GEOPOLITICS AND THE MIDDLE EAST

• The stalemate in U.S.-Iran relations has now lasted nine weeks—the two sides have been unable to agree on a date for the second round of talks in Pakistan. Iran refuses to negotiate as long as the naval blockade remains in place, while Trump has stated that he “has all the time in the world” and does not intend to rush to resolve the conflict. As a reminder, Trump initially promised a resolution within “four to five weeks.”

• Trump announced a three-week extension of the ceasefire between Israel and Lebanon following a meeting at the White House with representatives from both sides. The president’s optimism was quickly dampened, however—Israel’s ambassador to the UN, Danny Danon, told CNN that the extension “is not 100 percent certain,” warning that Hezbollah is actively firing rockets at positions, undermining the truce.

• Trump ordered the U.S. Navy to “shoot and destroy any vessel” laying mines in the Strait of Hormuz, claiming at the same time that the U.S. now controls the strait. In reality, Iran continues to maintain tight control over this strategic waterway, and the situation remains tense.

• Trump has threatened the United Kingdom with “heavy tariffs” if London does not withdraw its Digital Services Tax, which targets American tech giants—Apple, Google, and Meta. This marks yet another flashpoint in transatlantic relations ahead of Trump’s planned state visit to the United Kingdom.

ECONOMY AND MACROECONOMIC DATA

• Japan’s core inflation (core CPI) stood at 1.8% year-over-year in March, in line with expectations but below the BOJ’s 2% target—for the second consecutive month. At the same time, the PPI for services surprised on the upside—3.1% versus an expected 3.0% and a previous reading of 2.7%—signaling persistent price pressures in the pipeline. The energy shock linked to the war with Iran is expected to push inflation back above the target in the coming months, keeping a June rate hike by the BOJ on the table.

• Japanese Finance Minister Katayama has stepped up his interventionist rhetoric regarding the yen, warning of "decisive action" against currency speculation, in close coordination with the U.S. The yen is hovering around the psychological level of 160 per dollar. The reference to coordination with Washington evokes the conditions that preceded the first joint U.S.-Japan currency intervention in 15 years.

• Trump warned Americans that higher gas prices would persist “for some time yet” due to the tightening of sanctions against Iran. This comment has real implications for inflation—energy costs spilling over into transportation, logistics, and consumer goods could add another layer of price pressure, complicating the Fed’s interest rate path.

• Lufthansa has canceled 20,000 flights due to rising jet fuel prices—a direct consequence of the oil market crisis stemming from the conflict in the Persian Gulf region. This is a sign that the energy crisis is beginning to have a real impact on the European transportation sector.

