- U.S. equity futures edge higher despite rising oil prices.

- The conflict between the United States and Iran is escalating once again.

- China's June CPI inflation came in slightly below market expectations.

- U.S. equity futures edge higher despite rising oil prices.

- The conflict between the United States and Iran is escalating once again.

- China's June CPI inflation came in slightly below market expectations.

- Asian equities surrendered most of their earlier gains and are now up just 0.1%, as the rally in semiconductor stocks lost momentum. Despite this, U.S. equity futures are moving higher, with the US100 up 0.6% and the US500 gaining 0.3%, while European index futures point to a stronger open.

- Brent crude is up more than 1% to around USD 79 per barrel, marking its third consecutive daily gain following another wave of U.S. strikes on Iran. Government bonds continue to decline across Japan, Australia and New Zealand as markets increasingly price in further Fed rate hikes in response to rising inflation risks.

- The yield on the U.S. 2-year Treasury approached its highest level of the year on Wednesday, although Treasuries traded broadly stable during the Asian session. Meanwhile, the U.S. dollar index is edging lower, while Bitcoin has rebounded to USD 62,500.

- Gold is falling for a fourth consecutive session to around USD 4,050 per ounce, while silver is down nearly 1%, slipping below USD 58 per ounce, as higher interest rate expectations continue to reduce the appeal of non-yielding assets.

- Shipping through the Strait of Hormuz has slowed to a near standstill following a second consecutive day of U.S. strikes on Iran. This has reinforced concerns over disruptions to one of the world's most important energy shipping routes, although equity markets are not yet pricing in the risk of prolonged supply disruptions. The U.S. has also revoked a waiver that allowed Tehran to sell oil globally following attacks on tankers in the Strait of Hormuz.

- China's June CPI rose 1.0% YoY, below the 1.1% consensus and down from 1.2% in May. Meanwhile, PPI accelerated to 4.1% YoY, in line with expectations and up from 3.9% a month earlier. Hong Kong's Hang Seng Index fell more than 1%.

- Nearly 400 S&P 500 companies closed lower yesterday, although the benchmark recovered part of its losses after Donald Trump suggested he does not expect the war to resume.

- The semiconductor sector outperformed after reports that China may allow its leading AI companies to purchase a limited number of Nvidia H200 processors.

- Apple is expanding its partnership with Broadcom, with the value of the agreement for U.S.-made components expected to exceed USD 30 billion. Meanwhile, Meta plans to invest approximately USD 10 billion in its first data center in Canada, further expanding its AI infrastructure.

- Iranian state television reported eight explosions near the city of Bandar Abbas. According to the reports, two projectiles struck Sirik Port, while another two detonated at Jask Port. There were also reports of a bridge being destroyed in northeastern Iran, although these claims have not been independently verified. Tehran warned of potential attacks on U.S. bases across the Middle East, while U.S. officials indicated that the next wave of strikes on Iran could be even more intense.

