Shares of European defense companies started the week with clear gains after remarks by NATO Secretary General Mark Rutte, who noted that weapons manufacturers are increasingly struggling to keep up with the surge in orders.

For the market, this was another signal and confirmation that the biggest challenge for European industry is not demand, but the industry’s ability to deliver equipment on time.

Italy’s Fincantieri stood out the most, with its shares rising by more than ten percent.

Gains were also recorded by, among others, Leonardo, Saab, Hensoldt, Rheinmetall, Thales, Indra, Dassault Aviation, and Safran, up in the 2 to 5 percent range.

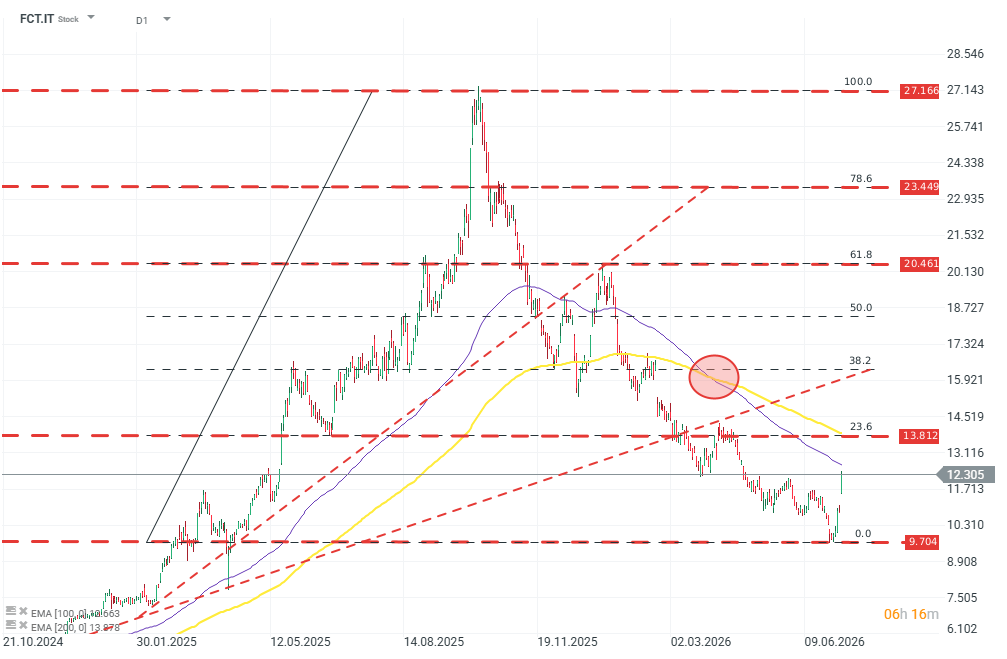

Technical analysis of Fincantieri (FCT.IT) (D1)

The Italian manufacturer of systems intended for naval warfare has lost more than 60 percent of its valuation from the peak at the end of 2025. Today’s gains are impressive and very much needed on the demand side if it wants to regain the initiative, but they may not be enough to change the longer term trend. The company’s valuation is weighed down by a “death cross” from March 2026. Investors should track the price in relation to Fibonacci levels. Only a move above the 38.2 percent Fibonacci level can be treated as a meaningful signal that offers hope for a return to an uptrend. Source: xStaion5

Investors’ reaction shows that the market is increasingly pricing in not only higher defense budgets, but also a potential improvement in margins and in the negotiating power of manufacturers operating at maximum capacity utilization.

Rutte pointed out that NATO is only now moving from the stage of political declarations to the stage of executing orders. According to NATO data, European allies (and Canada) increased defense spending by 20 percent versus 2024, to more than USD 574 billion. At the same time, under the new target, allies are to reach 5 percent of GDP for defense and security related spending by 2035.

Rutte also noted that constraints concern both industrial capacity and the ability to recruit and train military personnel. According to his remarks, around USD 300 billion in orders has already gone to U.S. arms manufacturers, which further illustrates the scale of demand generated by NATO countries.

From the perspective of European defense companies, this is an ambiguous but market positive signal. On the one hand, limited production capacity means the risk of delays, pressure on supply chains, and the need to incur high capital expenditures.

On the other hand, if demand is structural and long term, manufacturers can count on longer order backlogs, improved revenue quality, and potentially better contract terms.

An additional catalyst is the upcoming NATO summit in Ankara, scheduled for July 7 to 8. The meeting is set to focus on defense spending, transfer and logistics capabilities, and further support for Ukraine. A particularly promising area for additional spending may be drones and counter drone systems.

From a sector sentiment perspective, it is absolutely crucial that these gains are being seen in the context of Donald Trump’s comments that “Putin feels pressure” and that “the end of the war is closer than everyone thinks.” In the past, such declarations would have put significant pressure on defense company valuations. Today, however, the market sees more opportunities than risks for the sector’s valuations, which is important after several months of deep declines from the peaks.

🔴European TTF gas prices fall by 7.5%

Economic Calendar: What you need to watch closely this week❓ (27.07.2026)

Morning Wrap: The weekend slump in oil prices is accelerating 💥 (27.07.2026)

When will the rise in oil prices reach us?

The content of this report has been created by XTB S.A., with its registered office in Warsaw, at Prosta 67, 00-838 Warsaw, Poland, (KRS number 0000217580) and supervised by Polish Supervision Authority ( No. DDM-M-4021-57-1/2005). This material is a marketing communication within the meaning of Art. 24 (3) of Directive 2014/65/EU of the European Parliament and of the Council of 15 May 2014 on markets in financial instruments and amending Directive 2002/92/EC and Directive 2011/61/EU (MiFID II). Marketing communication is not an investment recommendation or information recommending or suggesting an investment strategy within the meaning of Regulation (EU) No 596/2014 of the European Parliament and of the Council of 16 April 2014 on market abuse (market abuse regulation) and repealing Directive 2003/6/EC of the European Parliament and of the Council and Commission Directives 2003/124/EC, 2003/125/EC and 2004/72/EC and Commission Delegated Regulation (EU) 2016/958 of 9 March 2016 supplementing Regulation (EU) No 596/2014 of the European Parliament and of the Council with regard to regulatory technical standards for the technical arrangements for objective presentation of investment recommendations or other information recommending or suggesting an investment strategy and for disclosure of particular interests or indications of conflicts of interest or any other advice, including in the area of investment advisory, within the meaning of the Trading in Financial Instruments Act of 29 July 2005 (i.e. Journal of Laws 2019, item 875, as amended). The marketing communication is prepared with the highest diligence, objectivity, presents the facts known to the author on the date of preparation and is devoid of any evaluation elements. The marketing communication is prepared without considering the client’s needs, his individual financial situation and does not present any investment strategy in any way. The marketing communication does not constitute an offer of sale, offering, subscription, invitation to purchase, advertisement or promotion of any financial instruments. XTB S.A. is not liable for any client’s actions or omissions, in particular for the acquisition or disposal of financial instruments, undertaken on the basis of the information contained in this marketing communication. In the event that the marketing communication contains any information about any results regarding the financial instruments indicated therein, these do not constitute any guarantee or forecast regarding the future results.