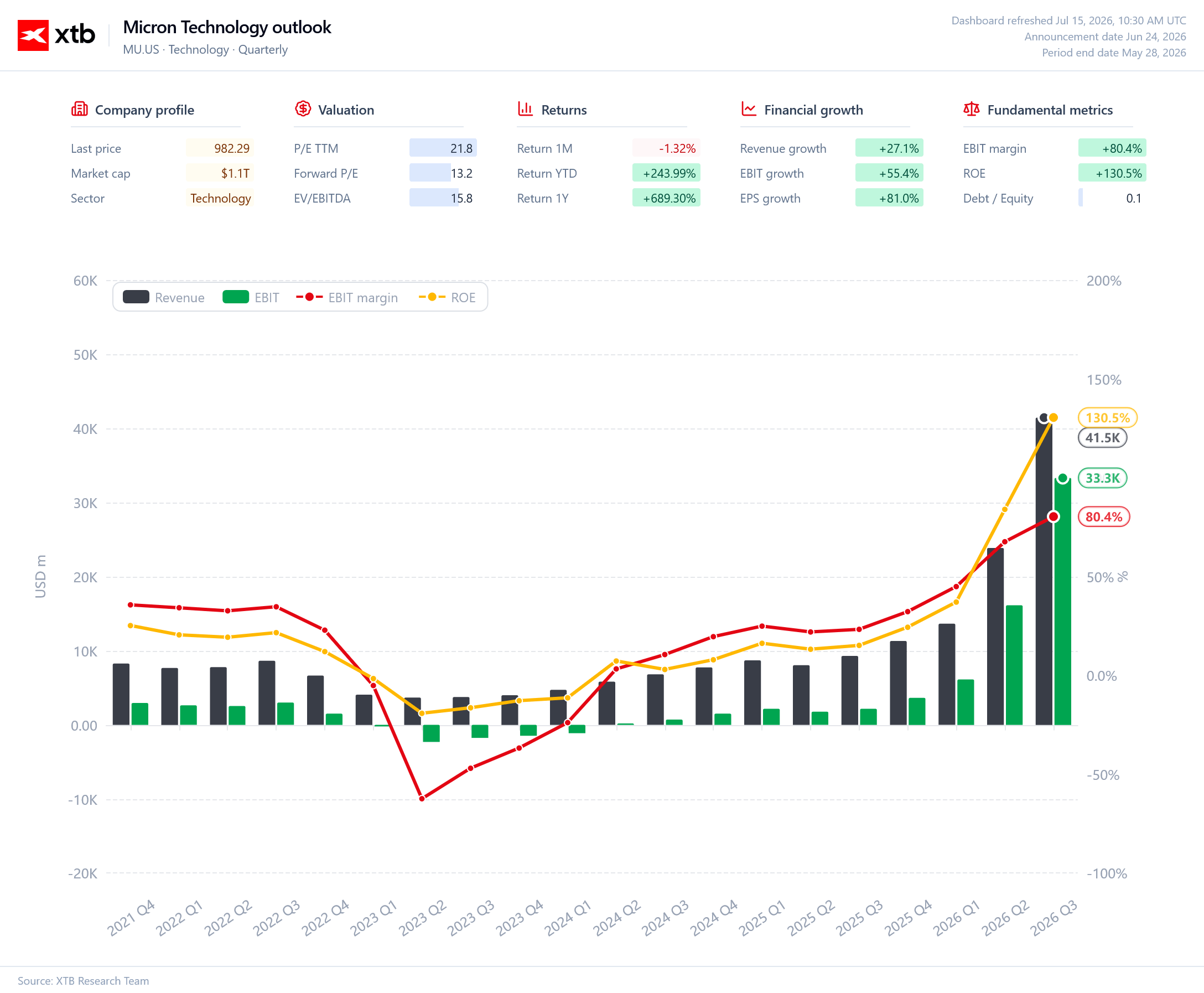

The charts below illustrate that Nvidia has delivered more stable growth while maintaining exceptionally high profitability over many consecutive quarters. Micron, by contrast, remains at an earlier stage of a powerful recovery following the cyclical downturn in the memory market. At the same time, Micron's improvement in margins and earnings is currently outpacing Nvidia's, driven by extraordinary demand for HBM memory. In practice, Nvidia remains the undisputed leader of the AI ecosystem, while Micron has become one of the most important beneficiaries of the rapidly growing demand for memory powering AI accelerators.

Nvidia vs. Micron: A Comparison of the Financial Outlook

Nvidia's financial performance continues to reinforce the company's dominant position in AI infrastructure and the exceptional quality of its business model. Revenue and operating income have continued to grow steadily, while EBIT margins remain exceptionally high at around 66%. Return on equity (ROE) exceeds 130%, highlighting the company's outstanding profitability. Nvidia remains the world's leading supplier of AI computing power, enabling it to maintain premium margins despite its enormous scale. At the same time, the company trades at valuation multiples that remain below many of the largest semiconductor peers, reflecting strong earnings growth. Nvidia continues to lead the current AI investment cycle.

Source: XTB Research

Micron's financial profile tells a different story. The company has emerged from one of the deepest downturns in memory industry history and entered one of the strongest recoveries ever seen in the semiconductor sector. Revenue and operating income are growing almost exponentially as demand for HBM memory used in AI accelerators continues to surge. Profitability has improved dramatically, with EBIT margins already exceeding 80%, while return on equity has climbed to around 130%, comparable to Nvidia's. Despite this rapid improvement, Micron continues to trade at a relatively modest valuation considering its growth profile. If the current AI investment cycle persists, Micron appears well positioned to remain one of the biggest beneficiaries of expanding AI infrastructure spending.

