-

Asia-Pacific indices traded at mixed levels during Wednesday's trading session, given the lingering uncertainty surrounding the Chinese economy. Japan's Nikkei gained close to 0.85%, Australia's S&P/ASX 200 traded 0.42% above yesterday's closing levels and India's Nifty 50 rallied close to 0.25%. The Hang Seng Index is currently leading the declines in APAC markets (-1.17%).

-

Yesterday's session on Wall Street was dominated by gains in the Russell 2000 index, which benefited from capital inflows into ETFs based on regional US banks.

-

Futures on the DAX and S&P 500 indices pointed to a slightly higher opening of the cash session on markets in Europe and the US.

-

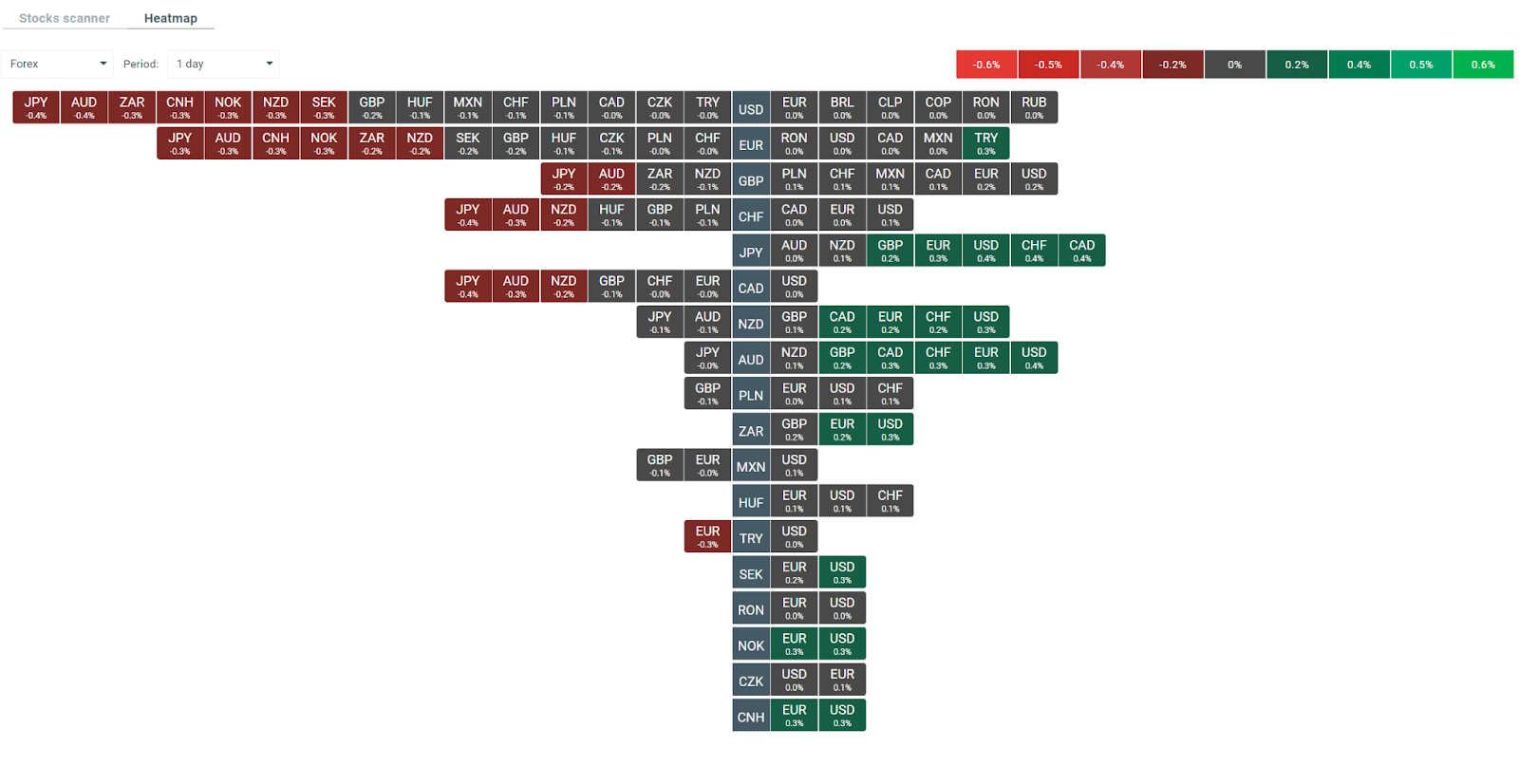

The dollar index has stopped its recent downward momentum, nevertheless it remains below the psychological barrier of 100. The EURUSD pair is trading above the resistance of 1.12, weakness is currently being recorded in the JPY, the USDJPY pair is back above the 139 zone.

