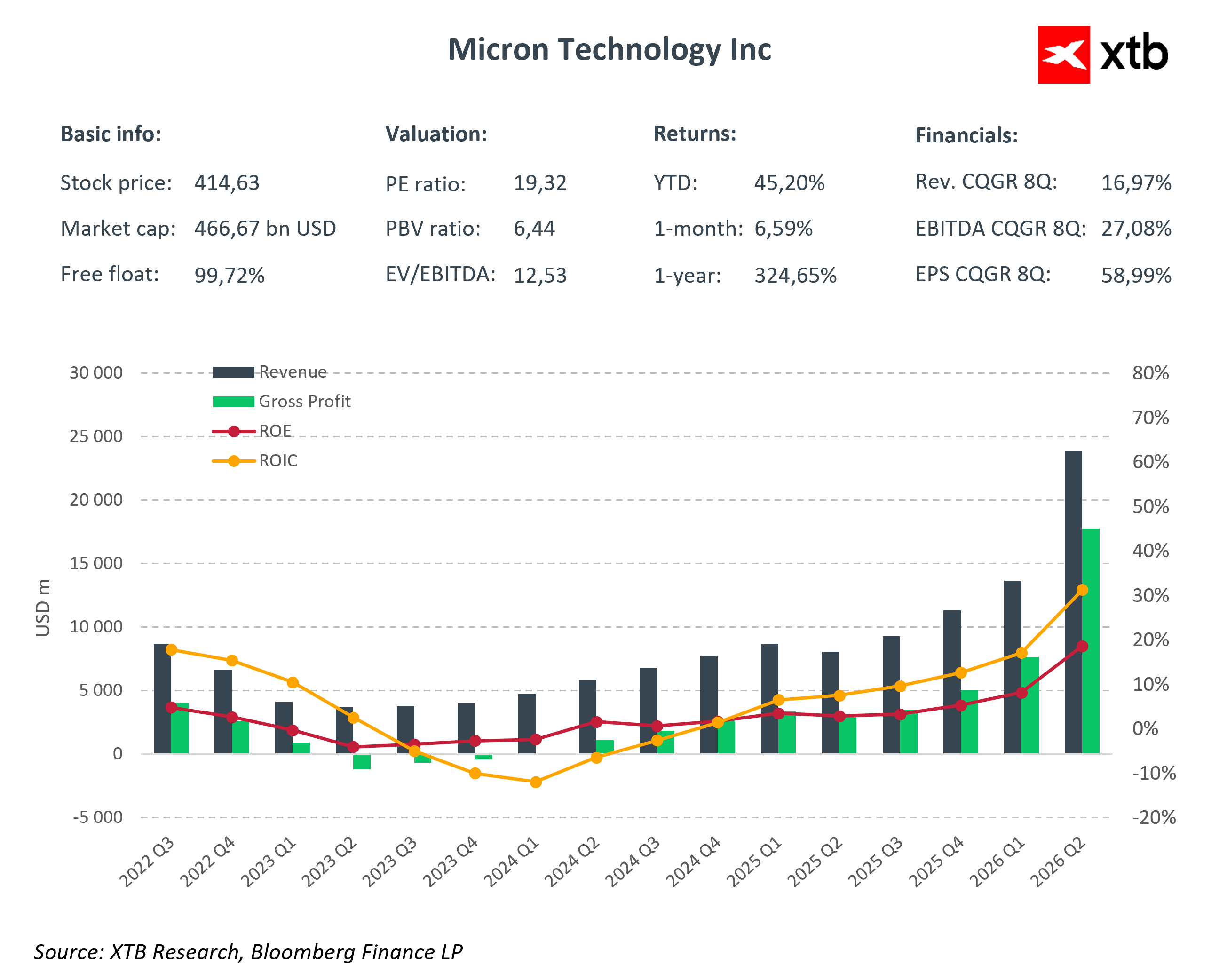

Micron Technology announced record results for the second quarter of fiscal 2026, surpassing market expectations by double-digit figures and confirming that the AI-driven memory supercycle is entering an unprecedented profitability phase. Despite the fundamentally euphoric reception of the results, the company’s shares fell five to seven percent after the session due to concerns over higher capital expenditures, representing a classic “sell the news” scenario that does not alter the long-term growth trajectory.

