Key statements regarding Trump's speech at the NATO summit in Ankara

- End of diplomatic handling of Iran: Trump announced that the temporary agreement with Tehran is dead. He announced further strikes (energy infrastructure and Kharg Island are at play) to "finish the job." He will not send ground troops but will not stop harassing merchant ships.

- War-scale production momentum: He considered the current NATO summit a success, announcing that the US could immediately quadruple ammunition production, and Lockheed Martin will create a massive service center in Europe.

- Setting terms: Israel is to withdraw from southern Lebanon, Syria is to help contain Hezbollah, and the EU (starting with Spain) received a warning about a possible trade embargo.

- Oil as a tool: Trump claims that there is currently oversupply in the market and that ultimately prices will fall significantly. The US is to secure routes so that the transport of the raw material is "free, easy, and fast." On the other hand, he does not rule out short-term upward pressure.

What's next for oil?

The oil market now has the perfect recipe for another massive rollercoaster, as Trump's narrative clashes with brutal reality.

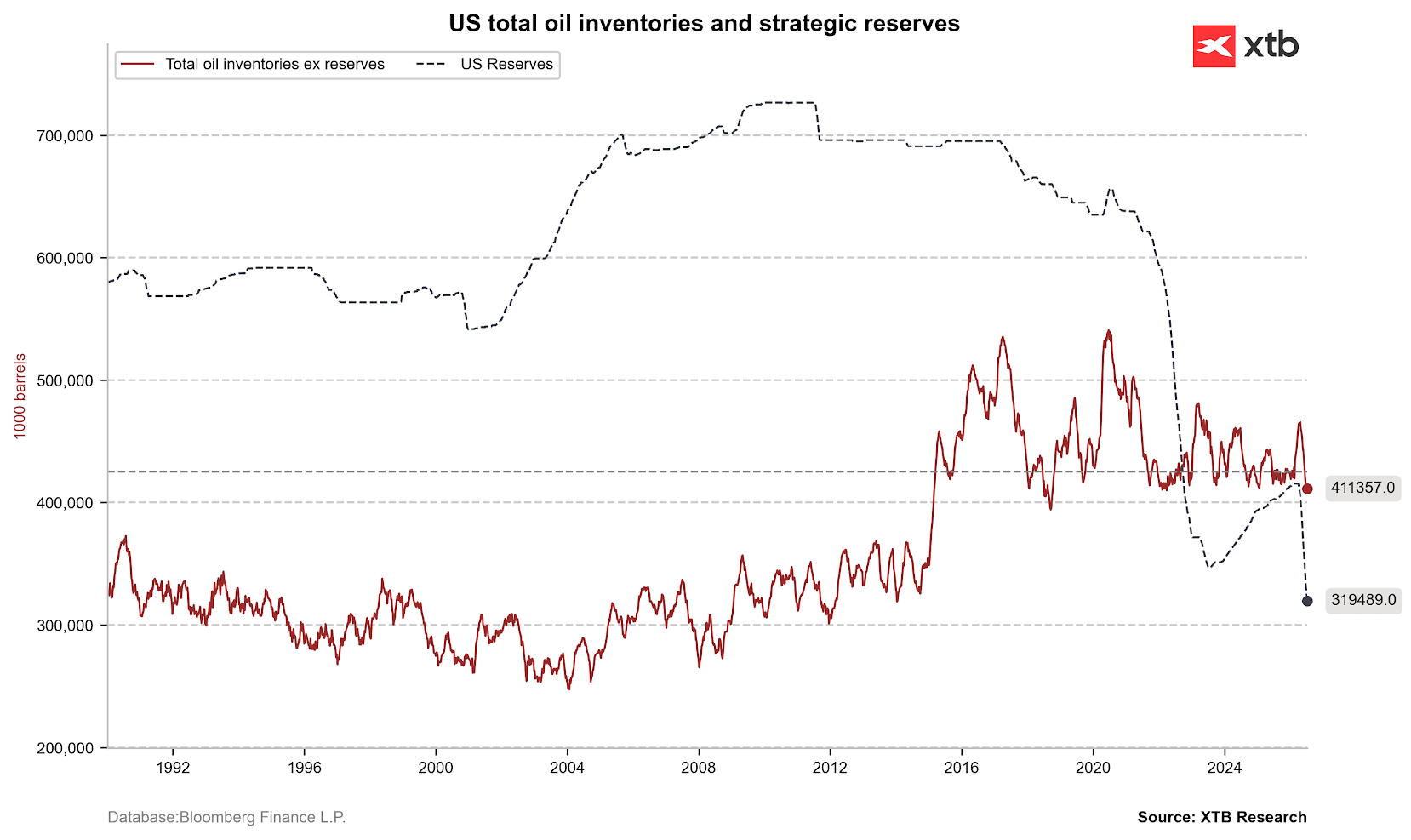

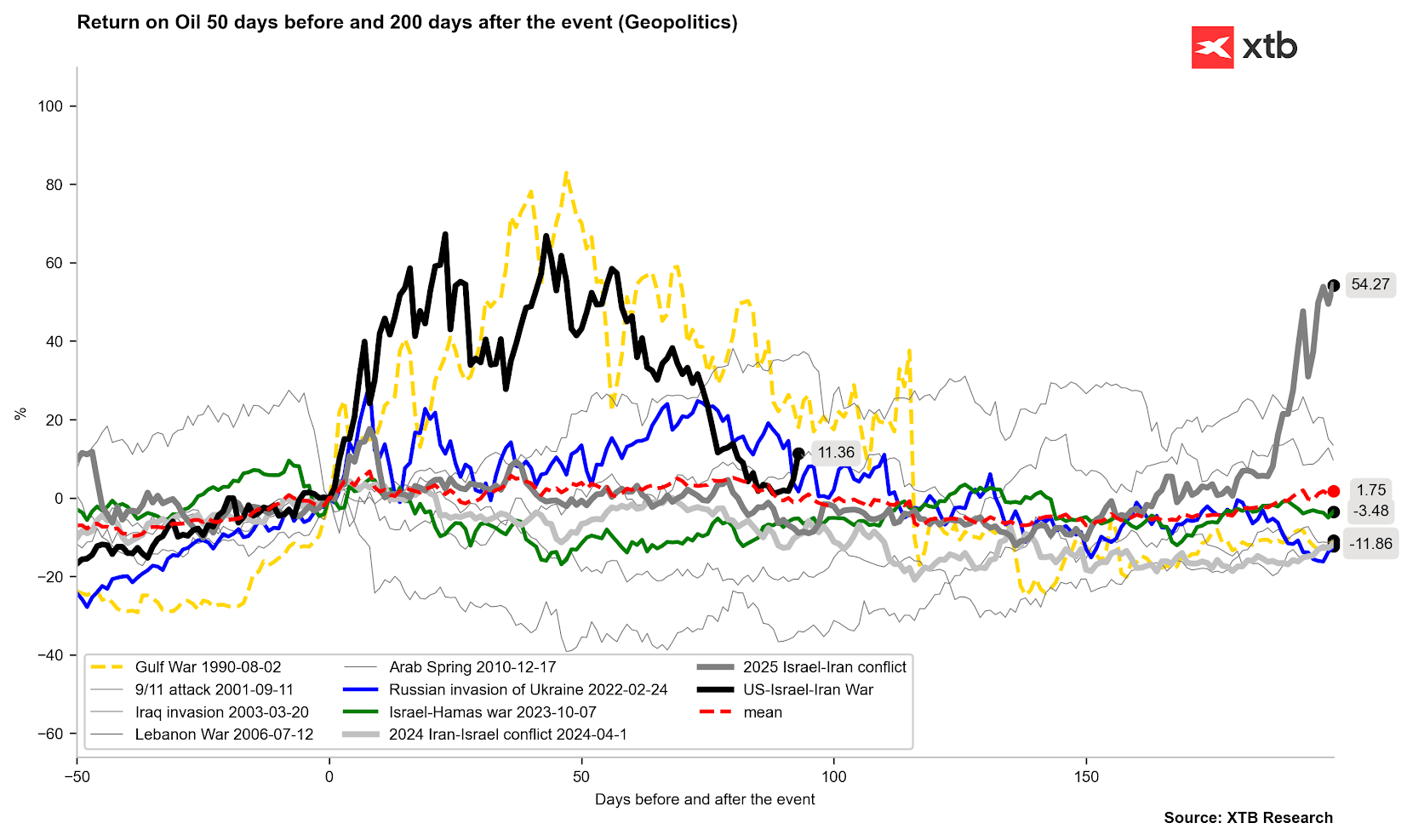

On one hand, it looks like a return to upward pressure in the short term. Trump is escalating the conflict, and Iran is already threatening a total blockade of the Strait of Hormuz (through which 1/5 of the world's oil flows). To make matters worse, the Americans don't have much room for maneuver, as their strategic reserves (SPR) are currently hitting rock bottom and are the lowest since 1984. Add to that the Russian ban on diesel exports and we have a market recipe for a return to higher prices, although at the same time, as history indicates, we should have long passed the peaks resulting from the conflict.

Although commercial inventories rebounded slightly, strategic reserves dived deep to a level below 320 million barrels. Source: Bloomberg Finance LP, XTB

