Forecasts point to an exceptionally strong El Niño in 2026, with sea surface temperatures potentially rising by as much as ~2.5°C, placing this episode on par with—or even exceeding—historic events such as 1997–98 and 2015–16. Such a scenario implies significant shifts in global weather patterns, including milder winter conditions and reduced summer temperature volatility in the United States. From a natural gas market perspective, the key implication is higher storage levels and weaker energy demand during the spring–summer period. As a result, the market environment becomes fundamentally bearish for US gas prices, especially given already subdued seasonal demand (limited heating and softer cooling demand).

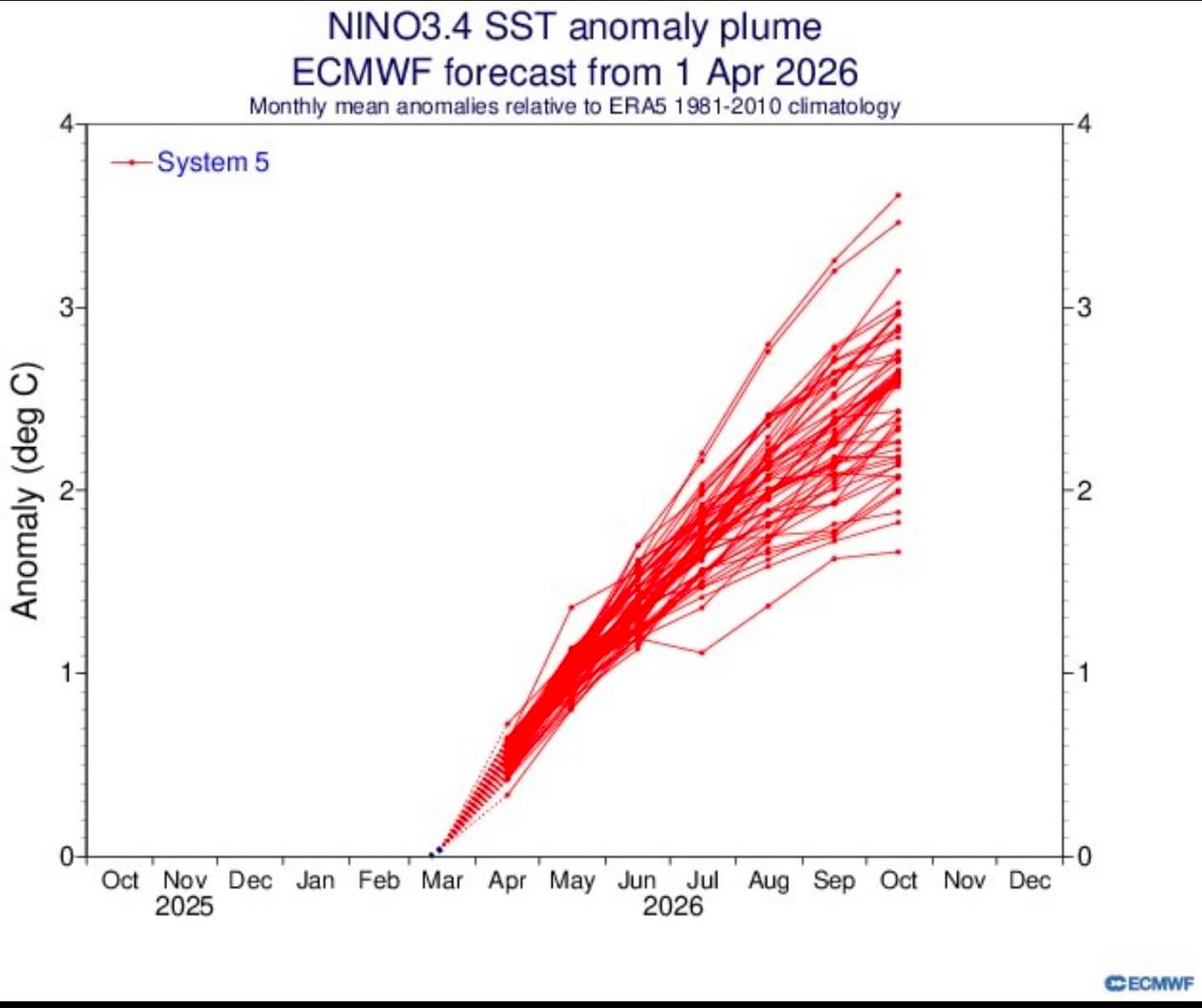

- Models are nearly unanimous in projecting strong warming in the Niño 3.4 region by autumn 2026, increasing confidence in a very strong El Niño scenario.

