Monday, May 25, began on financial markets with a sharp decline in oil prices, a powerful opening for Wall Street futures, and gains in the precious metals market. This situation is unfolding on a US market holiday due to Memorial Day. Throughout the weekend, hints suggested that a US-Iran agreement is very close, although Trump himself admitted it could probably take a few more days. Even though nothing has actually changed in reality, the market is once again living on hope and clearly reacting to the potential reopening of the Strait of Hormuz.

Brent crude is losing nearly 5%, trading at levels close to $95 per barrel, while WTI crude is dropping slightly more, trading around $91 per barrel. On the other hand, gold prices jumped 1% to $4,550, and silver is gaining as much as 2.5%, trading above $77 per ounce. S&P 500 futures are hitting consecutive all-time highs, nearing 7,559 points, gaining almost 1% ahead of the European market open.

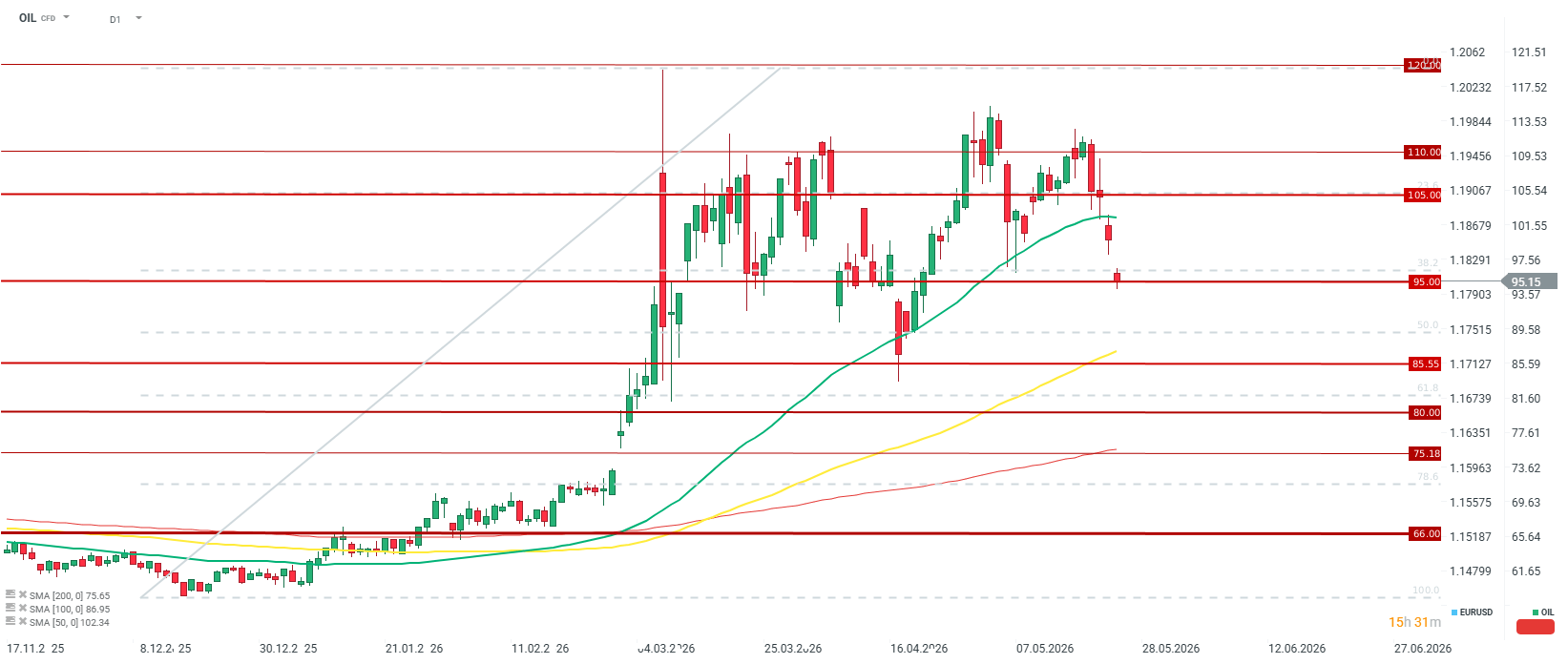

Crude oil is losing about 5% at the start of the final week of May, hitting its lowest levels in over a month. However, even with significant optimism, it seems that a short-term floor could be around $85 per barrel, and with a massive return of supply, somewhere around $75–$80 per barrel.Source: xStation5

