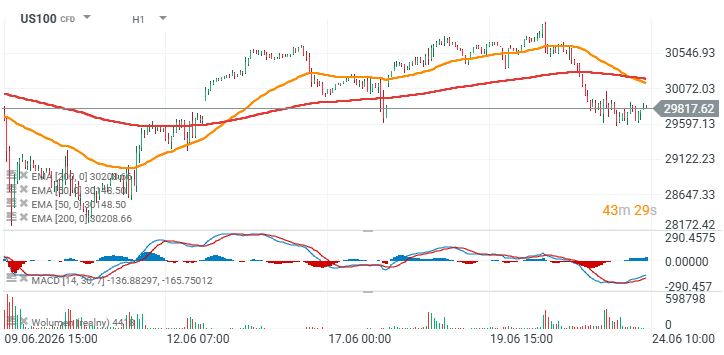

- Global equity markets are trying to stabilize after Tuesday’s AI-driven selloff, but investors remain cautious ahead of Micron’s earnings release today after the U.S. close, which could become an important test of demand for memory chips used in AI infrastructure. Nasdaq 100 futures (US100) are up 0.2%, while European index futures point to a calm open in Europe.

- SpaceX priced its first-ever bond issuance at $25 billion, offering notes maturing between 2031 and 2056. The stock gained only 0.5% after the U.S. close and has fallen as much as 22% in recent days. Proceeds are expected to be used to repay bridge financing and for general corporate purposes. The scale of the issuance shows that even the most dynamic technology companies are increasingly turning to debt markets, which is especially important in a high-rate environment.

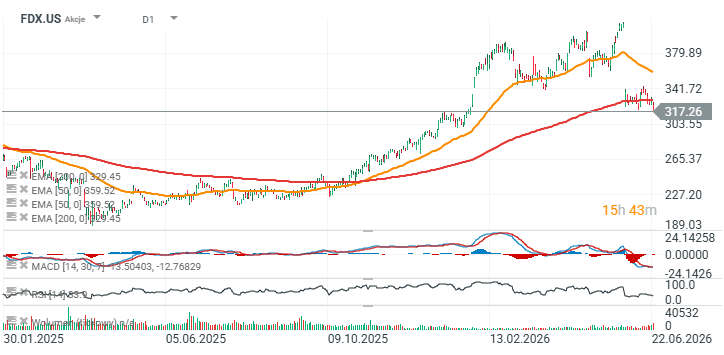

- FedEx also reported results after the close and remains a key barometer of global trade and economic activity. Shares fell 6% after the report and have lost nearly 25% in recent weeks. The company posted adjusted EPS of $6.31 versus $6.07 a year earlier, while revenue rose 13% year-over-year to $25 billion. Federal Express revenue increased 14% to $21.6 billion, and management guided for adjusted 2026 EPS of $16.90–18.10. The results suggest that transport and logistics activity remains relatively resilient despite broader slowdown concerns.

- The MSCI All Country World Index slipped 0.1%, while Asia’s broad equity benchmark finished 0.4% lower, giving back almost all of an earlier gain of nearly 1%. The move shows that risk appetite remains fragile.

- TSMC shares fell more than 3%, joining the broader semiconductor selloff after earlier pressure on U.S. technology names.

- U.S. equity futures edged slightly higher ahead of the Wall Street open, suggesting an attempt to recover after sharp losses, although the scale of the rebound remains limited.

- South Korea’s KOSPI recovered part of its losses as Samsung gained on reports that the company may announce a share buyback, but sentiment remains fragile after one of the steepest selloffs in the index’s history.

- Tuesday’s KOSPI slump was largely driven by a rapid unwinding of leveraged positions concentrated in semiconductor stocks and AI beneficiaries, showing how much of the rally had been supported by aggressive investor positioning.

- In FX markets, the classic defensive move was visible: the dollar strengthened to a seven-month high, while demand for U.S. Treasuries remained elevated. Investors are becoming more cautious toward risk-asset valuations while reassessing the impact of higher interest rates on markets.

- Oil continued to decline but did not provide meaningful relief for equity indices. Brent crude moved toward $76 per barrel as the market gradually removed the geopolitical risk premium linked to tensions in the Middle East.

- The normalization of tanker traffic through the Strait of Hormuz after the interim U.S.-Iran agreement reduced concerns over energy supply disruptions, limiting upward pressure on energy prices.

- Indonesian equities fell about 1.6% after MSCI delayed its review of reforms aimed at improving foreign investor access to the market. The decision revived debate over a potential downgrade of Indonesia from emerging-market to frontier-market status if liquidity and market-access issues are not resolved.

US100 and FedEx charts

Source: xStation5

Source: xStation5

Daily Summary: Nasdaq 100 Up 3.2% – Is the Bull Market Back? (04.08.2026)

US Open: S&P 500 at ATH, Strait of Hormuz nearing reopening, Palantir up 23%

Platinum gains 6% as precious metals rebound, US Dollar weakens

🚨 Brent crude falls below $80!

The content of this report has been created by XTB S.A., with its registered office in Warsaw, at Prosta 67, 00-838 Warsaw, Poland, (KRS number 0000217580) and supervised by Polish Supervision Authority ( No. DDM-M-4021-57-1/2005). This material is a marketing communication within the meaning of Art. 24 (3) of Directive 2014/65/EU of the European Parliament and of the Council of 15 May 2014 on markets in financial instruments and amending Directive 2002/92/EC and Directive 2011/61/EU (MiFID II). Marketing communication is not an investment recommendation or information recommending or suggesting an investment strategy within the meaning of Regulation (EU) No 596/2014 of the European Parliament and of the Council of 16 April 2014 on market abuse (market abuse regulation) and repealing Directive 2003/6/EC of the European Parliament and of the Council and Commission Directives 2003/124/EC, 2003/125/EC and 2004/72/EC and Commission Delegated Regulation (EU) 2016/958 of 9 March 2016 supplementing Regulation (EU) No 596/2014 of the European Parliament and of the Council with regard to regulatory technical standards for the technical arrangements for objective presentation of investment recommendations or other information recommending or suggesting an investment strategy and for disclosure of particular interests or indications of conflicts of interest or any other advice, including in the area of investment advisory, within the meaning of the Trading in Financial Instruments Act of 29 July 2005 (i.e. Journal of Laws 2019, item 875, as amended). The marketing communication is prepared with the highest diligence, objectivity, presents the facts known to the author on the date of preparation and is devoid of any evaluation elements. The marketing communication is prepared without considering the client’s needs, his individual financial situation and does not present any investment strategy in any way. The marketing communication does not constitute an offer of sale, offering, subscription, invitation to purchase, advertisement or promotion of any financial instruments. XTB S.A. is not liable for any client’s actions or omissions, in particular for the acquisition or disposal of financial instruments, undertaken on the basis of the information contained in this marketing communication. In the event that the marketing communication contains any information about any results regarding the financial instruments indicated therein, these do not constitute any guarantee or forecast regarding the future results.