Source: XTB Research

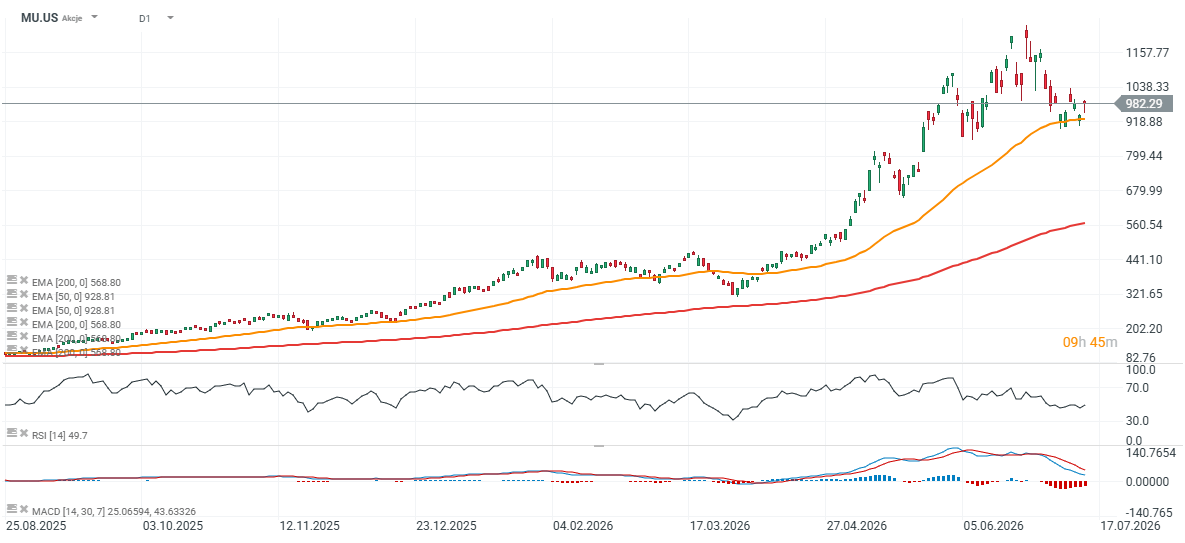

Micron Shares (D1 Chart)

Micron shares have already experienced a correction of nearly 20% from their recent highs, with the decline finding support around the 50-day exponential moving average (EMA50, orange line). The first major resistance zone lies between approximately $1,050 and $1,100, followed by the all-time highs near $1,200 per share. On the downside, the $900 area represents an important technical support level for maintaining the current bullish momentum.

The 200-day exponential moving average (EMA200, red line)—a level Nvidia has tested several times during the AI bull market despite its long-term uptrend—is currently located near $560 per share. A decline toward that level would imply a correction of roughly 35% from current prices.

Source: xStation5

Eryk Szmyd XTB Financial Markets Analyst

Daily Summary 🗽 Wall Street Holds Firm Despite Weakness in Memory Stocks, Rising Oil Price

Moderna shares slide despite mFlusiva success 📉 What's next for the mRNA vaccines market giant?

Stock of the Week: Arista Networks—A Second-Tier Technology with Top-Tier Results

US Open: S&P 500 shows strength as semiconductor lags 🚩 Western Digital down 12%

The content of this report has been created by XTB S.A., with its registered office in Warsaw, at Prosta 67, 00-838 Warsaw, Poland, (KRS number 0000217580) and supervised by Polish Supervision Authority ( No. DDM-M-4021-57-1/2005). This material is a marketing communication within the meaning of Art. 24 (3) of Directive 2014/65/EU of the European Parliament and of the Council of 15 May 2014 on markets in financial instruments and amending Directive 2002/92/EC and Directive 2011/61/EU (MiFID II). Marketing communication is not an investment recommendation or information recommending or suggesting an investment strategy within the meaning of Regulation (EU) No 596/2014 of the European Parliament and of the Council of 16 April 2014 on market abuse (market abuse regulation) and repealing Directive 2003/6/EC of the European Parliament and of the Council and Commission Directives 2003/124/EC, 2003/125/EC and 2004/72/EC and Commission Delegated Regulation (EU) 2016/958 of 9 March 2016 supplementing Regulation (EU) No 596/2014 of the European Parliament and of the Council with regard to regulatory technical standards for the technical arrangements for objective presentation of investment recommendations or other information recommending or suggesting an investment strategy and for disclosure of particular interests or indications of conflicts of interest or any other advice, including in the area of investment advisory, within the meaning of the Trading in Financial Instruments Act of 29 July 2005 (i.e. Journal of Laws 2019, item 875, as amended). The marketing communication is prepared with the highest diligence, objectivity, presents the facts known to the author on the date of preparation and is devoid of any evaluation elements. The marketing communication is prepared without considering the client’s needs, his individual financial situation and does not present any investment strategy in any way. The marketing communication does not constitute an offer of sale, offering, subscription, invitation to purchase, advertisement or promotion of any financial instruments. XTB S.A. is not liable for any client’s actions or omissions, in particular for the acquisition or disposal of financial instruments, undertaken on the basis of the information contained in this marketing communication. In the event that the marketing communication contains any information about any results regarding the financial instruments indicated therein, these do not constitute any guarantee or forecast regarding the future results.