The Wall Street session started on a positive note, although futures are erasing almost all of their earlier gains. Today, we observed a new record high on the US500 at 7,570 points, while the US100 reached nearly 30,400 points. Currently, futures remain slightly in the green a dozen or so minutes after the session opening, although earlier gains ranged between 0.3-0.6%.

Investors continue to be driven not only by the unrelenting euphoria surrounding artificial intelligence but also by a sharp plunge in the energy commodities market. Today, however, it is mainly the latter factor boosting sentiment, as we are seeing a slight correction in the tech sector.

Crude oil prices are experiencing a deep decline amid persistent hopes for peace in the Middle East. A barrel of Brent crude is falling by 3.4% to around $93, while US WTI crude is losing slightly more, over 4%, dropping below $90. This is a direct reaction to reports of a working agreement between Washington and Tehran to restore normal shipping traffic through the strategic Strait of Hormuz. According to Iranian public television, the flow of ships through the strait would return to normal within 1 month of its opening. Currently, only a few ships a day pass through the strait, although more and more supertankers have been passing through since mid-May.

It is worth noting that fading concerns over a further sharp rise in inflation have driven bond yields lower. The yield on 10-year US Treasury bonds fell to a level slightly above 4.47%.

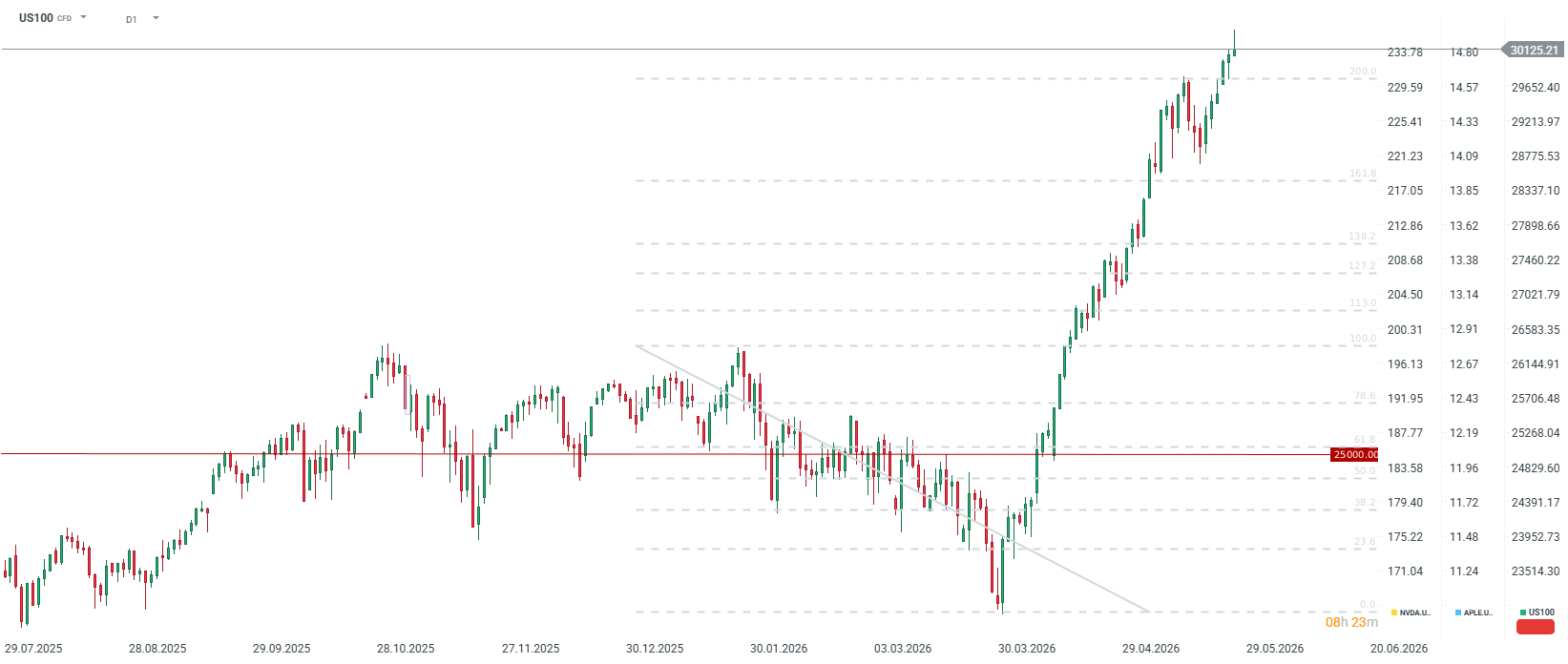

Technical Look at US100 (Nasdaq 100)

From the opening minutes of trading, the Nasdaq 100 index improved upon its all-time highs, but a slight pullback occurred later. Earlier, the US100 contract had reached levels of 30,377 points, and it is currently stabilizing just above 30,000 points. From a technical perspective, the market is in a strong uptrend, completely ignoring signals of potential overbought conditions. It is worth noting that despite extremely high nominal levels or a current P/E ratio around 40, the Forward P/E ratio sits around 26-27, significantly lower than it was at the turn of 2025 and 2026.

The US100 broke above the 200.0% retracement of the last downward wave a few days ago and is already gaining over 30% from its local low at the end of March. Today marks potentially the 6th consecutive winning session on the Nasdaq.

US100 limits its gains after the session start. If the day ends with such a large wick, it could be a dangerous signal for the rest of the week. Source: xStation5

US100 limits its gains after the session start. If the day ends with such a large wick, it could be a dangerous signal for the rest of the week. Source: xStation5