Crude oil is losing about 5% at the start of the final week of May, hitting its lowest levels in over a month. However, even with significant optimism, it seems that a short-term floor could be around $85 per barrel, and with a massive return of supply, somewhere around $75–$80 per barrel.Source: xStation5

Anatomy of the Deal: What is Really on the Negotiation Table?

The technical outline of the potential agreement leaked to the media does not mean a lasting peace, but rather a temporary freezing of the crisis. The draft under discussion envisions a 60-day extension of the current, fragile ceasefire. During this period, the Strait of Hormuz would be conditionally reopened for commercial tanker traffic, and Iran would receive temporary permission to sell its own crude oil.

In exchange for this move, Tehran has agreed "in principle" to dispose of its stockpiles of highly enriched uranium. However, the devil is in the details: the precise timeline for this process and the final moratorium on further enrichment are to be postponed and negotiated only in an unspecified future. The draft agreement also includes winding down the parallel conflict between Israel and Hezbollah in Lebanon, which erupted about three months ago following a combined strike by US and Israeli forces on Tehran.

Despite US Secretary of State Marco Rubio publicly declaring that he is "very confident" a good compromise can be reached, internal political tensions on both sides could blow up the talks at any moment:

-

The dispute over frozen billions: Iran firmly demands the immediate unfreezing of its financial assets. Meanwhile, representatives of Donald Trump's administration have clearly informed reporters that the current framework of the agreement absolutely does not provide for the release of these funds. Iran's Tasnim news agency is already warning that because of this, the entire draft agreement could quickly be thrown into the trash.

-

Lack of key restrictions: The framework being developed does not impose a direct ban on Iran developing its missile arsenal or a permanent ban on uranium enrichment—Trump's two primary, original goals. This is provoking fury among American hawks. Senate Armed Services Committee Chairman Roger Wicker openly called the new ceasefire a "disaster" that wastes all previous military achievements of Operation Epic Fury. At the same time, it is worth noting that Trump emphasizes at every turn that Iran will never have a nuclear weapon.

-

Pressure from Israel: Prime Minister Benjamin Netanyahu, in a personal conversation with Trump, reminded him that any final agreement must unconditionally and completely eliminate the Iranian nuclear threat.

Logistic Reality: Why the Return of Oil Will Take Months

Even assuming an ultra-optimistic scenario where documents are signed within the next few days, the physical rebuilding of disrupted supply chains is a matter of many months, if not years. Futures markets react instantly, but physical infrastructure operates under entirely different rules.

The armed conflict has blocked the flow of approximately 14 million barrels of oil per day. The Strait of Hormuz handled nearly 20% of global oil and fuel supplies, as well as 20% of liquefied natural gas (LNG) transport. Although Saudi Arabia and the United Arab Emirates maximized the capacity of pipelines bypassing the strait, these alternative routes were unable to compensate for the massive supply gap. So far, the war has disrupted the flow of over a billion barrels of the commodity.

The most telling forecast comes from the CEO of the UAE's state-owned oil company, Adnoc. According to his estimates, even if hostilities were to end immediately, restoring volumes to just 80% of pre-war levels will take at least 4 months. Full pre-war transit capacity will return in the first or second half of 2027 at the earliest. However, it is also worth remembering that in the 1990s, the return of OPEC production was fast, and the price drop was even faster.

