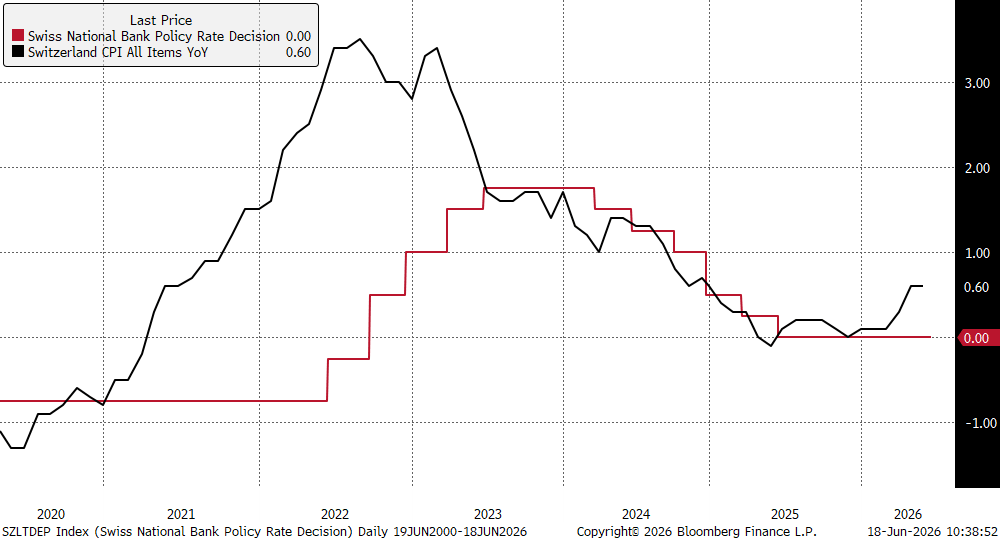

The Swiss National Bank (SNB) decided to keep its main interest rate unchanged during its June meeting. The interest rate has remained unchanged exactly since June last year. It is worth emphasizing that interest rate decisions in Switzerland are made quarterly. The interest rate remains at 0% and currently, due to slightly elevated inflation, we should not expect any pressure for cuts, but at the same time, it is still far from the upper limit of the inflation target.

Despite the fact that the war in Iran caused a temporary increase in imported energy prices and pushed the May inflation reading to 0.6%, the Swiss CPI index still sits comfortably in the lower range of the 0-2% inflation target.

Switzerland shows significantly less dependence on energy commodities from the Middle East thanks to developed hydropower and nuclear energy, which protects the local economy from global price shocks more strongly than the Eurozone. The main focus for policymakers remains the exchange rate of the Swiss franc and the risk of its excessive appreciation in the face of geopolitical uncertainty.

Macroeconomic forecasts

The SNB made a slight upward revision to its inflation forecasts in the short and medium term:

- Inflation: The Bank now forecasts average inflation at 0.6% in 2026 (up from 0.5% in the March forecast) and 0.6% in 2027 (also up from 0.5%). In 2028, inflation is expected to be 0.7% (compared to 0.6% previously), and a reading of 0.8% is expected in the first quarter of 2029.

- GDP Growth: Economic forecasts remained unchanged. The SNB expects the Swiss economy to grow by about 1.0% in 2026 and 1.5% in 2027.

Statements from bankers at the SNB conference

Key members of the SNB Governing Board sent clear signals during today's conference:

- Martin Schlegel (Chairman of the SNB):

- "If necessary, we show an increased readiness to intervene in the foreign exchange market. In this way, we counteract a rapid and excessive strengthening of the Swiss franc, which would threaten price stability in Switzerland".

- "Inflation has risen in recent months as a result of higher energy prices. However, medium-term inflationary pressure is virtually unchanged compared to the last monetary policy assessment".

- "Everything between 0 and 2% is fine regarding inflation" and "no preference as to where in the range inflation is located".

- He also indicated that monetary conditions are weaker than in March, and the bank does not currently see second-round effects in Switzerland.

- Antoine Martin (Member of the SNB Governing Board):

- He pointed out that the situation in the Middle East remains fragile, adding that global inflation should be expected to remain at an elevated level.

- Attilio Tschudin (Member of the SNB Governing Board):

- He noted that domestic indicators show a solid economic recovery, but the main risk for Swiss prospects is the condition of the global economy.