Although commercial inventories rebounded slightly, strategic reserves dived deep to a level below 320 million barrels. Source: Bloomberg Finance LP, XTB

As history shows in 1990 and 2022, increases occur even 4 months after the start of escalation, but the amplitude of changes clearly decreases. Source: Bloomberg Finance LP, XTB

As history shows in 1990 and 2022, increases occur even 4 months after the start of escalation, but the amplitude of changes clearly decreases. Source: Bloomberg Finance LP, XTB

On the other hand, in the longer term, Trump wants to flood the market with oil. The US is producing and exporting fuels at record levels. The President is betting that American overproduction will eventually suppress prices.

If Trump actually decides on an attack and naval blockade, and Iran again closes the Strait of Hormuz, we face a return of prices to the range of 90-100 USD per barrel. However, if he lets up on today's attacks and other politicians announce a return to negotiations, the price of a barrel of Brent could quickly return to around 75 USD.

Additionally, we observe a rebound in the US100. Media reports indicate that China is to allow smaller companies to purchase H200 chips from Nvidia.

France Challenges Palantir, Market Reacts.

Morning Wrap: US halt to attacks balanced by semiconductor sector declines (28.07.2026)

Oil Slides Ahead of the Weekend!

BREAKING: Eurozone recovery? Positive PMI data tempered by high oil and gas prices

The content of this report has been created by XTB S.A., with its registered office in Warsaw, at Prosta 67, 00-838 Warsaw, Poland, (KRS number 0000217580) and supervised by Polish Supervision Authority ( No. DDM-M-4021-57-1/2005). This material is a marketing communication within the meaning of Art. 24 (3) of Directive 2014/65/EU of the European Parliament and of the Council of 15 May 2014 on markets in financial instruments and amending Directive 2002/92/EC and Directive 2011/61/EU (MiFID II). Marketing