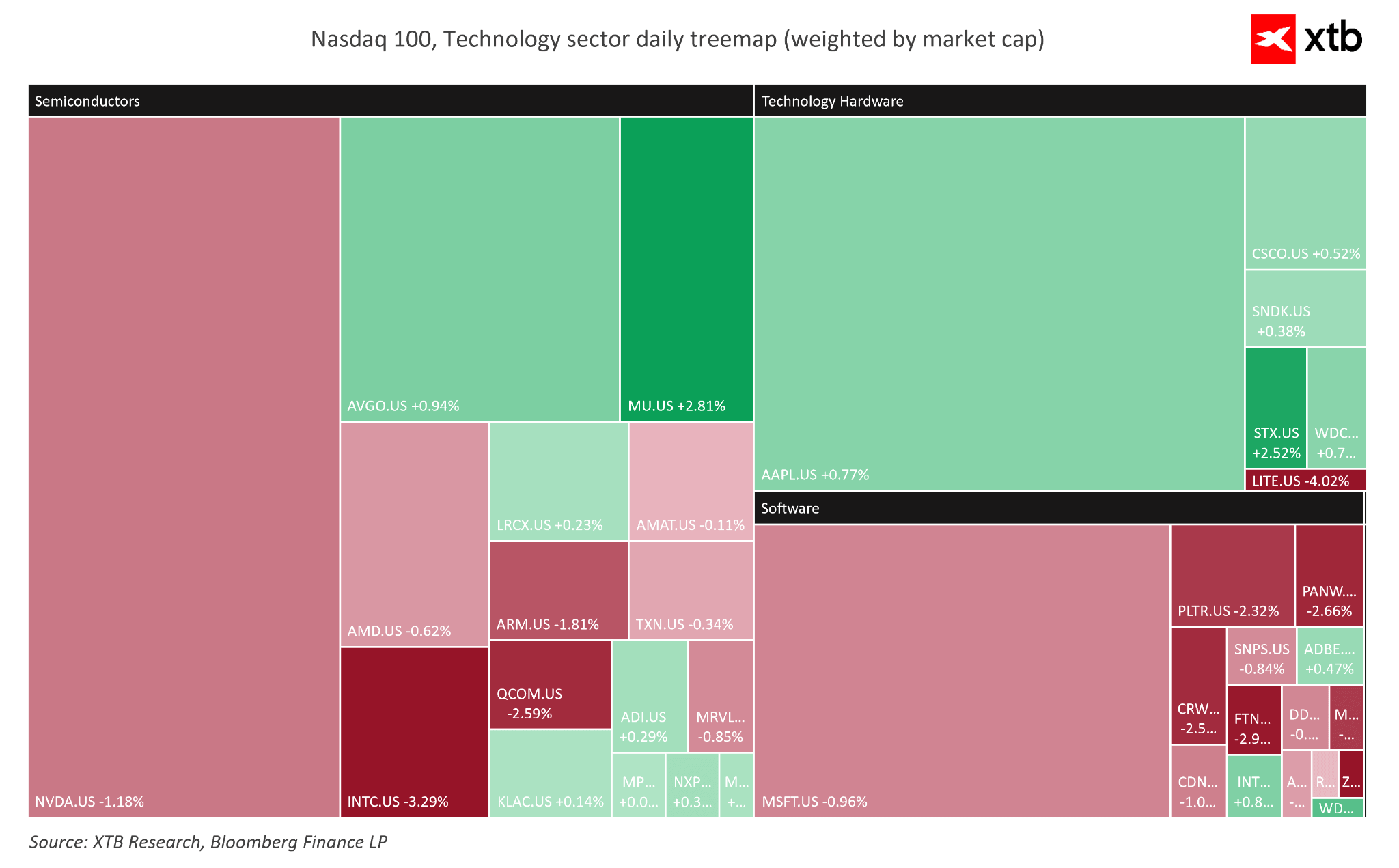

A Look at Sectors

Sector-wise, semiconductor manufacturers remain the main driving forces. The market capitalization of the leader, Nvidia, has consolidated at an astronomical level of $5.20 trillion, while Alphabet and Apple control $4.69 trillion and $4.53 trillion of market value, respectively. Crucially, today goes down in history as two memory giants South Korea's SK Hynix ($1.06–$1.08 trillion) and America's Micron Technology ($1.01 trillion) enter the elite club of companies with valuations exceeding $1 trillion. The second hottest trading area today is the space and satellite sector. Investors are buying up shares of companies linked to this technology in bulk, in response to incoming reports about plans for Elon Musk's SpaceX to go public, which promises to be the largest initial public offering (IPO) in capital markets history.

