🌍 Geopolitics – The Middle East remains in the spotlight

-

The conflict in the Middle East is escalating: over the weekend, the Houthis launched missile and drone attacks against Israel, while Israeli strikes caused temporary blackouts in Tehran and the surrounding area.

-

The United States continues to build up its forces in the region—several hundred special forces personnel (Rangers, SEALs), thousands of Marines, and the 82nd Airborne Division are already in the area, giving Trump the option of a ground operation.

-

Pakistan has announced that it will host direct talks between the U.S. and Iran in the coming days; Trump has signaled both progress in the negotiations and the possibility of seizing Iranian oil infrastructure, including Kharg Island.

-

Donald Trump said that negotiations with Iran are going well and that the Iranians have agreed to most of the 15 points proposed by the Americans.

-

Israel confirmed via Channel 12: In the event of a potential U.S. ground operation in Iran, the Israeli military will not participate on the ground.

🛢️ Oil and raw materials

-

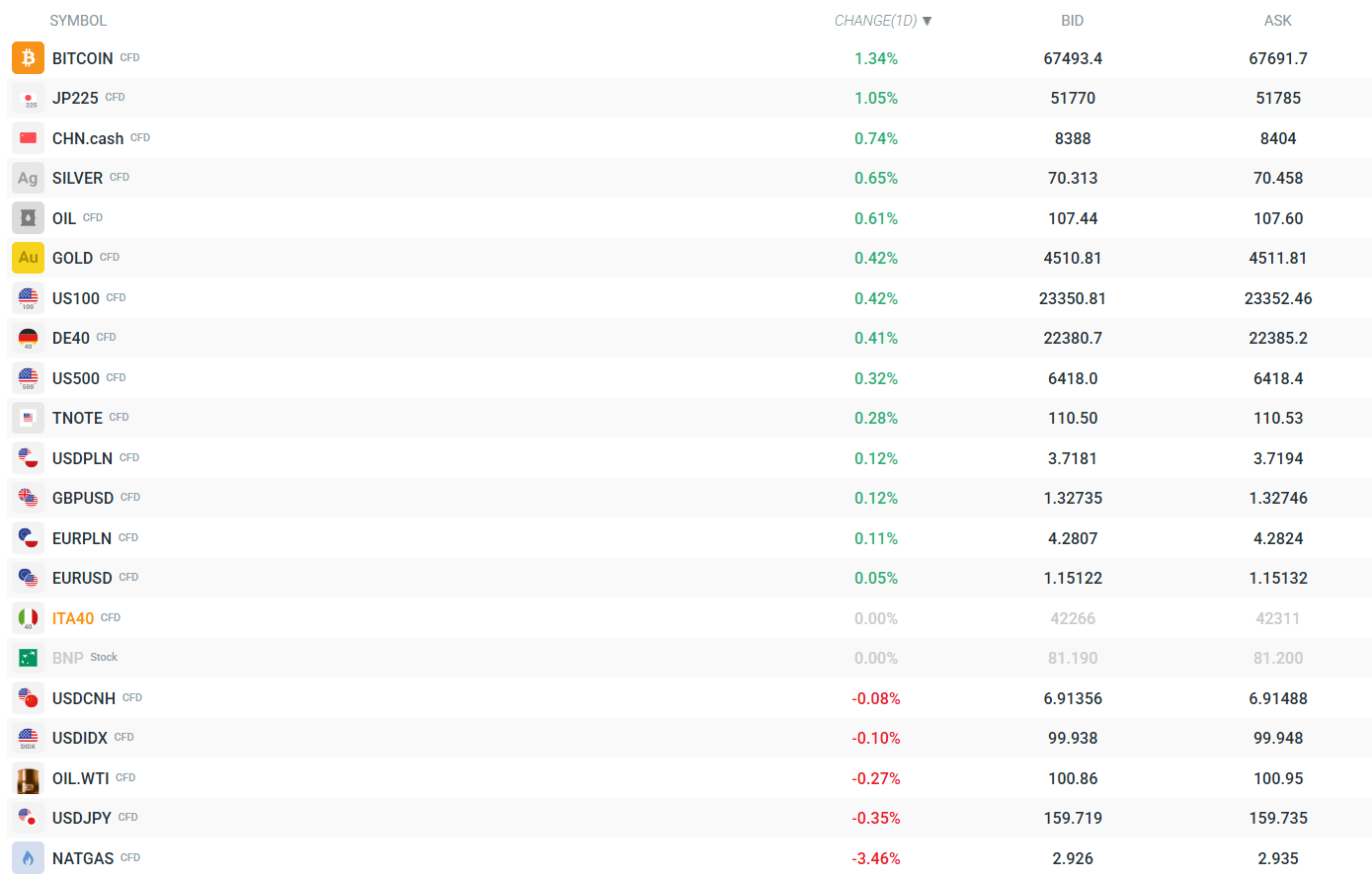

Brent crude opened the week significantly higher (~$107.7/bbl, +0.84%), but retreated after an initial rally, reflecting the uncertain ground built on both hopes for de-escalation and the real risk of a blockade of the Strait of Hormuz.

-

The market is closely monitoring tanker traffic—Trump noted that Iran has allowed 20 tankers to transit the Strait of Hormuz.

-

Gold continues its upward rally, trading at $4,514/oz (+0.49%), while silver is up 0.77% to $70.4/oz – demand for safe-haven and inflation-hedging assets remains strong amid the risk of war.

-

Natural gas (NATGAS) is down 3.23% to $2.93/MMBtu, while wheat on the CBOT is heading for its fourth gain in five sessions as higher energy and fertilizer costs weigh on the outlook for agricultural production.

🏛️ The Bank of Japan and the yen

-

The BoJ maintains its course of monetary tightening: The Summary of Opinions indicates a readiness for further rate hikes, although oil-driven inflation and the risk of stagflation are still cited as dampening factors.

-

Deputy Finance Minister Atsushi Mimura threatened "decisive action" against speculative moves in the yen—a clear escalation in interventionist rhetoric, backed by Governor Ueda’s remarks on the growing importance of the exchange rate for inflation.

