The introduction of new instruments based on commodity futures allows investors to trade much more precisely in terms of geographical and quality trading. Here is what is happening in these markets and how they compare to classic benchmarks:

NATGAS.EU (TTF Natural Gas)

- What is happening fundamentally: The European gas market (Dutch exchange) is facing a return of elevated volatility, with prices in June 2026 exceeding the 50 EUR/MWh barrier at the beginning of the month and then falling back to around 40 EUR/MWh, the lowest levels since April. The main driver of the move is uncertainty around global LNG supplies (still feeling the effects of recent logistical tensions in the Middle East) and high demand generated by summer heatwaves in Europe (gas-fired power plants are working at full capacity for air conditioning needs). This makes it difficult for Europe to refill storage stress-free before the next winter.

- Difference from the benchmark (US Henry Hub / NATGAS): Henry Hub reflects the situation in the USA, where there is a structural oversupply of shale gas and export infrastructure constraints (gas in the USA is cheap and cut off from the rest of the world). NATGAS.EU (TTF) is, in turn, an instrument extremely sensitive to global geopolitics. Europe must compete on price for every LNG delivery with Asia, making TTF prices many times higher than in the USA, and a failure of one Norwegian pipe or a terminal outage in Qatar immediately triggers massive price rallies in Europe.

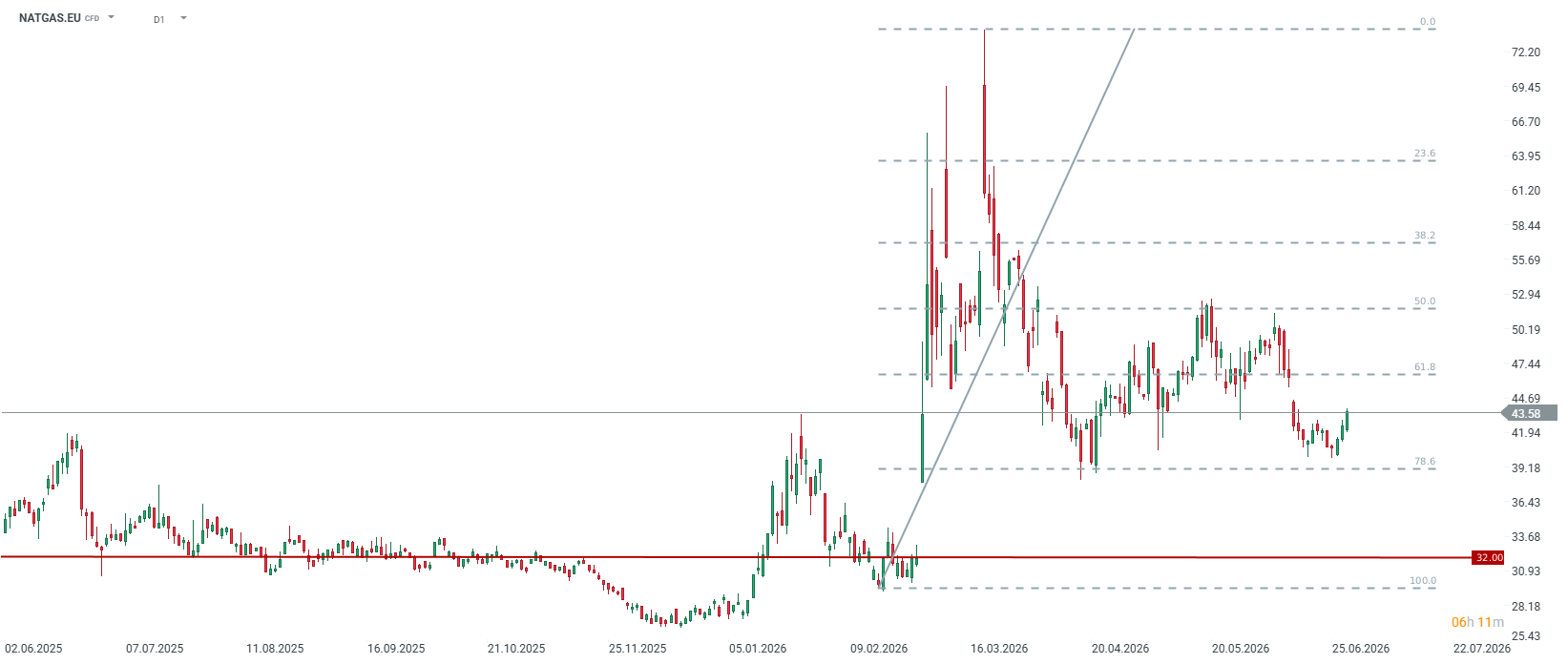

Prices are returning to growth after testing 40 EUR/MWh. Source: xStation5

Prices are returning to growth after testing 40 EUR/MWh. Source: xStation5

COFFEE.EU (Robusta Coffee)