STOCK MARKETS – WALL STREET AND ASIA

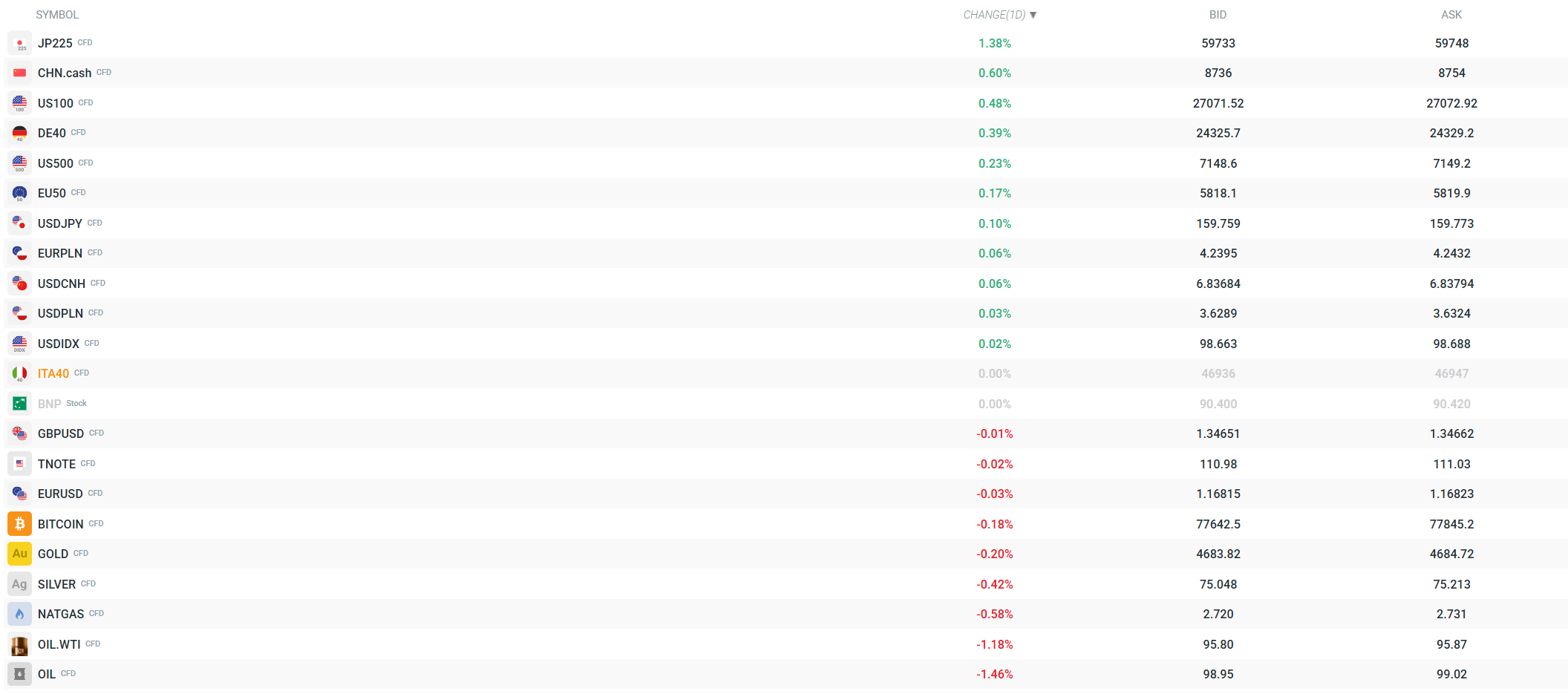

• Wall Street ended Thursday’s session in the red—the S&P 500 fell 0.4% and the Nasdaq Composite lost 0.9% (its worst day in nearly a month), even though both indices had earlier set new intraday highs during the session. For the week, the S&P 500 is down just 0.3%, and the Nasdaq 0.1% – surprisingly little given the 16–17% weekly jump in oil prices.

• U.S. index futures are mixed ahead of Friday’s session—S&P 500 futures are near flat, Nasdaq 100 futures are up about 0.4% (led by Intel), and Dow futures are down about 0.2%. The market remains in “narrow leadership” mode – Cameron Dawson of NewEdge Wealth notes that gains are driven almost exclusively by semiconductors, and the iShares Semiconductor ETF (SOXX) has recorded its 17th consecutive session of gains.

• Asian markets traded mixed on Friday. The Nikkei 225 gained 0.71% thanks to strength in the technology sector, while the Topix rose 0.30%. On the other hand, the Hang Seng lost 0.61%, the CSI 300 fell by 0.28%, the Kospi gave up 0.23%, and the Australian ASX 200 declined by 0.29%. The extension of the Israel-Lebanon ceasefire failed to reassure investors.

CURRENCIES

• The dollar strengthened slightly, trading within a narrow range. USDJPY remains around 159.8—close to the key 160 level, at which Japanese authorities have signaled their readiness to intervene. EURUSD is down slightly (-0.04%) at 1.168, while GBPUSD is virtually unchanged at 1.346.

• The zloty is losing ground slightly – USD/PLN is at 3.63 (+0.06%), EUR/PLN at 4.24 (+0.08%). In the broader currency market, commodity and emerging market currencies are showing weakness – the Norwegian krone, South African rand, and Mexican peso are losing ground against the dollar. The PBOC set the USD/CNY fixing at 6.8674, well above market estimates (6.8400), suggesting a continued controlled weakening of the yuan.

RAW MATERIALS

• Crude oil prices remain elevated amid the U.S.-Iran standoff and the ongoing blockade of the Strait of Hormuz. Brent has gained nearly 17% on a weekly basis, while WTI has risen by about 16%. On Friday morning, WTI is trading around $96 (-1.0% for the session), and Brent near $99 (-1.2%). A correction following a strong weekly rally, but the trend remains upward.

• Gold is giving back some of its gains—down 0.36% to around $4,677 per ounce. Silver is down 0.60%. Natural gas (NATGAS) is down 0.51%. Goldman Sachs estimates that oil production in the Persian Gulf could quickly recover after the opening of the Strait of Hormuz, but for now this remains a hypothetical scenario.

• The fuel crisis is hitting Asian refineries – the war with Iran is forcing refineries in Asia to cut back on processing, which threatens supplies of diesel and jet fuel in the region. This is precisely what led to Lufthansa’s decision to cancel 20,000 flights.