Key Financial Results Q2 FY2026:

-

Revenue: USD 23.86 billion (+75% q/q, +196% y/y; market consensus USD 19 billion)

-

Net Income: USD 14.02 billion

-

EPS: USD 12.20

-

Gross Margin: 74.4%

-

Operating Cash Flow: USD 11.90 billion

Such a spectacular beat of estimates is no accident. Micron is fully leveraging sold-out HBM and server DRAM inventories, where hyperscaler demand significantly exceeds supply. Margins have returned to historical cycle highs, and strong operating leverage has translated revenue growth into exponential profit gains.

Segment Growth Breakdown

Q2 FY2026 results demonstrate that Micron’s growth is primarily driven by cloud and AI-related segments, which have become the foundation of the memory supercycle.

-

Cloud Memory Business Unit: Revenue reached USD 7.75 billion with an operating margin of 66%, driven by strong demand for HBM3E and HBM4 for AI accelerators. The backlog for the current fiscal year is effectively sold out, providing exceptional revenue visibility for upcoming quarters.

-

Core Data Center Business Unit: Revenue totaled USD 5.69 billion, a 139% q/q increase, with an operating margin of 62%. This segment primarily serves server DRAM for hyperscalers and data centers investing in AI infrastructure.

-

Mobile & Client Business Unit: Generated USD 7.71 billion in revenue with a 76% operating margin, reflecting a recovery in smartphones and PCs, as well as a growing share of high-margin products in the sales mix.

-

Automotive & Embedded Business Unit: Revenue reached USD 2.71 billion with a 52% margin, driven by growing demand for embedded memory, automotive solutions, and IoT applications.

All segments reported improved profitability, demonstrating a successful product mix restructuring. The share of advanced memory, including HBM and modern data center DRAM, increased to over 40% of total sales, significantly raising the company’s average margin.

This product mix enhances profitability and reduces Micron’s sensitivity to cyclical consumer market fluctuations. High-value-added products act as barriers to entry for competitors, ensuring stable revenues and a strategic advantage in pricing negotiations and production planning for the coming years.

Q3 FY2026 Guidance, Dividend, and Capital Expenditures

Following the record Q2 results, Micron issued an exceptionally ambitious guidance for the third quarter, significantly exceeding market expectations. Management anticipates:

-

Revenue: approximately USD 33.5 billion

-

EPS: USD 19.15

-

Gross Margin: approximately 81%

The guidance reflects persistently tight HBM demand and full utilization of production capacity in FY2026 and FY2027, providing high revenue visibility for upcoming quarters.

Additionally, Micron announced a 30% increase in the quarterly dividend to USD 0.15 per share, signaling confidence in cash generation and financial stability.

At the same time, forecasted CapEx for Q3 is USD 7–8 billion, with total FY2026 spending around USD 30 billion. These significant investments triggered short-term market concerns, leading to a post-session stock decline—a typical “sell the news” effect. However, these expenditures are strategic, aimed at maintaining technological leadership in HBM and expanding production capacity to meet growing AI and data center memory demand.

Industry Context and Micron’s Market Position

The current memory supercycle, in which Micron plays a key role, is primarily structural and driven by the rapid expansion of artificial intelligence, data centers, and modern computing infrastructure. Unlike previous cycles, revenue growth is not solely due to DRAM and NAND price rebounds but stems from sustained demand for high-value-added advanced products. DRAM prices increased 90–95% q/q in the last quarter, and NAND prices rose 55–60%, with the growing share of HBM and server memory maintaining record margins.