- What is happening fundamentally: Robusta prices on the London exchange have recently seen a technical cooling (the July contract fell to around 3,500 USD per ton) as expectations of larger harvests from Indonesia and Brazil slowly enter the market. Earlier, however, Robusta was becoming more expensive at an extreme pace due to devastating droughts in Vietnam (the world's largest Robusta producer) caused by the whims of El Niño. The supply of this species is still considered very tight. El Niño has a huge impact on harvests in Asia, so this coffee may be exposed to significant changes if El Niño actually occurs at the end of this year. Robusta remains in fairly clear backwardation, especially on the nearest calendar spread.

- Difference from the main benchmark (Arabica / COFFEE): Classic Arabica (traded in New York) is a premium segment coffee, grown at higher altitudes, mainly in Latin America, characterized by a milder taste. Robusta (traded in London) is easier to grow, contains much more caffeine and is a key raw material for the production of instant coffees and espresso blends. Due to the climate crisis in Asia, the traditional price discount of Robusta relative to Arabica has drastically decreased. By trading COFFEE.EU, investors are playing for a completely different demand structure and weather factors prevailing in Vietnam, not Brazil.

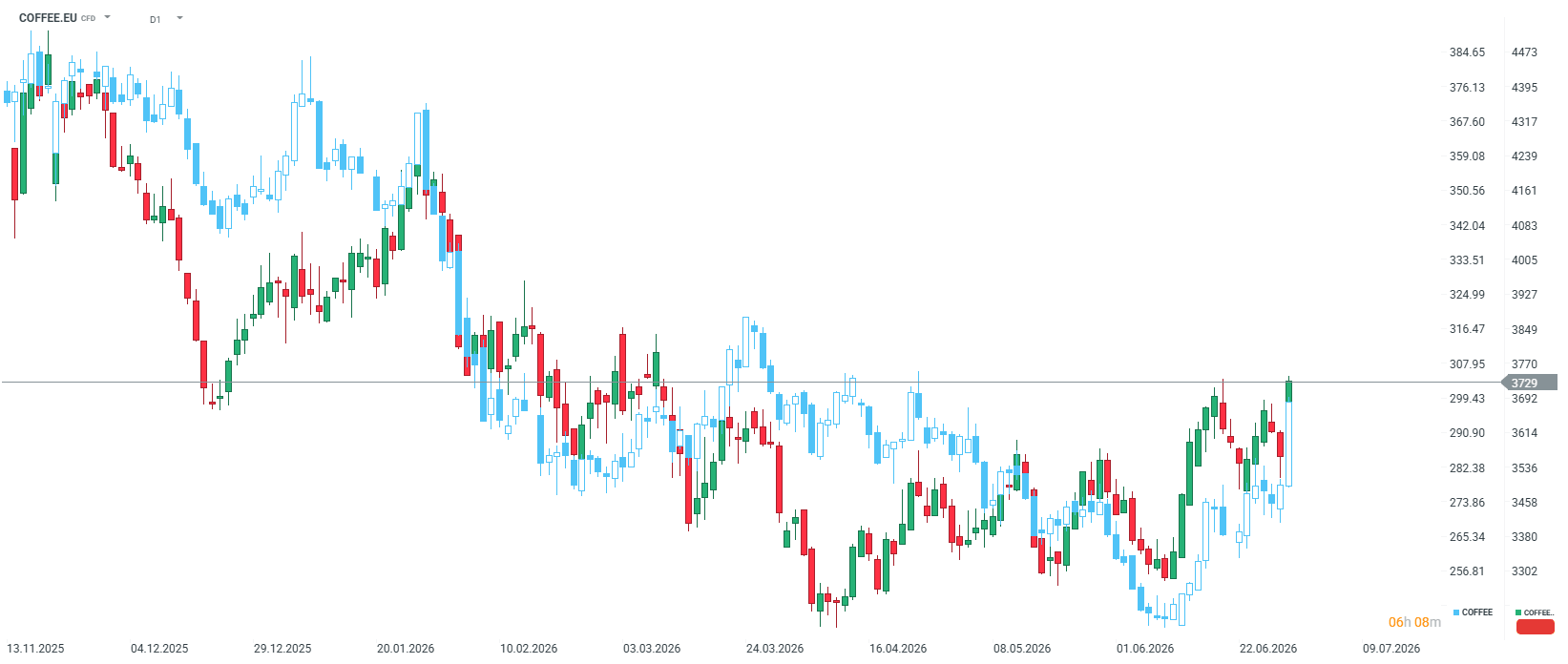

Despite different fundamentals, the correlation between Robusta and Arabica is quite high. It is worth remembering that although Vietnam is the 1st producer of Robusta in the world and Indonesia is 3rd, Brazil is in second place. Source: xStation5

Despite different fundamentals, the correlation between Robusta and Arabica is quite high. It is worth remembering that although Vietnam is the 1st producer of Robusta in the world and Indonesia is 3rd, Brazil is in second place. Source: xStation5

COCOA.EU (London Cocoa)

- What is happening fundamentally: The cocoa market in the UK (quoted in British pounds) is moving in a strong upward trend, testing multi-month highs (nearly 4,000 GBP per ton). Although current exports from Nigeria and Ivory Coast show increases, investors in London are intensively pricing in dismal prospects for the main harvests from West Africa for the 2026/2027 season due to weather anomalies, heavy rains hindering transport to ports, and cocoa tree diseases.

- Difference from the main benchmark (NY Cocoa / COCOA): The key cocoa benchmark is traded on the New York exchange in US dollars (USD). The new COCOA.EU instrument is a contract from the ICE Europe exchange in London, quoted in pounds (GBP). This means that the GBP/USD exchange rate directly affects the valuation of this instrument and creates room for arbitrage transactions. Additionally, the London contract specifies physical delivery of the commodity to European ports (e.g., Rotterdam, Antwerp). As a result, COCOA.EU reacts much more strongly to local EU customs and environmental regulations (e.g., restrictive EU anti-deforestation regulations – EUDR) and to the level of inventory in Europe itself.