COMPANIES

• Intel – shares rose 19% following the release of Q1 results that significantly exceeded expectations (EPS of $0.29 vs. consensus of $0.01, revenue of $13.58 billion vs. $12.42 billion). The company also raised its forecast for Q2. This is the main driver of gains on the Nasdaq.

• SAP rose 5% in after-hours trading on the back of better-than-expected results (EPS of $1.72 vs. $1.69) and a 19% increase in cloud revenue. However, the company noted that its 2026 forecast assumes a de-escalation of the conflict in the Middle East.

• Nike announced the layoff of 1,400 employees—the second round of cuts this year.

• DeepSeek has released a preview version of its V4 model—the latest chapter in China’s AI race. The model is open-source and is designed to compete with the world’s top large language models (LLMs). Alibaba has announced the integration of its Qwen model into vehicles manufactured by BYD and Volkswagen (a local joint venture), reflecting the growing trend of AI in the automotive industry.

CRYPTOCURRENCIES

• Bitcoin is down 0.38%, trading around $77,500–$77,700. The crypto market is awaiting Saturday’s crypto summit at Mar-a-Lago, where Trump is set to deliver a speech—the event is open exclusively to the 297 largest holders of the $TRUMP memecoin. This could potentially trigger volatility in the memecoin segment over the weekend.

WHAT TO EXPECT FROM TODAY'S SESSION

• Before the U.S. markets open, Procter & Gamble, Norfolk Southern, Charter Communications, and SLB will release their quarterly reports—SLB’s results (oil sector) in particular may provide insights into the impact of the energy crisis on the industry.

• At 4:00 p.m. CET, the final reading of the University of Michigan Consumer Sentiment Index for April will be released—against the backdrop of Trump’s warnings about higher gas prices, the reading may confirm a deterioration in U.S. household sentiment.

• Markets will remain sensitive to news from the Middle East—the weekend is shaping up to be turbulent due to Israel’s heightened readiness for a potential escalation. Narrow market leadership (dominated by semiconductors) and the disconnect between investor optimism and geopolitical realities create a fragile environment in which any negative headline could trigger a sharp correction.

Current market volatility. Source: xStation

Platinum gains 6% as precious metals rebound, US Dollar weakens

🚨 Brent crude falls below $80!

Nasdaq Gains 0.6% and Reclaims 29,000 🔼 Strong Results from ON Semiconductor and Palantir

Cocoa Pauses Its Sharp Rally 🚩 Production Concerns in West Africa Return

The content of this report has been created by XTB S.A., with its registered office in Warsaw, at Prosta 67, 00-838 Warsaw, Poland, (KRS number 0000217580) and supervised by Polish Supervision Authority ( No. DDM-M-4021-57-1/2005). This material is a marketing communication within the meaning of Art. 24 (3) of Directive 2014/65/EU of the European Parliament and of the Council of 15 May 2014 on markets in financial instruments and amending Directive 2002/92/EC and Directive 2011/61/EU (MiFID II). Marketing communication is not an investment recommendation or information recommending or suggesting an investment strategy within the meaning of Regulation (EU) No 596/2014 of the European Parliament and of the Council of 16 April 2014 on market abuse (market abuse regulation) and repealing Directive 2003/6/EC of the European Parliament and of the Council and Commission Directives 2003/124/EC, 2003/125/EC and 2004/72/EC and Commission Delegated Regulation (EU) 2016/958 of 9 March 2016 supplementing Regulation (EU) No 596/2014 of the European Parliament and of the Council with regard to regulatory technical standards for the technical arrangements for objective presentation of investment recommendations or other information recommending or suggesting an investment strategy and for disclosure of particular interests or indications of conflicts of interest or any other advice, including in the area of investment advisory, within the meaning of the Trading in Financial Instruments Act of 29 July 2005 (i.e. Journal of Laws 2019, item 875, as amended). The marketing communication is prepared with the highest diligence, objectivity, presents the facts known to the author on the date of preparation and is devoid of any evaluation elements. The marketing communication is prepared without considering the client’s needs, his individual financial situation and does not present any investment strategy in any way. The marketing communication does not constitute an offer of sale, offering, subscription, invitation to purchase, advertisement or promotion of any financial instruments. XTB S.A. is not liable for any client’s actions or omissions, in particular for the acquisition or disposal of financial instruments, undertaken on the basis of the information contained in this marketing communication. In the event that the marketing communication contains any information about any results regarding the financial instruments indicated therein, these do not constitute any guarantee or forecast regarding the future results.