Barriers to entry in the HBM segment are high, as only a few suppliers operate globally, protecting Micron’s profitability and increasing revenue predictability. At the same time, industry risks, including geopolitical tensions in Asia, consumer demand fluctuations, competitive pressure, and the cyclical nature of the memory market, remain relevant. However, the current product mix and strong AI segment position significantly reduce the company’s sensitivity to short-term market swings.

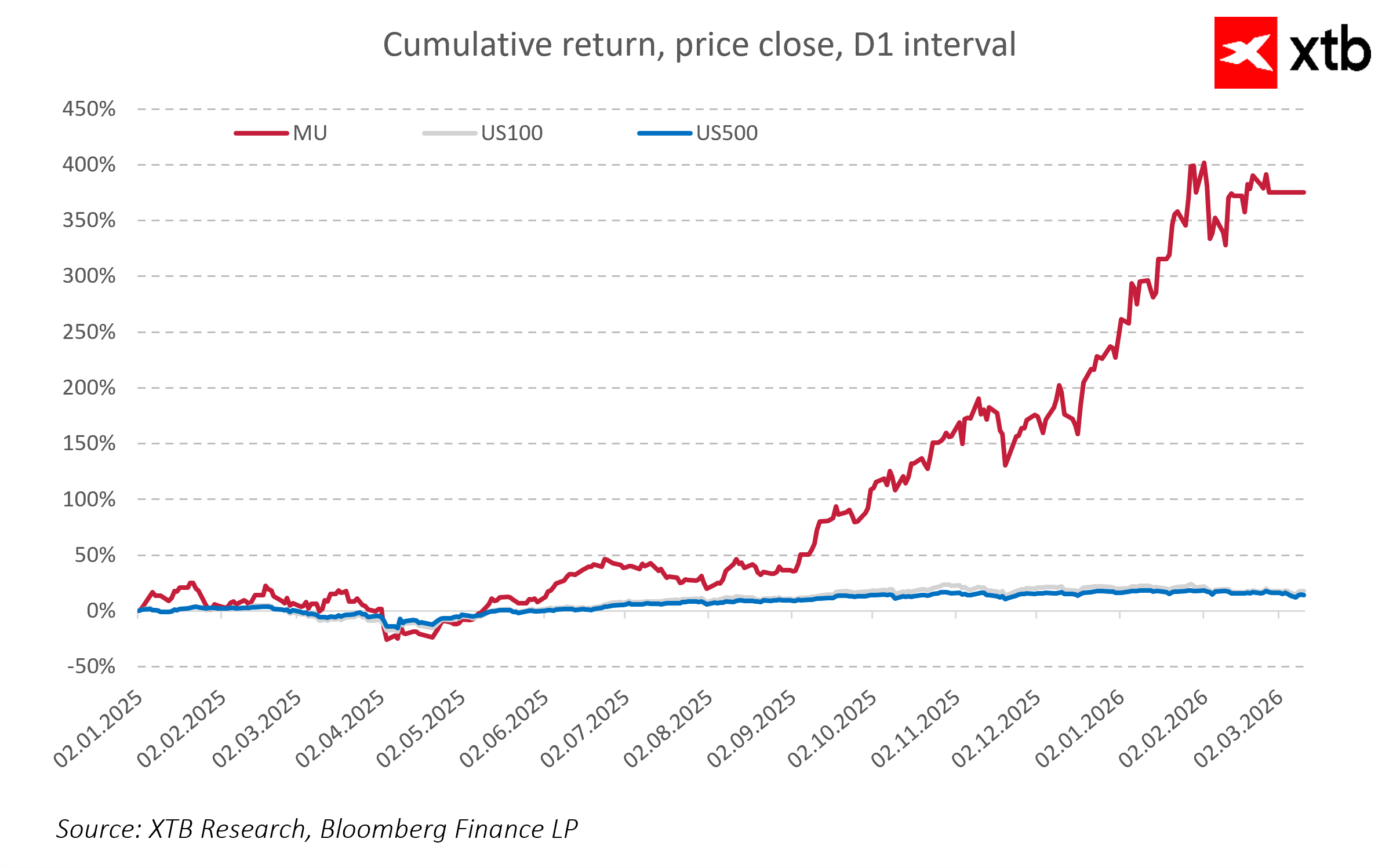

Micron is currently seen as a pure beneficiary of the AI memory boom, with its shares outperforming broader U.S. indices, confirming the investment attractiveness amid rising revenues and stable margins. The durability of the memory supercycle supports continued revenue expansion even through 2028, with annual growth of 50–70% in data center and AI memory segments.