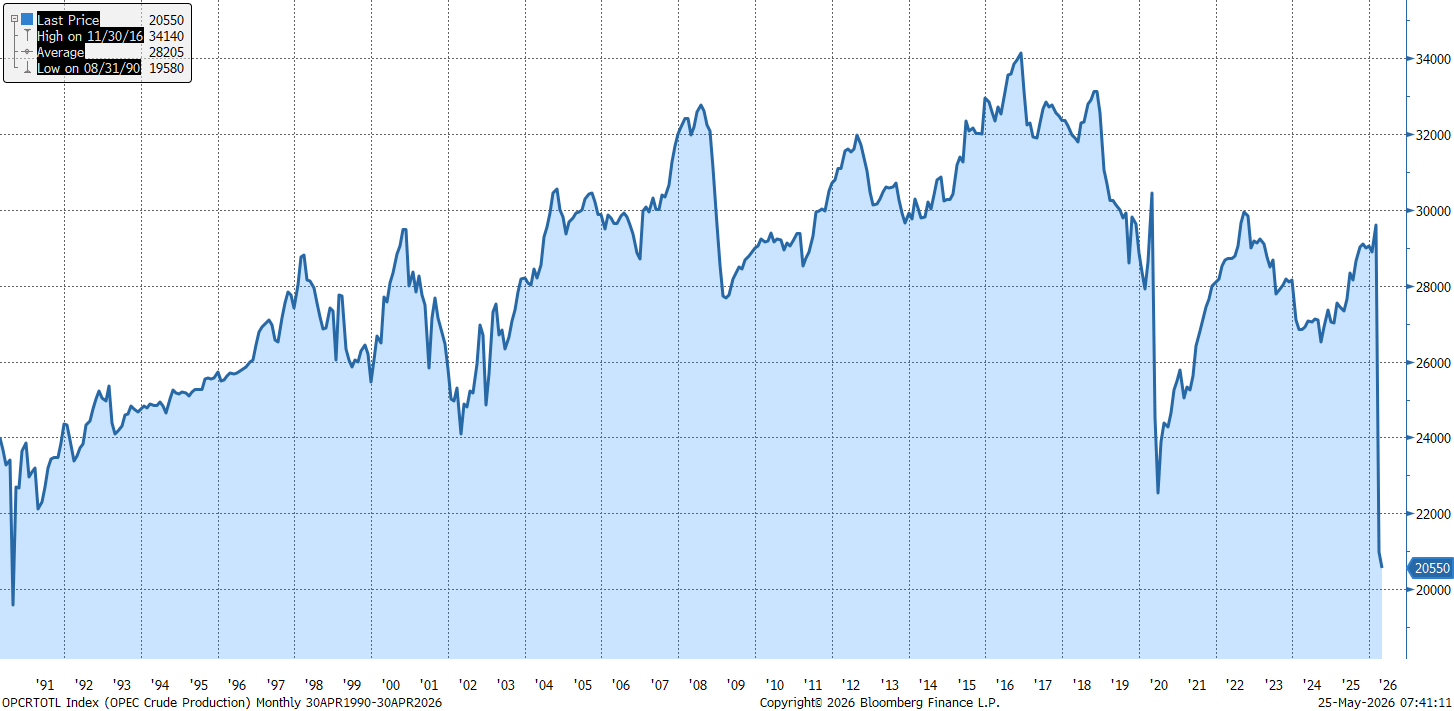

OPEC oil production has fallen to levels unseen since 1990. Back then, the recovery of production was very rapid and marked the beginning of a steady increase in the cartel's oil extraction until the end of the decade.Source: Bloomberg Finance LP

OPEC oil production has fallen to levels unseen since 1990. Back then, the recovery of production was very rapid and marked the beginning of a steady increase in the cartel's oil extraction until the end of the decade.Source: Bloomberg Finance LP

Price Forecasts: Will Brent Bid a Permanent Farewell to $100?