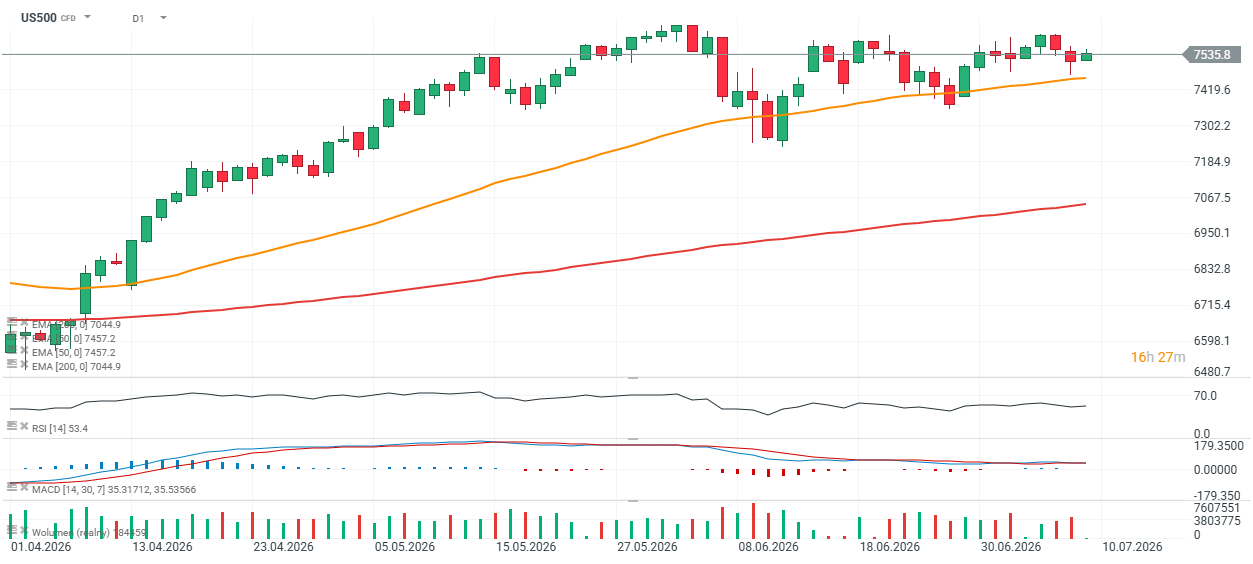

US 500 (D1 chart)

S&P 500 futures have once again rebounded from the 50-day exponential moving average (EMA50, orange line), which provided support during yesterday's session. During the two stronger corrective moves in June, the benchmark briefly traded below this level before recovering. The key support remains around 7,460 points, while the nearest resistance is defined by the recent local highs near 7,650 points.

Source: xStation 5

Euro Area core inflation above estiamtes! EURUSD under key resistance!

Economic Calendar: Key European CPI Readings and Oil Giants’ Earnings

Morning Wrap: AI Fuels the Rebound. Technology Makes a Strong Comeback

Daily Summary: Equities rally on not-so-hawkish Fed and AI trade revival, Yen dominates FX, oil retreats (30.07.2026)

The content of this report has been created by XTB S.A., with its registered office in Warsaw, at Prosta 67, 00-838 Warsaw, Poland, (KRS number 0000217580) and supervised by Polish Supervision Authority ( No. DDM-M-4021-57-1/2005). This material is a marketing communication within the meaning of Art. 24 (3) of Directive 2014/65/EU of the European Parliament and of the Council of 15 May 2014 on markets in financial instruments and amending Directive 2002/92/EC and Directive 2011/61/EU (MiFID II). Marketing communication is not an investment recommendation or information recommending or suggesting an investment strategy within the meaning of Regulation (EU) No 596/2014 of the European Parliament and of the Council of 16 April 2014 on market abuse (market abuse regulation) and repealing Directive 2003/6/EC of the European Parliament and of the Council and Commission Directives 2003/124/EC, 2003/125/EC and 2004/72/EC and Commission Delegated Regulation (EU) 2016/958 of 9 March 2016 supplementing Regulation (EU) No 596/2014 of the European Parliament and of the Council with regard to regulatory technical standards for the technical arrangements for objective presentation of investment recommendations or other information recommending or suggesting an investment strategy and for disclosure of particular interests or indications of conflicts of interest or any other advice, including in the area of investment advisory, within the meaning of the Trading in Financial Instruments Act of 29 July 2005 (i.e. Journal of Laws 2019, item 875, as amended). The marketing communication is prepared with the highest diligence, objectivity, presents the facts known to the author on the date of preparation and is devoid of any evaluation elements. The marketing communication is prepared without considering the client’s needs, his individual financial situation and does not present any investment strategy in any way. The marketing communication does not constitute an offer of sale, offering, subscription, invitation to purchase, advertisement or promotion of any financial instruments. XTB S.A. is not liable for any client’s actions or omissions, in particular for the acquisition or disposal of financial instruments, undertaken on the basis of the information contained in this marketing communication. In the event that the marketing communication contains any information about any results regarding the financial instruments indicated therein, these do not constitute any guarantee or forecast regarding the future results.