Financial Analysis of Micron Technology Q2 FY2026 and Outlook

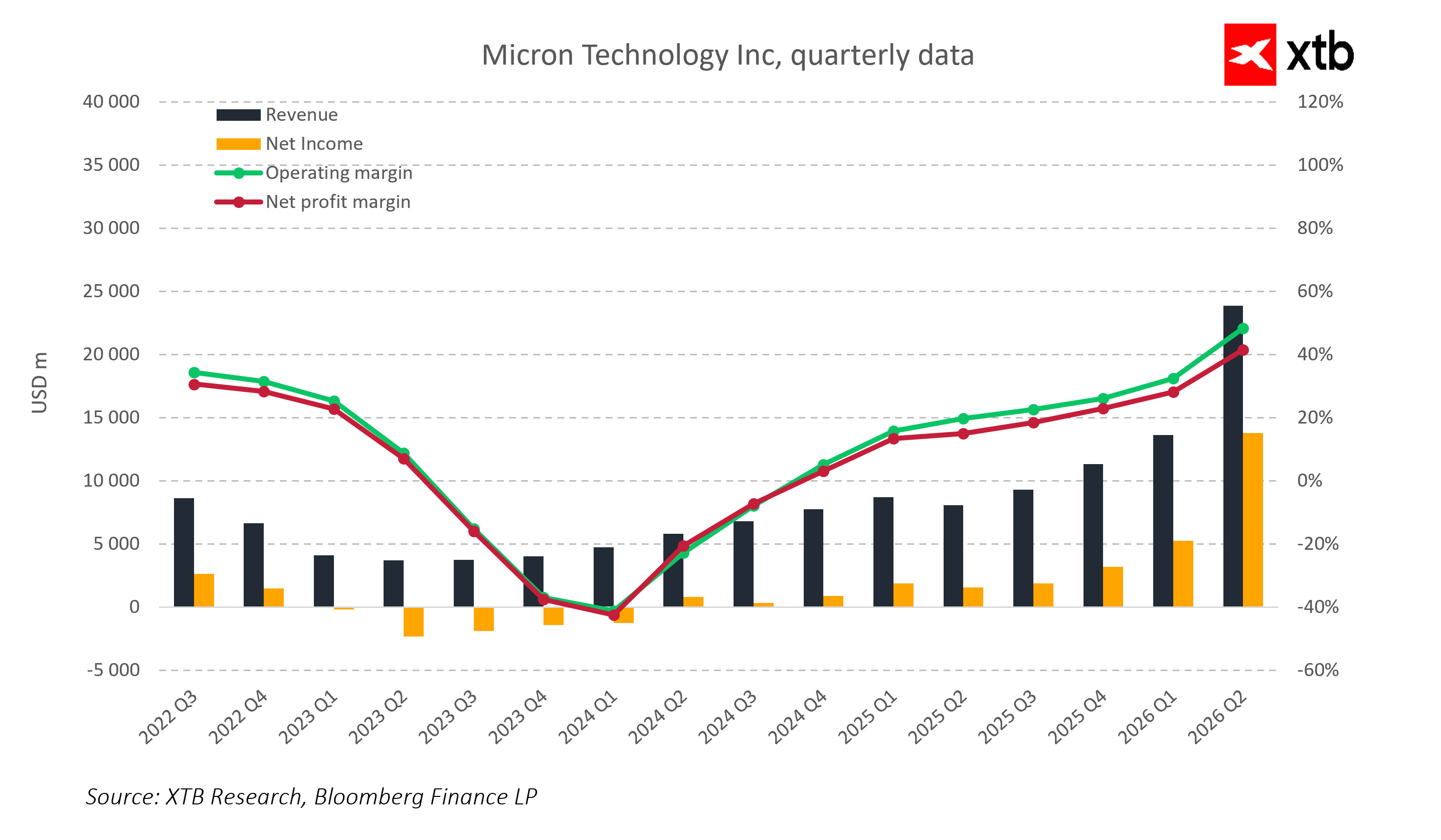

Micron Technology achieved spectacular results in Q2 FY2026. Revenue reached a record USD 23.86 billion, up 75% q/q and 196% y/y. Such dynamic growth confirms the company’s dominant position in the memory market, especially in advanced solutions for AI and data centers.

Operational profitability also improved significantly. Non-GAAP gross margin reached 74.4%, a level characteristic of historical memory cycle peaks. GAAP net income exceeded USD 13.79 billion, and non-GAAP EPS reached USD 12.20, a 150% q/q increase. High margins reflect a favorable product mix, with growing shares of HBM and server DRAM solutions, which are highly profitable and have stable, predictable demand.