The current flight of capital away from crude oil contracts may prove premature. If hard evidence does not emerge in the coming days showing that US optimism was well-founded, the price of Brent crude will easily climb back above the $100 per barrel threshold.

The main structural problem in the markets remains the drastic depletion of global reserves. Consumer nations, saving their economies from paralysis, drained inventories at a record pace. In March and April alone, these inventories shrunk by another several hundred million barrels. The world now faces the necessity of refilling these empty tanks.

Provided that shipping traffic actually resumes in June, the US Energy Information Administration (EIA) forecasts an average Brent crude price of $89 per barrel by the end of this year and $79 in 2027. However, independent economists, such as Hamad Hussain from Capital Economics, are tempering expectations, pointing out that a real improvement in the supply-demand balance will not occur until later in 2027, keeping commodity prices elevated for much of the next dozen or so months.

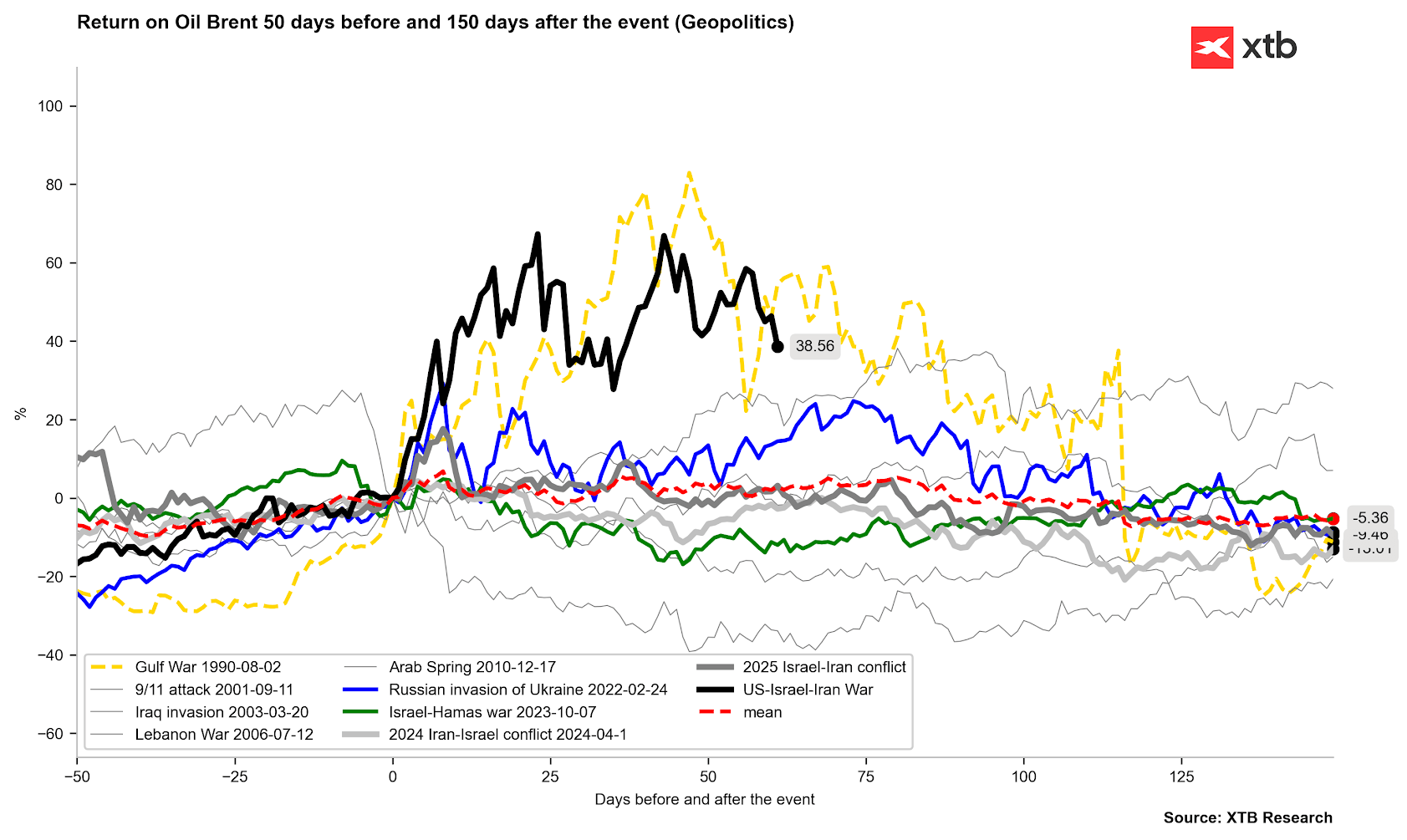

Crude oil prices are starting to move in the direction set by the situations in 1990 and 2022. Nonetheless, as history shows, the future path for oil could remain bumpy for many months to come.Source: Bloomberg Finance LP, XTB

Crude oil prices are starting to move in the direction set by the situations in 1990 and 2022. Nonetheless, as history shows, the future path for oil could remain bumpy for many months to come.Source: Bloomberg Finance LP, XTB

For the end consumer, another key factor remains: prices at gas stations may drop much more slowly than stock market oil quotes. Until cheaper crude reaches refineries and freight costs fall, pump prices will remain high. It is also worth mentioning that producing countries will need prices to be elevated relative to market realities to rebuild their infrastructure and transit channels.