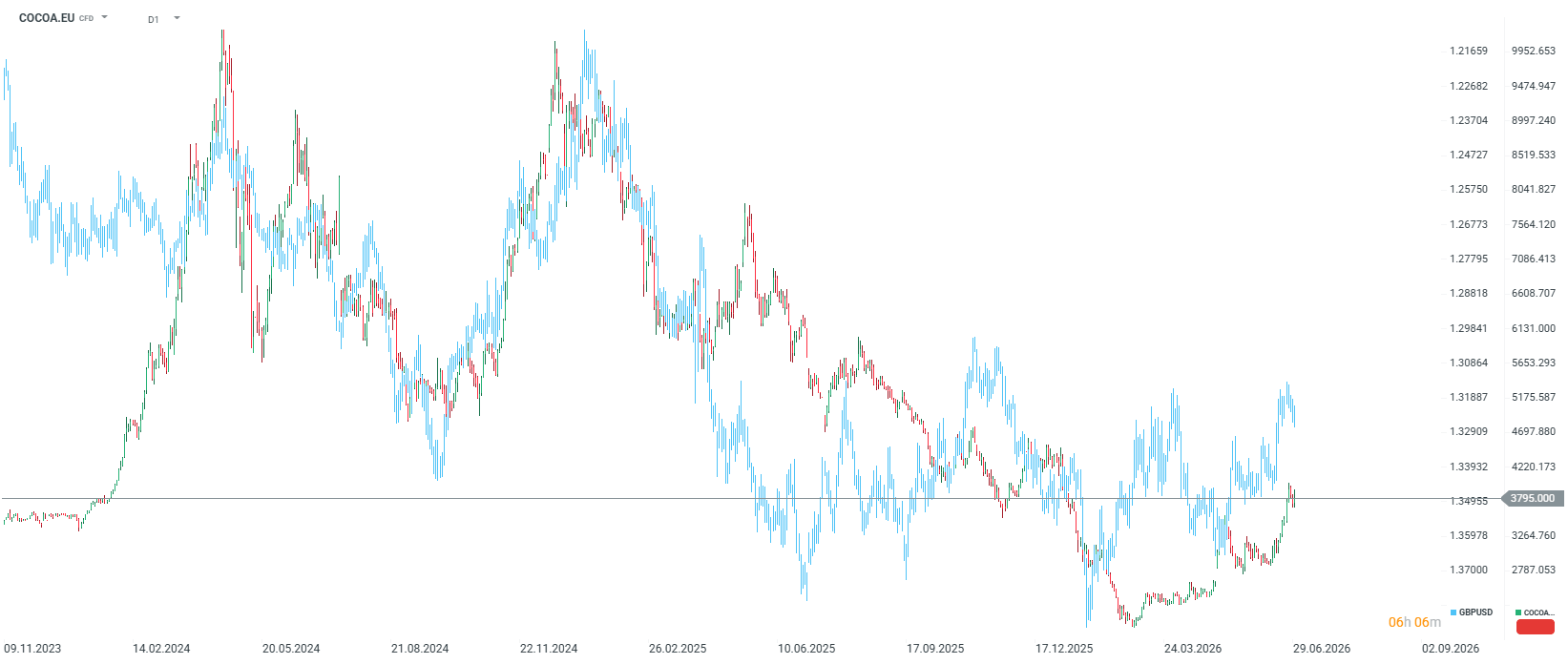

Historically, we have observed significant influence of the pound on cocoa quotations in London. Source: xStation5

Historically, we have observed significant influence of the pound on cocoa quotations in London. Source: xStation5