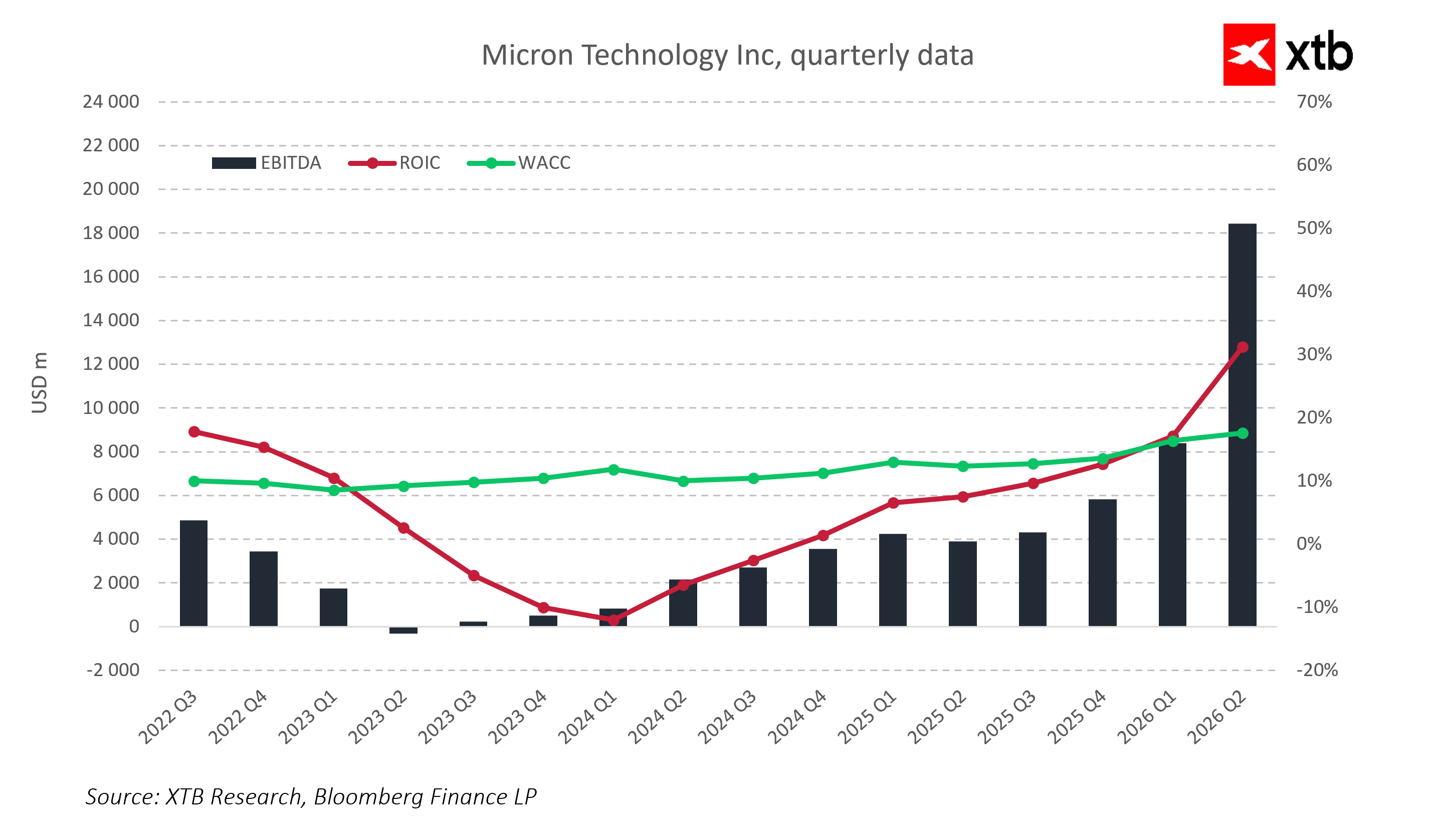

Operating cash flow increased to USD 11.90 billion, confirming the company’s ability to generate significant cash while financing intensive capital investments. Net CapEx in Q2 reached USD 5 billion, reflecting aggressive expansion of production capacity and maintenance of technological leadership. Q3 CapEx is expected to rise to USD 7–8 billion, demonstrating a long-term growth strategy and preparation for further HBM expansion.

From a capital efficiency perspective, Micron has significantly improved ROIC, exceeding the cost of capital (WACC), indicating value creation for shareholders and effective use of development resources.

The balance sheet remains strong and stable. High cash levels provide liquidity comfort and flexibility in future investment decisions. Financial stability is crucial in the semiconductor industry, where investments are large and market cycles volatile.

Guidance for the upcoming quarters remains optimistic. Management expects Q3 FY2026 revenue around USD 33.5 billion, gross margin of 81%, and non-GAAP EPS of approximately USD 19.15. This high forecast reflects continued strong demand for HBM and DRAM, as well as sold-out production capacity for the upcoming quarters.