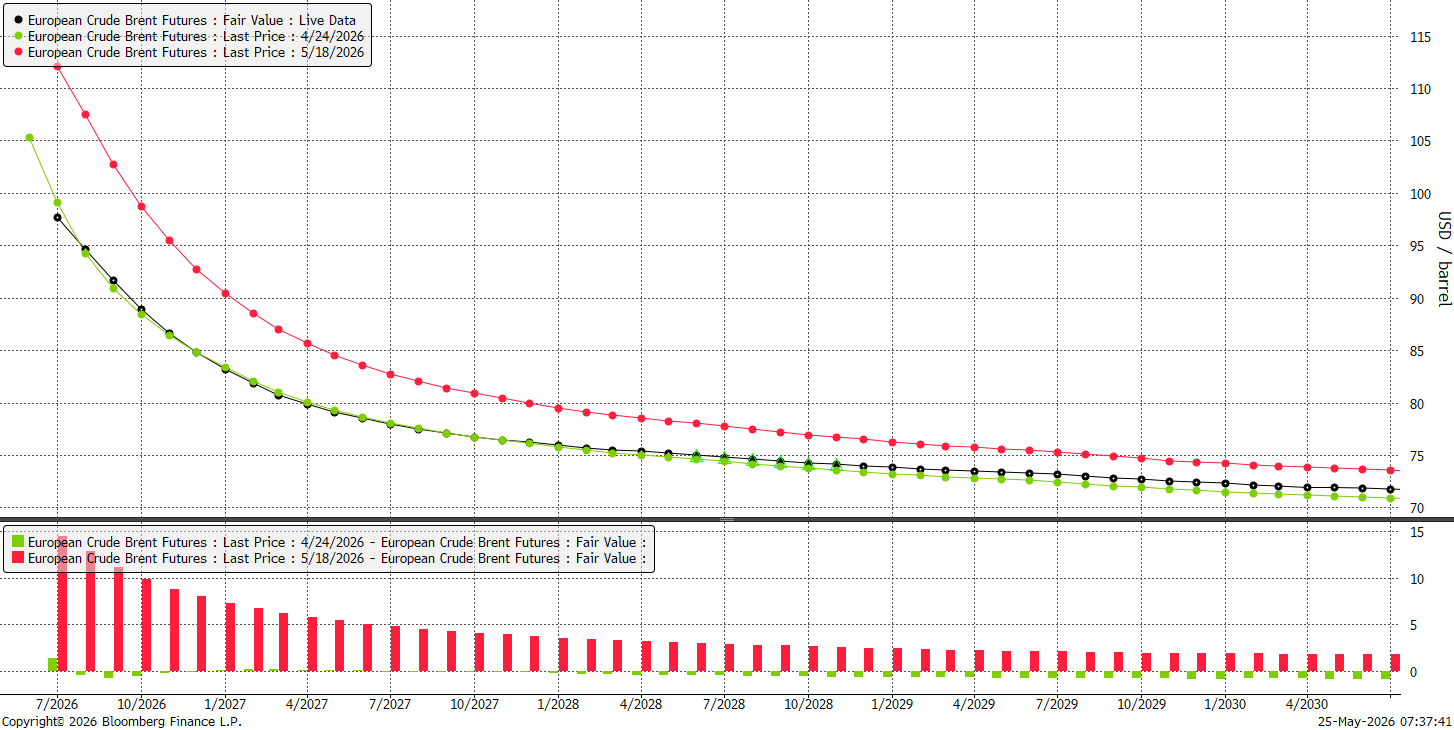

The current futures curve almost coincides with what it showed a month ago. On the other hand, a week ago, it was several to a dozen dollars higher. The normalization of calendar spreads is already quite significant, and the market appears to be in a balancing mode for April 2027, when oil is expected to trade at $80 per barrel.Source: Bloomberg Finance LP

The current futures curve almost coincides with what it showed a month ago. On the other hand, a week ago, it was several to a dozen dollars higher. The normalization of calendar spreads is already quite significant, and the market appears to be in a balancing mode for April 2027, when oil is expected to trade at $80 per barrel.Source: Bloomberg Finance LP

Oil Slides Ahead of the Weekend!

BREAKING: Eurozone recovery? Positive PMI data tempered by high oil and gas prices

Oil rises over 3% 🛢️

Defense sector ahead of earnings: Summary

The content of this report has been created by XTB S.A., with its registered office in Warsaw, at Prosta 67, 00-838 Warsaw, Poland, (KRS number 0000217580) and supervised by Polish Supervision Authority ( No. DDM-M-4021-57-1/2005). This material is a marketing communication within the meaning of Art. 24 (3) of Directive 2014/65/EU of the European Parliament and of the Council of 15 May 2014 on markets in financial instruments and amending Directive 2002/92/EC and Directive 2011/61/EU (MiFID II). Marketing communication is not an investment recommendation or information recommending or suggesting an investment strategy within the meaning of Regulation (EU) No 596/2014 of the European Parliament and of the Council of 16 April 2014 on market abuse (market abuse regulation) and repealing