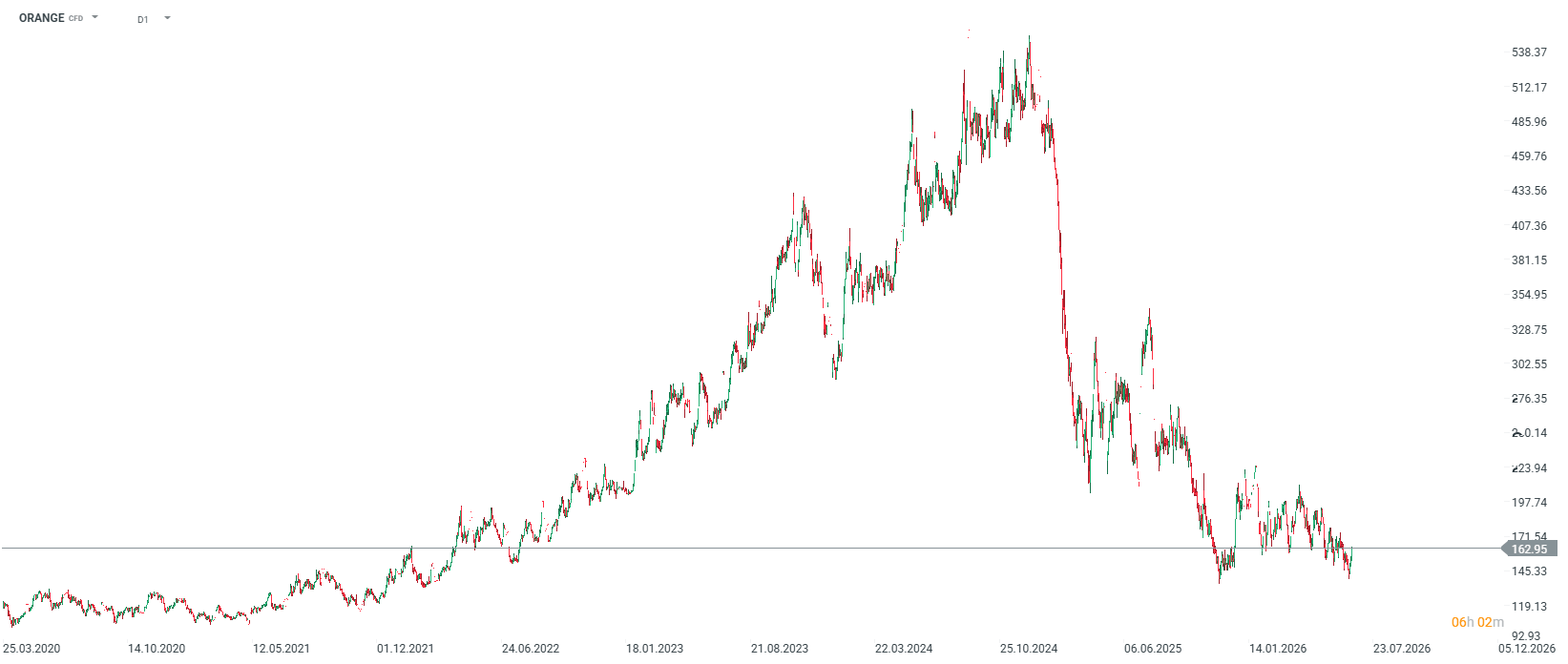

Orange Juice

- What is happening fundamentally: Quotations of frozen concentrated orange juice (FCOJ) are currently undergoing a rebound after testing the level of 140 cents per pound, although it is worth mentioning that as recently as 2024 quotations reached 540 cents per pound on fears for orange crops in the USA. In a broader perspective, this market has been through a historic supply crisis. Extreme droughts and heatwaves in Brazil and the uncontrolled spread of citrus greening disease (citrus greening) in Florida led to a drastic collapse of global production in recent years. Now, however, these fears essentially do not take place, and the market itself is prone to slightly increased interest, as at this point trading volumes remain extremely low compared to levels from several decades ago.