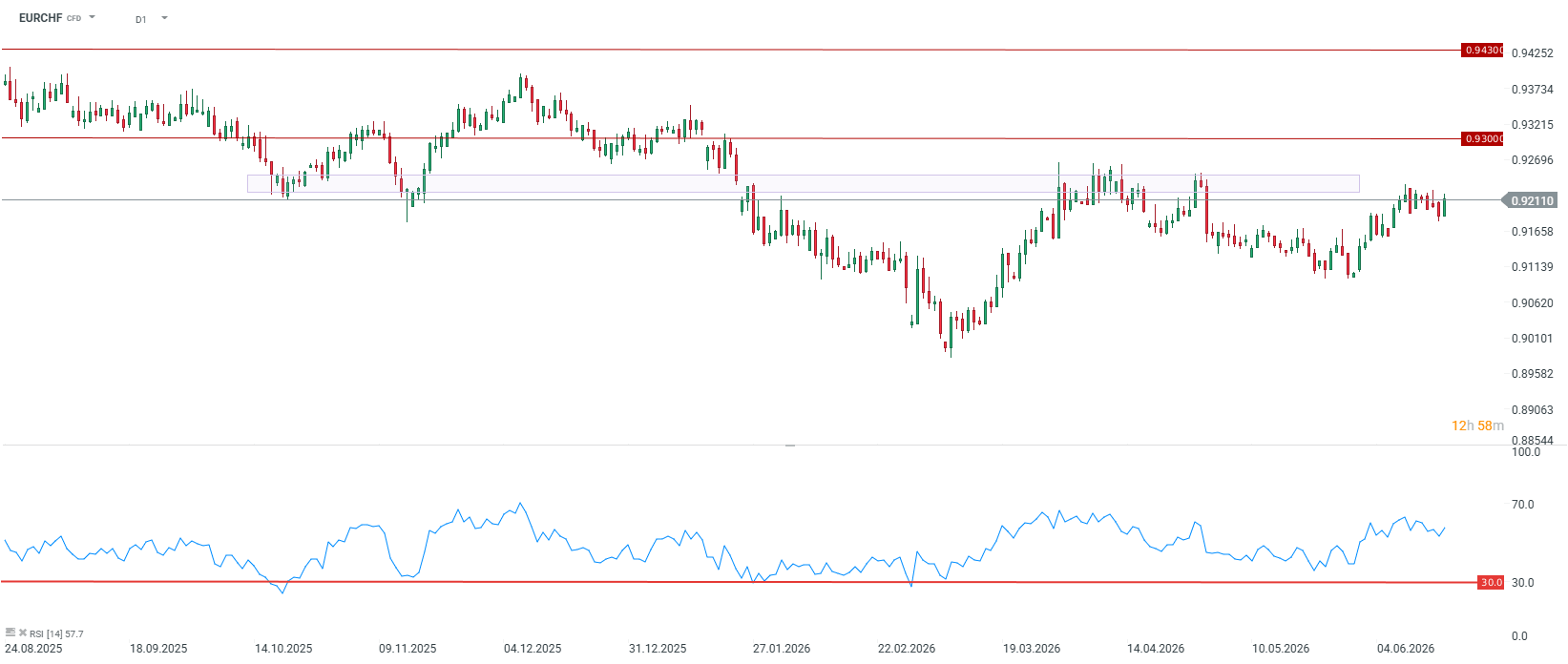

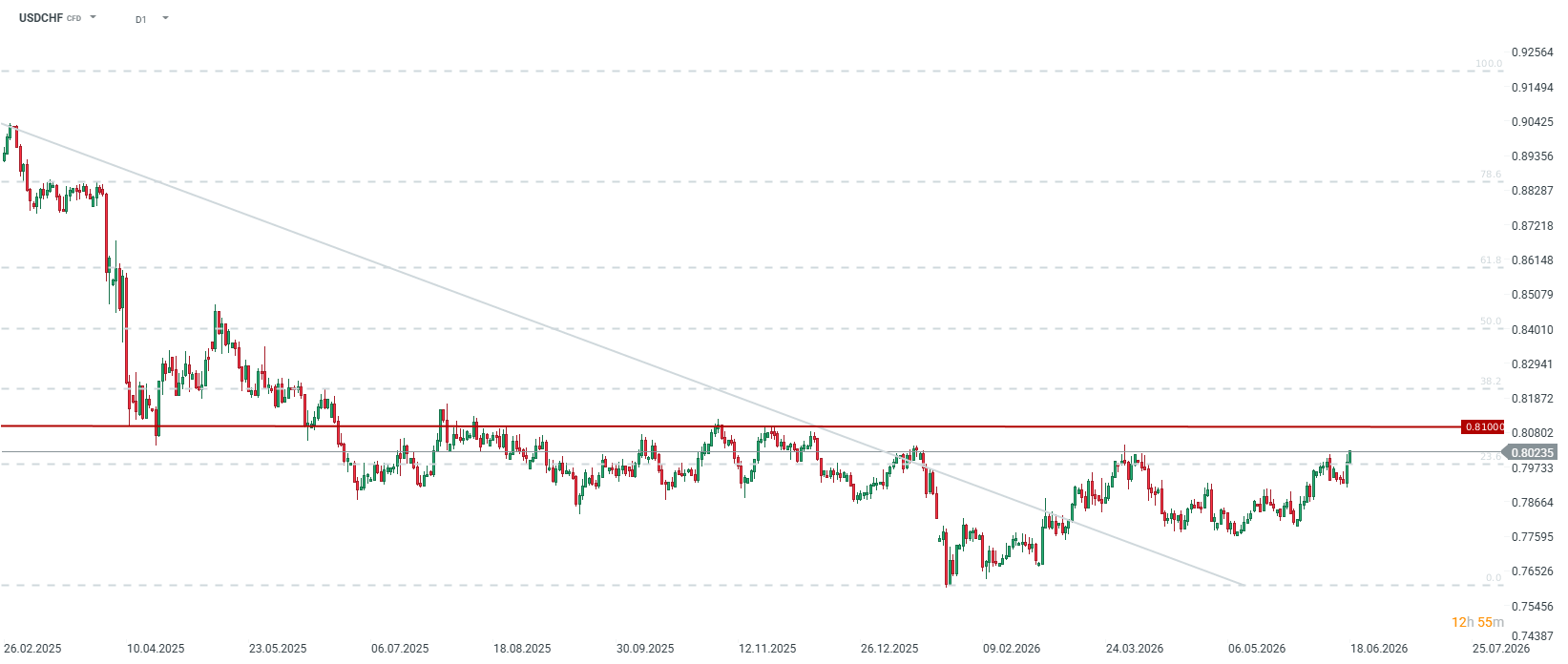

What to expect for EURCHF and USDCHF?

EURCHF

Immediately after the decision was announced, the franc weakened slightly against the euro, falling by 0.2%-0.3% to a level of around 0.9215 per euro. Since the sudden strengthening of the franc at the turn of February and March (outbreak of war in Iran), clear communication from the SNB about its readiness to intervene has systematically pushed the CHF rate down. A strong supply zone for the pair is around 0.9220 to 0.9250.

USDCHF

Wednesday's signing of a peace agreement in Versailles between the US and Iran by President Trump and the Iranian President is a strong factor mitigating tensions in energy commodity markets. This means a drop in demand for the franc as a "safe haven," which should favor a rebound and stabilization of EURCHF and USDCHF rates.

Nevertheless, due to Martin Schlegel's declared "increased readiness to intervene" in the event of any turmoil, investors must take into account that the SNB is artificially limiting the franc's potential for further strengthening. Any sudden attempts at CHF appreciation will likely be met with a decisive sell-off of the currency by the Swiss central bank, which sets a solid long-term floor for EURCHF and USDCHF quotes.

🟡Gold tests $4000 ahead of the Fed decision

France Challenges Palantir, Market Reacts.

Morning Wrap: US halt to attacks balanced by semiconductor sector declines (28.07.2026)

Oil Slides Ahead of the Weekend!

The content of this report has been created by XTB S.A., with its registered office in Warsaw, at Prosta 67, 00-838 Warsaw, Poland, (KRS number 0000217580) and supervised by Polish Supervision Authority ( No. DDM-M-4021-57-1/2005). This material is a marketing communication within the meaning of Art. 24 (3) of Directive 2014/65/EU of the European Parliament and of the Council of 15 May 2014 on markets in financial instruments and amending Directive 2002/92/EC and Directive 2011/61/EU (MiFID