Directive 2003/6/EC of the European Parliament and of the Council and Commission Directives 2003/124/EC, 2003/125/EC and 2004/72/EC and Commission Delegated Regulation (EU) 2016/958 of 9 March 2016 supplementing Regulation (EU) No 596/2014 of the European Parliament and of the Council with regard to regulatory technical standards for the technical arrangements for objective presentation of investment recommendations or other information recommending or suggesting an investment strategy and for disclosure of particular interests or indications of conflicts of interest or any other advice, including in the area of investment advisory, within the meaning of the Trading in Financial Instruments Act of 29 July 2005 (i.e. Journal of Laws 2019, item 875, as amended). The marketing communication is prepared with the highest diligence, objectivity, presents the facts known to the author on the date of preparation and is devoid of any evaluation elements. The marketing communication is prepared without considering the client’s needs, his individual financial situation and does not present any investment strategy in any way. The marketing communication does not constitute an offer of sale, offering, subscription, invitation to purchase, advertisement or promotion of any financial instruments. XTB S.A. is not liable for any client’s actions or omissions, in particular for the acquisition or disposal of financial instruments, undertaken on the basis of the information contained in this marketing communication. In the event that the marketing communication contains any information about any results regarding the financial instruments indicated therein, these do not constitute any guarantee or forecast regarding the future results.