-

Key topics in today's session include the UK inflation reading, Eurozone inflation and quarterly results from Tesla, Netflix, IBM and Goldman Sachs.

-

ASML reported Q2 2023 orders of €4.5bn against expectations of €3.98bn. Furthermore, net sales also surprised on the upside at €6.9bn (expected: €6.69bn).

-

The company's gross margin increased to 51.3% (50.6% expected). The company raised its earnings forecasts for 2023. The company's CEO added that the US-imposed semiconductor trade regulations will not affect the company's results.

-

Nissan and Renault are expected to announce a new alliance agreement within days.

-

China's Ministry of Industry says the industry is stagnating amid insufficient demand and falling revenues.

-

Inflation data from New Zealand came in above expectations, however, the money market saw no change in predictions regarding the next rate hike by the RBNZ. The NZDUSD pair erases early rally.

-

Credit Suisse raised its year-end forecast for the S&P 500 to 4700 points from its previous 4050 points.

-

Citi's global head of commodity market analysis sees oil in the $70 to $90 range.

- Data from the private oil market research (API) shows a smaller increase in oil inventories than expected.

-

The cryptocurrency market is seeing improved sentiment. Bitcoin gains 1%, Ethereum adds 0.9% and Cardano is trading 4.5% higher.

-

Precious metals are slightly halting yesterday's upward wave. Gold is currently losing 0.1% and testing the 1976 USD level, while silver is subtracting 0.5% and holding in the $25 zone.

Heatmap on the FX market showing the volatility on each currency pair at the moment. Source: xStation 5

FX Weekly: Yen Returns to Losses, Dollar Under Pressure (10.08.2026)

Economic Calendar: Markets Awaken After a Weekend of Geopolitical Deadlock🚢

Morning Wrap: No Breakthrough in the Strait of Hormuz; Investors React to Berkshire Hathaway's Earnings

NFP much below expectations! 🚨EURUSD spikes 📈

The content of this report has been created by XTB S.A., with its registered office in Warsaw, at Prosta 67, 00-838 Warsaw, Poland, (KRS number 0000217580) and supervised by Polish Supervision Authority ( No. DDM-M-4021-57-1/2005). This material is a marketing communication within the meaning of Art. 24 (3) of Directive 2014/65/EU of the European Parliament and of the Council of 15 May 2014 on markets in financial instruments and amending Directive 2002/92/EC and Directive 2011/61/EU (MiFID II). Marketing communication is not an investment recommendation or information recommending or suggesting an investment strategy within the meaning of Regulation (EU) No 596/2014 of the European Parliament and of the Council of 16 April 2014 on market abuse (market abuse regulation) and repealing Directive 2003/6/EC of the European Parliament and of the Council and Commission Directives 2003/124/EC, 2003/125/EC and 2004/72/EC and Commission Delegated Regulation (EU) 2016/958 of 9 March 2016 supplementing Regulation (EU) No 596/2014 of the European Parliament and of the Council with regard to regulatory technical standards for the technical arrangements for objective presentation of investment recommendations or other information recommending or suggesting an investment strategy and for disclosure of particular interests or indications of conflicts of interest or any other advice, including in the area of investment advisory, within the meaning of the Trading in Financial Instruments Act of 29 July 2005 (i.e. Journal of Laws 2019, item 875, as amended). The marketing communication is prepared with the highest diligence, objectivity, presents the facts known to the author on the date of preparation and is devoid of any evaluation elements. The marketing communication is prepared without considering the client’s needs, his individual financial situation and does not present any investment strategy in any way. The marketing communication does not constitute an offer of sale, offering, subscription, invitation to purchase, advertisement or promotion of any financial instruments. XTB S.A. is not liable for any client’s actions or omissions, in particular for the acquisition or disposal of financial instruments, undertaken on the basis of the information contained in this marketing communication. In the event that the marketing communication contains any information about any results regarding the financial instruments indicated therein, these do not constitute any guarantee or forecast regarding the future results.