- Difference from other agricultural benchmarks: Orange juice is one of the most niche, "narrow" and illiquid commodity markets (so-called soft commodities). Unlike coffee or sugar, where production is spread across many countries, the orange juice market depends almost 100% on just two points on the map: the state of São Paulo in Brazil and Florida in the USA. Every local weather anomaly in these places generates powerful price gaps and violent speculative moves, incomparable with large agricultural markets.

Prices are down about 70% from their last peak. Source: xStation5

Prices are down about 70% from their last peak. Source: xStation5

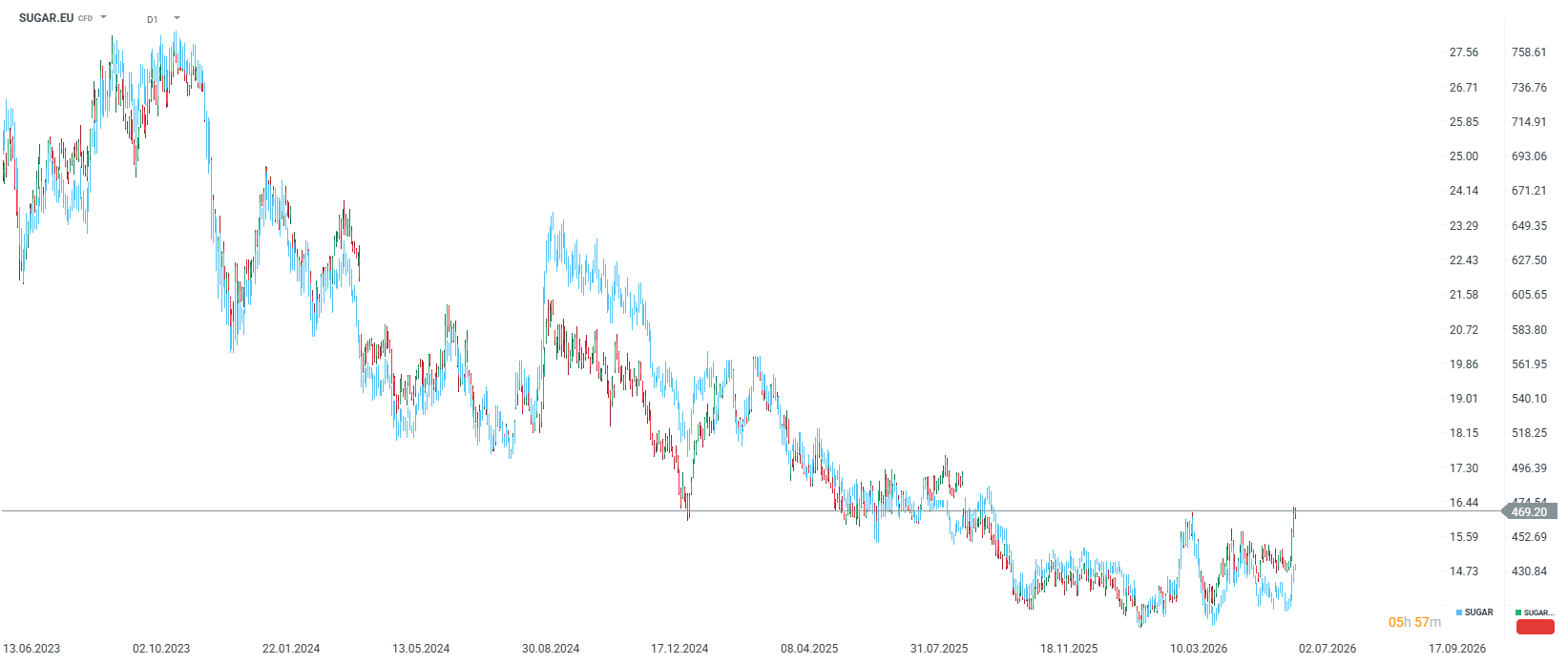

SUGAR.EU (White Sugar)