Q2 FY2026 results and forward-looking guidance clearly indicate that Micron is in an exceptionally favorable stage of its development. Significant revenue growth, record margins, effective cost management, and intensive capital investments create a solid foundation for continued expansion. Micron strengthens its position in the growing memory market, driven by increasing demand for advanced AI and data center solutions. All these factors point to further growth potential and financial stability in the coming quarters.

Valuation Overview

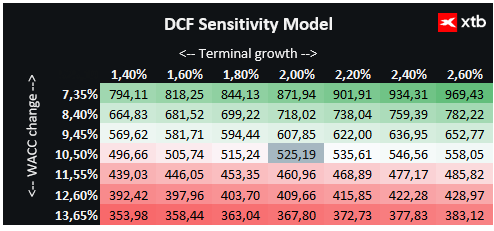

We valued Micron Technology using a discounted cash flow (DCF) model. This analysis is for informational purposes only and does not constitute an investment recommendation or exact stock valuation.

The model assumes continued dynamic revenue growth, driven primarily by DRAM, NAND, and HBM segments, which form the core of the company’s business. Initial growth is particularly strong due to rising demand for advanced memory solutions in AI, data centers, and modern mobile devices.

Further growth prospects are supported by technological innovation, including new memory generations that enhance performance and product functionality.