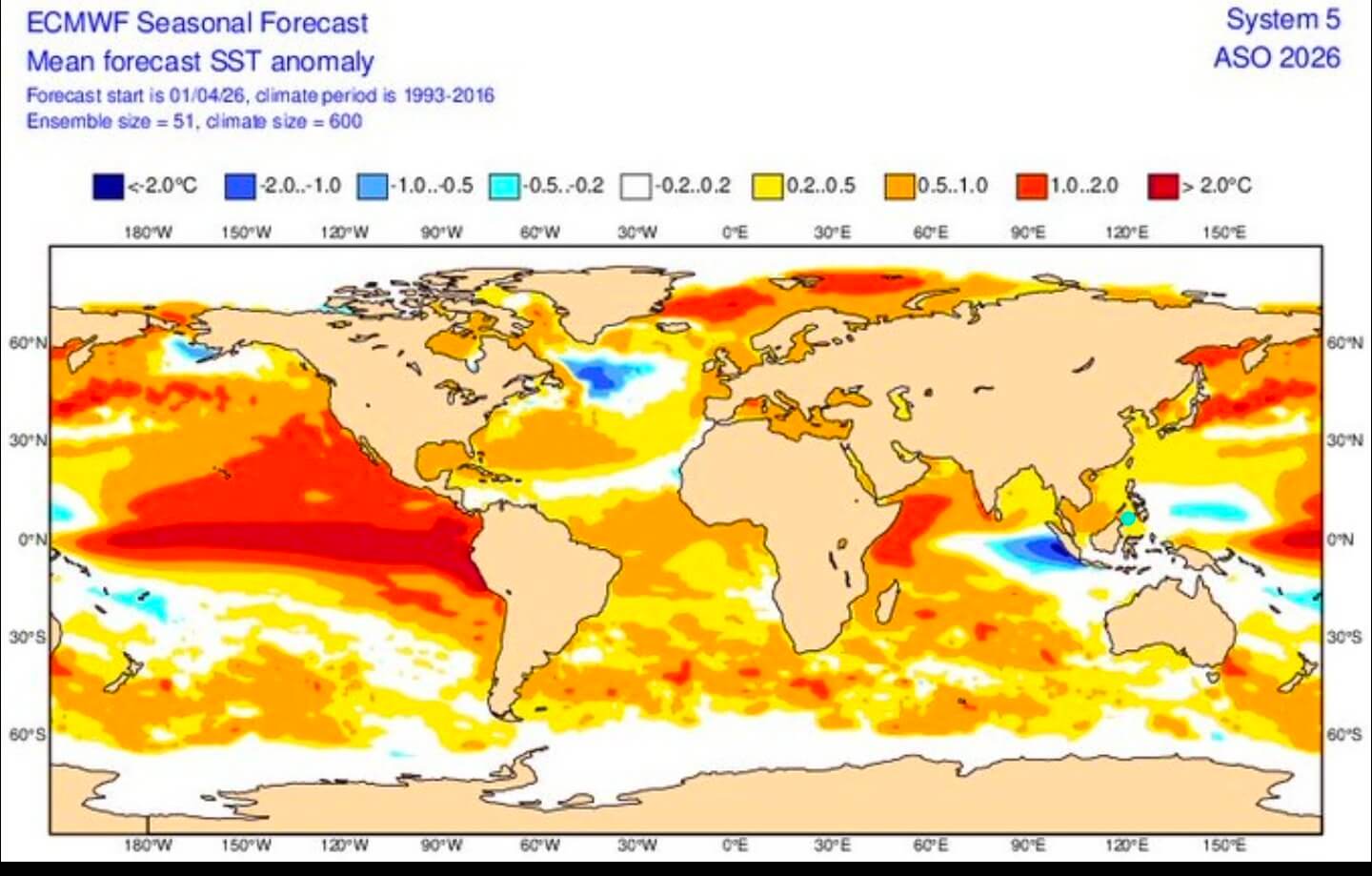

- Sea surface temperature anomalies exceeding +2.0°C across the equatorial Pacific point to a broad and persistent disruption in atmospheric circulation.

- In practice, this translates into a warmer winter in North America, leading to weaker heating demand and higher end-of-season gas storage levels.

- Entering spring with elevated inventories places the gas market in an oversupplied phase, which historically translates into price weakness during the shoulder season.

- During summer months, El Niño tends to limit the frequency and intensity of extreme heat in parts of the US, reducing electricity demand and gas burn in power generation.

- At the same time, it suppresses Atlantic hurricane activity, lowering the risk of supply disruptions in the Gulf of Mexico.