-

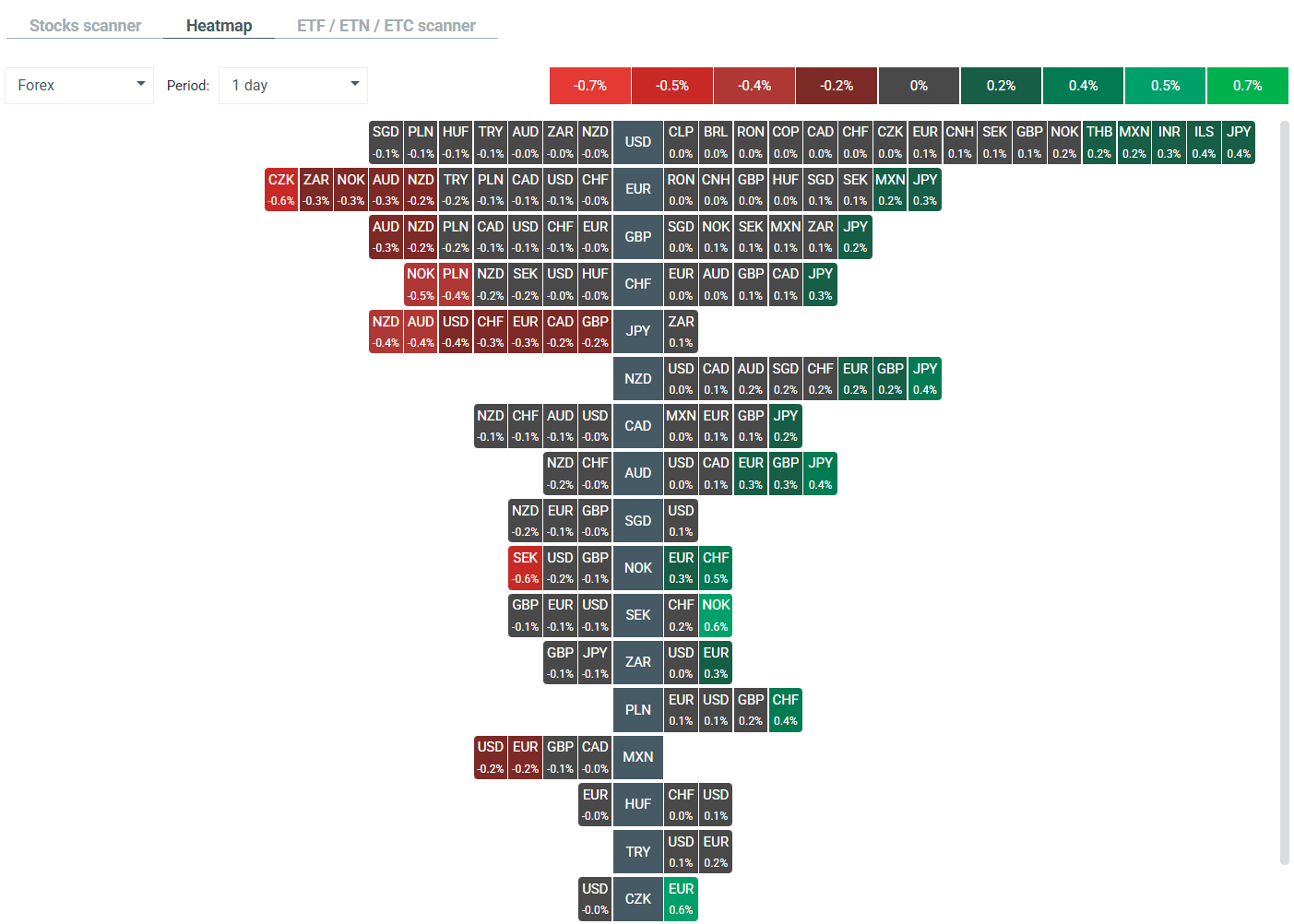

USD/JPY has slipped from around 160.50 to ~159.72 (-0.35%) – the yen is the strongest currency on the forex market today; the USDIDX dollar index has fallen below 100 points (-0.11%). The currencies of the Antipodes and the CAD are performing the weakest.

Heatmap of current volatility in the FX market. Source: xStation

📊 Asian markets and indices

-

The JP225 (Nikkei) is up +1.02% to ~51,757 points, recouping some of its earlier losses; regional markets are rebounding as the conflict did not escalate significantly over the weekend.

-

The CHN.cash (Chinese index) is up 0.90% to 8,401 points; the PBOC set today’s USD/CNY fixing at 6.9223—slightly above market expectations (6.9205)—causing the yuan to depreciate slightly.

-

European futures for the DAX (DE40) point to an opening near 22,380 points (+0.41%); the S&P 500 (US500) is up 0.33% to 6,419 points, and the Nasdaq (US100) is up 0.43% to 23,353 points.

Source: xStation

₿ Cryptocurrencies

-

Bitcoin stands out during the trading session: up 1.36% to ~$67,506 – the cryptocurrency is benefiting from both inflationary pressures and the broader "risk-on" market rally.