Semiconductor companies are giving back some of their previous gains. Source: Bloomberg Finance LP, XTB

Semiconductor companies are giving back some of their previous gains. Source: Bloomberg Finance LP, XTB

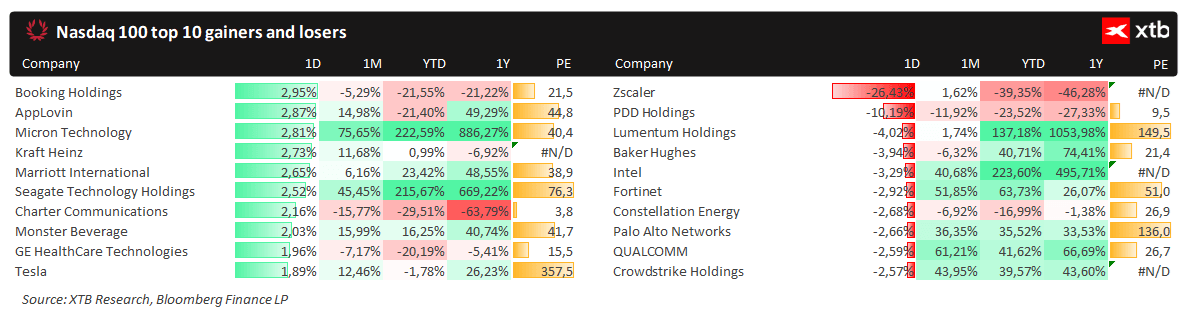

Among the top-performing companies, we don't see big names today apart from Micron and Tesla, which, however, pared their gains after the opening minutes of trading. Source: Bloomberg Finance LP, XTB

Among the top-performing companies, we don't see big names today apart from Micron and Tesla, which, however, pared their gains after the opening minutes of trading. Source: Bloomberg Finance LP, XTB

Corporate News

-

Micron Technology (MU): Shares of the memory manufacturer are gaining around 5-6% after the open. This move dynamically extends yesterday's impressive 19% surge, which allowed the company to cross the $1 trillion market cap barrier for the first time.