- This reduces the weather risk premium that typically supports gas prices during the summer season.

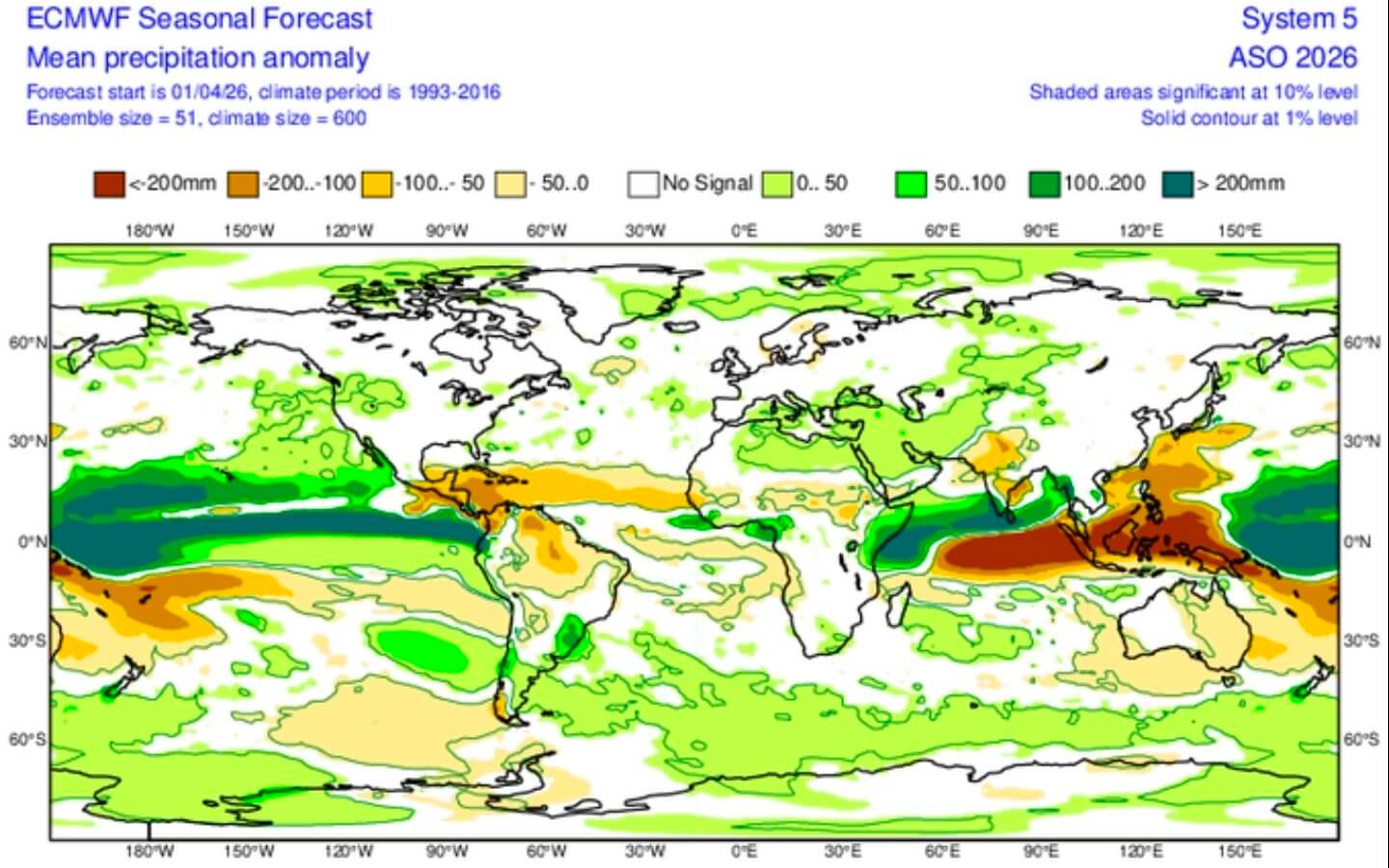

- Strong precipitation anomalies—drought in Indonesia and northern Australia alongside excessive rainfall in the equatorial Pacific—confirm the scale and global reach of the climatic disruption.

- From a valuation standpoint, the pace of storage injections in spring and their deviation from the five-year average remain critical variables.