communication is not an investment recommendation or information recommending or suggesting an investment strategy within the meaning of Regulation (EU) No 596/2014 of the European Parliament and of the Council of 16 April 2014 on market abuse (market abuse regulation) and repealing Directive 2003/6/EC of the European Parliament and of the Council and Commission Directives 2003/124/EC, 2003/125/EC and 2004/72/EC and Commission Delegated Regulation (EU) 2016/958 of 9 March 2016 supplementing Regulation (EU) No 596/2014 of the European Parliament and of the Council with regard to regulatory technical standards for the technical arrangements for objective presentation of investment recommendations or other information recommending or suggesting an investment strategy and for disclosure of particular interests or indications of conflicts of interest or any other advice, including in the area of investment advisory, within the meaning of the Trading in Financial Instruments Act of 29 July 2005 (i.e. Journal of Laws 2019, item 875, as amended). The marketing communication is prepared with the highest diligence, objectivity, presents the facts known to the author on the date of preparation and is devoid of any evaluation elements. The marketing communication is prepared without considering the client’s needs, his individual financial situation and does not present any investment strategy in any way. The marketing communication does not constitute an offer of sale, offering, subscription, invitation to purchase, advertisement or promotion of any financial instruments. XTB S.A. is not liable for any client’s actions or omissions, in particular for the acquisition or disposal of financial instruments, undertaken on the basis of the information contained in this marketing communication. In the event that the marketing communication contains any information about any results regarding the financial instruments indicated therein, these do not constitute any guarantee or forecast regarding the future results.