-

ByteDance: The Chinese tech giant and owner of the TikTok platform intends to spend a staggering $70 billion this year on the development of artificial intelligence infrastructure (compared to $25 billion last year). The aggressive plan aims to dominate the domestic AI market and directly challenge American competition abroad.

-

Zscaler (ZS): Shares of the cybersecurity company are experiencing a painful reality check today, losing 25% of their value. The sell-off is a direct consequence of conservative revenue forecasts for the next period, which quickly translated into a wave of market rating downgrades.

-

Tesla (TSLA): The stock price is rising by 2%, clearly outperforming the rest of the Magnificent Seven group. The optimism is backed by excellent April data on new car registrations in Europe and speculation regarding a potential merger with SpaceX.

-

Bath & Body Works (BBWI): The retail chain's shares are up by nearly 10%. The company's quarterly financial results turned out to be significantly higher than the analyst consensus, and the board decided to maintain its existing guidance for the full fiscal year.

-

Verra Mobility (VRRM): Is experiencing a massive crash, losing as much as 68% of its valuation. The drastic drop in stock prices was triggered by the loss of a contract with a key partner, Avis car rental, which prompted immediate rating cuts from leading investment banks.

Daily Summary - The market starts to doubt rate hikes after Warsh, but Trump destroys the rebound

US OPEN: Wall Street Holds Its Breath Ahead of Fed Decision and Tech Giant Earnings

SK Hynix earnings: Did market over-sold?

France Challenges Palantir, Market Reacts.

The content of this report has been created by XTB S.A., with its registered office in Warsaw, at Prosta 67, 00-838 Warsaw, Poland, (KRS number 0000217580) and supervised by Polish Supervision Authority ( No. DDM-M-4021-57-1/2005). This material is a marketing communication within the meaning of Art. 24 (3) of Directive 2014/65/EU of the European Parliament and of the Council of 15 May 2014 on markets in financial instruments and amending Directive 2002/92/EC and Directive 2011/61/EU (MiFID II). Marketing communication is not an investment recommendation or information recommending or suggesting an investment strategy within the meaning of Regulation (EU) No 596/2014 of the European Parliament and of the Council of 16 April 2014 on market abuse (market abuse regulation) and repealing Directive 2003/6/EC of the European Parliament and of the Council and Commission Directives 2003/124/EC, 2003/125/EC and 2004/72/EC and Commission Delegated Regulation (EU) 2016/958 of 9 March 2016 supplementing Regulation (EU) No 596/2014 of the European Parliament and of the Council with regard to regulatory technical standards for the technical arrangements for objective presentation of investment recommendations or other information recommending or suggesting an investment strategy and for disclosure of particular interests or indications of conflicts of interest or any other advice, including in the area of investment advisory, within the meaning of the Trading in Financial Instruments Act of 29 July 2005 (i.e. Journal of Laws 2019, item 875, as amended). The marketing communication is prepared with the highest diligence, objectivity, presents the facts known to the author on the date of preparation and is devoid of any evaluation elements. The marketing communication is prepared without considering the client’s needs, his individual financial situation and does not present any investment strategy in any way. The marketing communication does not constitute an offer of sale, offering, subscription, invitation to purchase, advertisement or promotion of any financial instruments. XTB S.A. is not liable for any client’s actions or omissions, in particular for the acquisition or disposal of financial instruments, undertaken on the basis of the information contained in this marketing communication. In the event that the marketing communication contains any information about any results regarding the financial instruments indicated therein, these do not constitute any guarantee or forecast regarding the future results.