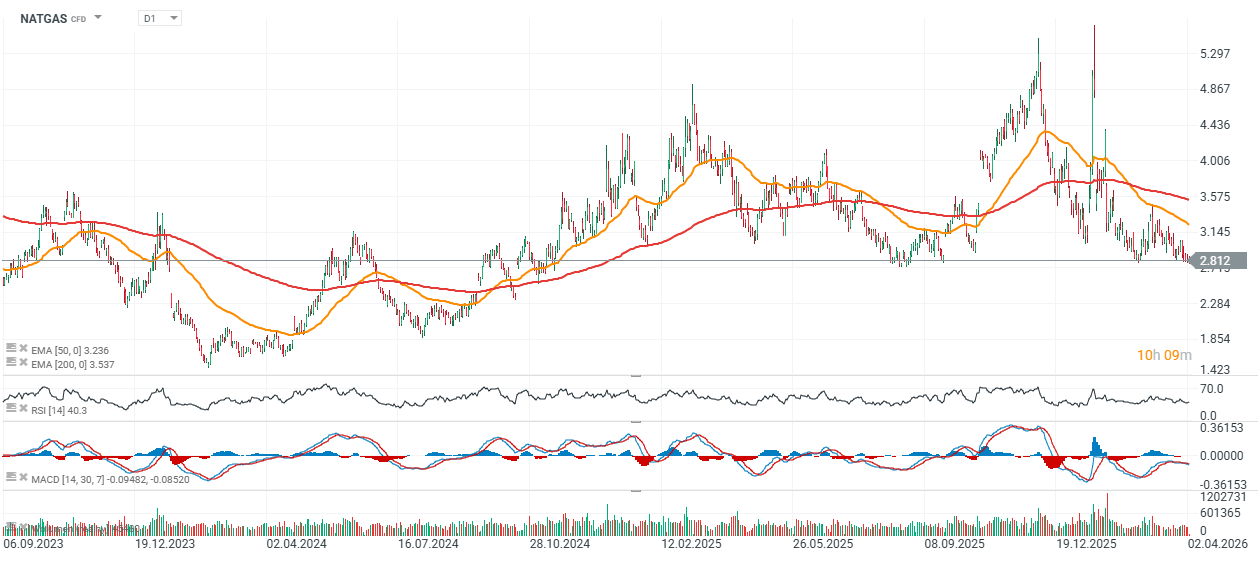

- In summary, a strong—potentially the strongest in over 140 years—El Niño scenario creates a setup in which US gas prices face limited upside, with the market balance shifting toward oversupply unless offset by strong external demand.

Source: xStation5

Source: ECMWF

Source: ECMWF

Source: ECMWF

When will the rise in oil prices reach us?

Daily Summary: Equities Diverge as Tech Lags, Europe Rallies on Earnings & PMIs (24.07.2026)

Three markets to watch next week (24.07.2026)

Oil Slides Ahead of the Weekend!

The content of this report has been created by XTB S.A., with its registered office in Warsaw, at Prosta 67, 00-838 Warsaw, Poland, (KRS number 0000217580) and supervised by Polish Supervision Authority ( No. DDM-M-4021-57-1/2005). This material is a marketing communication within the meaning of Art. 24 (3) of Directive 2014/65/EU of the European Parliament and of the Council of 15 May 2014 on markets in financial instruments and amending Directive 2002/92/EC and Directive 2011/61/EU (MiFID II). Marketing communication is not an investment recommendation or information recommending or suggesting an investment strategy within the meaning of Regulation (EU) No 596/2014 of the European Parliament and of the Council of 16 April 2014 on market abuse (market abuse regulation) and repealing Directive 2003/6/EC of the European Parliament and of the Council and Commission Directives 2003/124/EC, 2003/125/EC and 2004/72/EC and Commission Delegated Regulation (EU) 2016/958 of 9 March 2016 supplementing Regulation (EU) No 596/2014 of the European Parliament and of the Council with regard to regulatory technical standards for the technical arrangements for objective presentation of investment recommendations or other information recommending or suggesting an investment strategy and for disclosure of particular interests or indications of conflicts of interest or any other advice, including in the area of investment advisory, within the meaning of the Trading in Financial Instruments Act of 29 July 2005 (i.e. Journal of Laws 2019, item 875, as amended). The marketing communication is prepared with the highest diligence, objectivity, presents the facts known to the author on the date of preparation and is devoid of any evaluation elements. The marketing communication is prepared without considering the client’s needs, his individual financial situation and does not present any investment strategy in any way. The marketing communication does not constitute an offer of sale, offering, subscription, invitation to purchase, advertisement or promotion of any financial instruments. XTB S.A. is not liable for any client’s actions or omissions, in particular for the acquisition or disposal of financial instruments, undertaken on the basis of the information contained in this marketing communication. In the event that the marketing communication contains any information about any results regarding the financial instruments indicated therein, these do not constitute any guarantee or forecast regarding the future results.