Inflation surprised to the upside in March when it came out at 2.6% y/y but the markets ignored the data amid soothing comments from the FOMC. This time the market consensus is already at 3.6%. What if actual inflation is even higher? To what extend can the Fed keep ignoring it?

The narrative from the Fed is simple – inflation spike is transitory and is mainly a result of very low level from a year ago. Indeed a spike of inflation in March was driven mainly by fuel costs – 0.7pp in transport alone (so without this, inflation would be 1.9%) and this will get much worse today as fuels lowered inflation in April 2020 by 1.2pp!

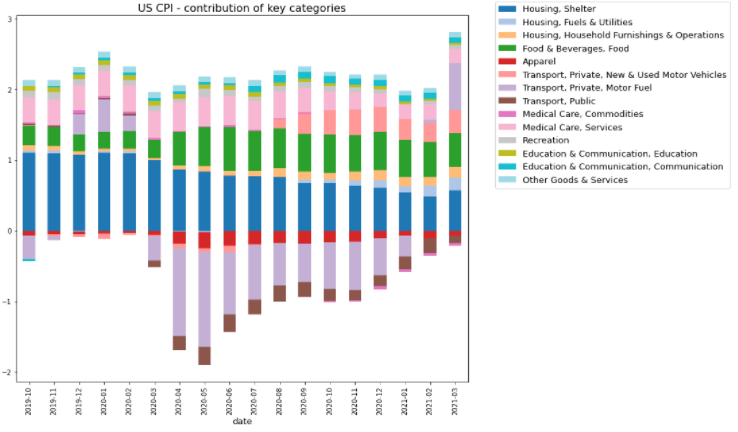

Pick up of inflation in March was mainly a result of higher fuel prices while other categories will tell us more on the seriousness of the inflation pressure. Source: Macrobond, XTB Research

Pick up of inflation in March was mainly a result of higher fuel prices while other categories will tell us more on the seriousness of the inflation pressure. Source: Macrobond, XTB Research

The question is, to what extend will other categories contribute? In March there were no clear signs of a broad inflation pressure. Used cars was the only category outside fuels that saw outsized contribution (which will be probably much higher today). This broad inflation needs to be seen before the Fed actually reacts in any way.

Market reaction is another thing. If the Fed was officially worried about inflation, higher reading would have obvious ramifications. But because the Fed maintains it’s transitory, inflation would need to be probably much above expectations (perhaps above 4%) to spook the markets.

US100 has actually stabilized after a sell-off. This is the market that can react the most directly to the CPI release. Source: XTB Trading Platform

US100 has actually stabilized after a sell-off. This is the market that can react the most directly to the CPI release. Source: XTB Trading Platform

Daily summary: Dollar rout after NFP, Gold back on the rise

Three markets to watch next week (07.08.2026)

The dollar sinks after labor market data💲📉

US OPEN: Shallow rebound in the shadow of a weak labor market

The content of this report has been created by XTB S.A., with its registered office in Warsaw, at Prosta 67, 00-838 Warsaw, Poland, (KRS number 0000217580) and supervised by Polish Supervision Authority ( No. DDM-M-4021-57-1/2005). This material is a marketing communication within the meaning of Art. 24 (3) of Directive 2014/65/EU of the European Parliament and of the Council of 15 May 2014 on markets in financial instruments and amending Directive 2002/92/EC and Directive 2011/61/EU (MiFID II). Marketing communication is not an investment recommendation or information recommending or suggesting an investment strategy within the meaning of Regulation (EU) No 596/2014 of the European Parliament and of the Council of 16 April 2014 on market abuse (market abuse regulation) and repealing Directive 2003/6/EC of the European Parliament and of the Council and Commission Directives 2003/124/EC, 2003/125/EC and 2004/72/EC and Commission Delegated Regulation (EU) 2016/958 of 9 March 2016 supplementing Regulation (EU) No 596/2014 of the European Parliament and of the Council with regard to regulatory technical standards for the technical arrangements for objective presentation of investment recommendations or other information recommending or suggesting an investment strategy and for disclosure of particular interests or indications of conflicts of interest or any other advice, including in the area of investment advisory, within the meaning of the Trading in Financial Instruments Act of 29 July 2005 (i.e. Journal of Laws 2019, item 875, as amended). The marketing communication is prepared with the highest diligence, objectivity, presents the facts known to the author on the date of preparation and is devoid of any evaluation elements. The marketing communication is prepared without considering the client’s needs, his individual financial situation and does not present any investment strategy in any way. The marketing communication does not constitute an offer of sale, offering, subscription, invitation to purchase, advertisement or promotion of any financial instruments. XTB S.A. is not liable for any client’s actions or omissions, in particular for the acquisition or disposal of financial instruments, undertaken on the basis of the information contained in this marketing communication. In the event that the marketing communication contains any information about any results regarding the financial instruments indicated therein, these do not constitute any guarantee or forecast regarding the future results.