The valuation model assumes a cost of capital (WACC) of 10.5% throughout the forecast period, reflecting sector specifics and Micron’s moderate debt. The terminal value is based on a conservative revenue growth rate of 2%.

Based on the analysis, Micron Technology Inc’s stock is valued at USD 525.19, exceeding the current market price of USD 435.00 and implying a potential upside of 21%. Current fundamentals and financial forecasts indicate that Micron occupies a favorable position in the semiconductor memory cycle, combining characteristics of a cyclical rebound with long-term growth driven by AI and data center infrastructure development.

Key Takeaways

Micron Technology closed Q2 FY2026 with impressive financial results, demonstrating the company is in a strong growth phase with stable profitability. Revenue nearly doubled compared to the previous year, and margins reached levels typical of the strongest points in the memory cycle. Efficient operating cost management and strong cash flow allow simultaneous financing of aggressive technology investments and expansion of production capacity.

Business segments focused on HBM and data center solutions are experiencing exceptionally dynamic growth, confirming the durability of demand for high-margin advanced products. Tight supply and sold-out backlogs for upcoming quarters provide high revenue and profit visibility.

Strategic capital investments, while raising short-term investor concerns, are essential for maintaining competitive advantage and meeting rising market demand. Dividend growth reflects management confidence in the company’s continued stability and cash generation.

Overall, Micron Technology’s financial position is exceptionally strong, and outlooks for the coming quarters indicate the continuation of a positive trend driven by fundamental, structural growth factors in the semiconductor memory industry.

Daily Summary: Equities Diverge as Tech Lags, Europe Rallies on Earnings & PMIs (24.07.2026)

US OPEN: Nasdaq hits 1-month low! Geopolitics bring AI trade down!

Market Wrap: European Stocks Are Trying to Rebound as the Week Comes to an End💡

Alphabet shares are down 22% from their all-time high 🚩 Is Google ready to resume its bull run?

The content of this report has been created by XTB S.A., with its registered office in Warsaw, at Prosta 67, 00-838 Warsaw, Poland, (KRS number 0000217580) and supervised by Polish Supervision Authority ( No. DDM-M-4021-57-1/2005). This material is a marketing communication within the meaning of Art. 24 (3) of Directive 2014/65/EU of the European Parliament and of the Council of 15 May 2014 on markets in financial instruments and amending Directive 2002/92/EC and Directive 2011/61/EU (MiFID II). Marketing communication is not an investment recommendation or information recommending or suggesting an investment strategy within the meaning of Regulation (EU) No 596/2014 of the European Parliament and of the Council of 16 April 2014 on market abuse (market abuse regulation) and repealing Directive 2003/6/EC of the European Parliament and of the Council and Commission Directives 2003/124/EC, 2003/125/EC and 2004/72/EC and Commission Delegated Regulation (EU) 2016/958 of 9 March 2016 supplementing Regulation (EU) No 596/2014 of the European Parliament and of the Council with regard to regulatory technical standards for the technical arrangements for objective presentation of investment recommendations or other information recommending or suggesting an investment strategy and for disclosure of particular interests or indications of conflicts of interest or any other advice, including in the area of investment advisory, within the meaning of the Trading in Financial Instruments Act of 29 July 2005 (i.e. Journal of Laws 2019, item 875, as amended). The marketing communication is prepared with the highest diligence, objectivity, presents the facts known to the author on the date of preparation and is devoid of any evaluation elements. The marketing communication is prepared without considering the client’s needs, his individual financial situation and does not present any investment strategy in any way. The marketing communication does not constitute an offer of sale, offering, subscription, invitation to purchase, advertisement or promotion of any financial instruments. XTB S.A. is not liable for any client’s actions or omissions, in particular for the acquisition or disposal of financial instruments, undertaken on the basis of the information contained in this marketing communication. In the event that the marketing communication contains any information about any results regarding the financial instruments indicated therein, these do not constitute any guarantee or forecast regarding the future results.