II). Marketing communication is not an investment recommendation or information recommending or suggesting an investment strategy within the meaning of Regulation (EU) No 596/2014 of the European Parliament and of the Council of 16 April 2014 on market abuse (market abuse regulation) and repealing Directive 2003/6/EC of the European Parliament and of the Council and Commission Directives 2003/124/EC, 2003/125/EC and 2004/72/EC and Commission Delegated Regulation (EU) 2016/958 of 9 March 2016 supplementing Regulation (EU) No 596/2014 of the European Parliament and of the Council with regard to regulatory technical standards for the technical arrangements for objective presentation of investment recommendations or other information recommending or suggesting an investment strategy and for disclosure of particular interests or indications of conflicts of interest or any other advice, including in the area of investment advisory, within the meaning of the Trading in Financial Instruments Act of 29 July 2005 (i.e. Journal of Laws 2019, item 875, as amended). The marketing communication is prepared with the highest diligence, objectivity, presents the facts known to the author on the date of preparation and is devoid of any evaluation elements. The marketing communication is prepared without considering the client’s needs, his individual financial situation and does not present any investment strategy in any way. The marketing communication does not constitute an offer of sale, offering, subscription, invitation to purchase, advertisement or promotion of any financial instruments. XTB S.A. is not liable for any client’s actions or omissions, in particular for the acquisition or disposal of financial instruments, undertaken on the basis of the information contained in this marketing communication. In the event that the marketing communication contains any information about any results regarding the financial instruments indicated therein, these do not constitute any guarantee or forecast regarding the future results.