📅 In the spotlight this week

-

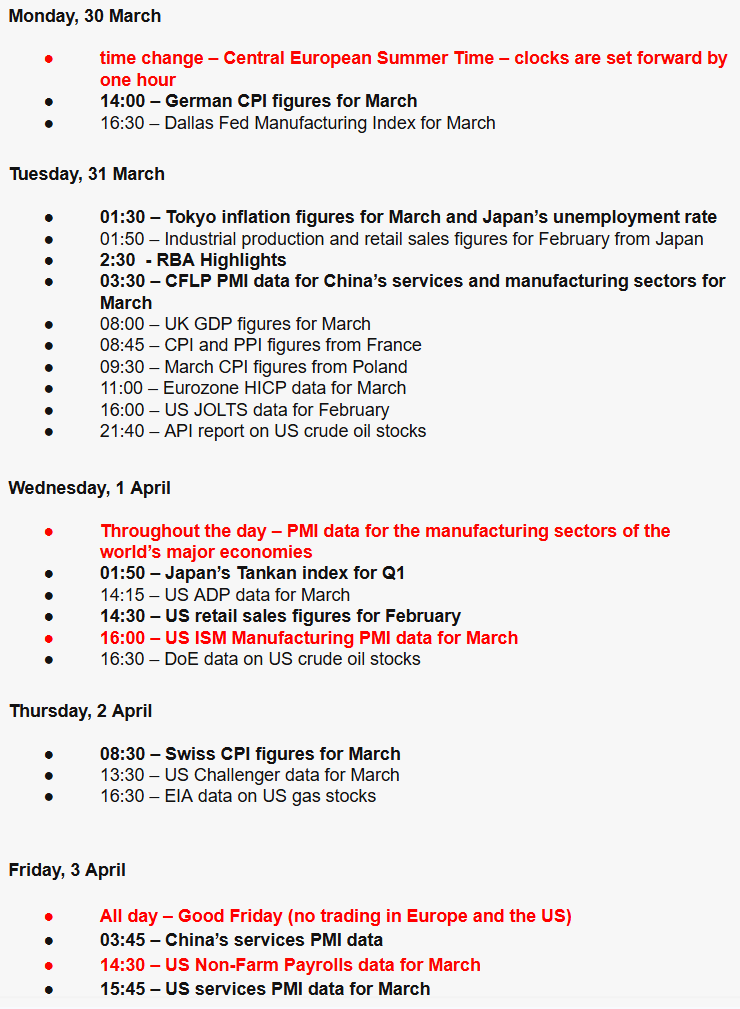

Friday: Key U.S. NFP report, along with ISM Manufacturing and Retail Sales data—these figures will determine the Fed’s path amid war-related uncertainty.

-

Eurozone: Preliminary CPI for March (Villeroy signals the ECB’s readiness to act, but says it is too early for specific decisions)

-

Australia: RBA Minutes – Following the government’s decision to cut the fuel tax, Morgan Stanley warns of a supply shock in the fuel market and upside risks.

-

BoJ Tankan (Q1 2026) – a key indicator of Japanese business sentiment following weeks of interventionist rhetoric.

Daily Summary: Wall Street Regains Ground; Another Intervention in the Yen Market❓

Three Markets to Watch Next Week (July 31, 2026)

Market Wrap: European equities at 3-week highs! Apple dips in US premarket!

Euro Area core inflation above estiamtes! EURUSD under key resistance!

The content of this report has been created by XTB S.A., with its registered office in Warsaw, at Prosta 67, 00-838 Warsaw, Poland, (KRS number 0000217580) and supervised by Polish Supervision Authority ( No. DDM-M-4021-57-1/2005). This material is a marketing communication within the meaning of Art. 24 (3) of Directive 2014/65/EU of the European Parliament and of the Council of 15 May 2014 on markets in financial instruments and amending Directive 2002/92/EC and Directive 2011/61/EU (MiFID II). Marketing communication is not an investment recommendation or information recommending or suggesting an investment strategy within the meaning of Regulation (EU) No 596/2014 of the European Parliament and of the Council of 16 April 2014 on market abuse (market abuse regulation) and repealing Directive 2003/6/EC of the European Parliament and of the Council and Commission Directives 2003/124/EC, 2003/125/EC and 2004/72/EC and Commission Delegated Regulation (EU) 2016/958 of 9 March 2016 supplementing Regulation (EU) No 596/2014 of the European Parliament and of the Council with regard to regulatory technical standards for the technical arrangements for objective presentation of investment recommendations or other information recommending or suggesting an investment strategy and for disclosure of particular interests or indications of conflicts of interest or any other advice, including in the area of investment advisory, within the meaning of the Trading in Financial Instruments Act of 29 July 2005 (i.e. Journal of Laws 2019, item 875, as amended). The marketing communication is prepared with the highest diligence, objectivity, presents the facts known to the author on the date of preparation and is devoid of any evaluation elements. The marketing communication is prepared without considering the client’s needs, his individual financial situation and does not present any investment strategy in any way. The marketing communication does not constitute an offer of sale, offering, subscription, invitation to purchase, advertisement or promotion of any financial instruments. XTB S.A. is not liable for any client’s actions or omissions, in particular for the acquisition or disposal of financial instruments, undertaken on the basis of the information contained in this marketing communication. In the event that the marketing communication contains any information about any results regarding the financial instruments indicated therein, these do not constitute any guarantee or forecast regarding the future results.