- What is happening fundamentally: The white sugar market (traded on the ICE Europe exchange in London) is moving in a stable sideways trend, and futures prices after consolidating at 430-440 shot up to nearly 470 USD per ton and are at their highest since September 2025. The exceptionally flat structure of the forward curve suggests that the global balance of supply and demand is currently relatively balanced. The biggest, fresh risk factor attracting investor attention at the end of June 2026 is a heatwave developing over key agricultural regions of Central Europe, threatening yields. Long-term, prices in this market are also supported by India's decision to ban sugar exports until the end of September to protect domestic reserves, as well as concerns about the negative impact of weather anomalies on harvests in Thailand.

- Difference from the main benchmark (Sugar No. 11 / SUGAR): The classic SUGAR instrument (based on the Sugar No. 11 contract from the New York exchange) reflects the prices of raw sugar (unrefined), obtained from sugar cane, where Brazil is the absolute supply hegemon. The new SUGAR.EU instrument (based on the Sugar No. 5 contract in London) concerns white sugar, fully refined (crystal), ready for direct use in the food industry. Crucially, in Europe, it is produced largely from sugar beets, not cane. The price difference between the two markets creates the so-called white sugar premium, reflecting the profitability of the refining process. By trading SUGAR.EU, an investor plays for European weather conditions, EU energy costs necessary for processing and local customs regulations, which gives a great field for arbitrage trading relative to cheaper raw sugar from the USA.

European sugar and American sugar. Source: xStation5

European sugar and American sugar. Source: xStation5

Economic Calendar: RBA Holds Rates, Markets Await US Housing Data

Daily Summary: Failure of negotiations in the gulf, oil and gas prices soar

⬆️TTF gas rises over 6% near 58 EUR

Morning Wrap: No Breakthrough in the Strait of Hormuz; Investors React to Berkshire Hathaway's Earnings

The content of this report has been created by XTB S.A., with its registered office in Warsaw, at Prosta 67, 00-838 Warsaw, Poland, (KRS number 0000217580) and supervised by Polish Supervision Authority ( No. DDM-M-4021-57-1/2005). This material is a marketing communication within the meaning of Art. 24 (3) of Directive 2014/65/EU of the European Parliament and of the Council of 15 May 2014 on markets in financial instruments and amending Directive 2002/92/EC and Directive 2011/61/EU (MiFID II). Marketing communication is not an investment recommendation or information recommending or suggesting an investment strategy within the meaning of Regulation (EU) No 596/2014 of the European Parliament and of the Council of 16 April 2014 on market abuse (market abuse regulation) and repealing Directive 2003/6/EC of the European Parliament and of the Council and Commission Directives 2003/124/EC, 2003/125/EC and 2004/72/EC and Commission Delegated Regulation (EU) 2016/958 of 9 March 2016 supplementing Regulation (EU) No 596/2014 of the European Parliament and of the Council with regard to regulatory technical standards for the technical arrangements for objective presentation of investment recommendations or other information recommending or suggesting an investment strategy and for disclosure of particular interests or indications of conflicts of interest or any other advice, including in the area of investment advisory, within the meaning of the Trading in Financial Instruments Act of 29 July 2005 (i.e. Journal of Laws 2019, item 875, as amended). The marketing communication is prepared with the highest diligence, objectivity, presents the facts known to the author on the date of preparation and is devoid of any evaluation elements. The marketing communication is prepared without considering the client’s needs, his individual financial situation and does not present any investment strategy in any way. The marketing communication does not constitute an offer of sale, offering, subscription, invitation to purchase, advertisement or promotion of any financial instruments. XTB S.A. is not liable for any client’s actions or omissions, in particular for the acquisition or disposal of financial instruments, undertaken on the basis of the information contained in this marketing communication. In the event that the marketing communication contains any information about any results regarding the financial instruments indicated therein, these do not constitute any guarantee or forecast regarding the future results.