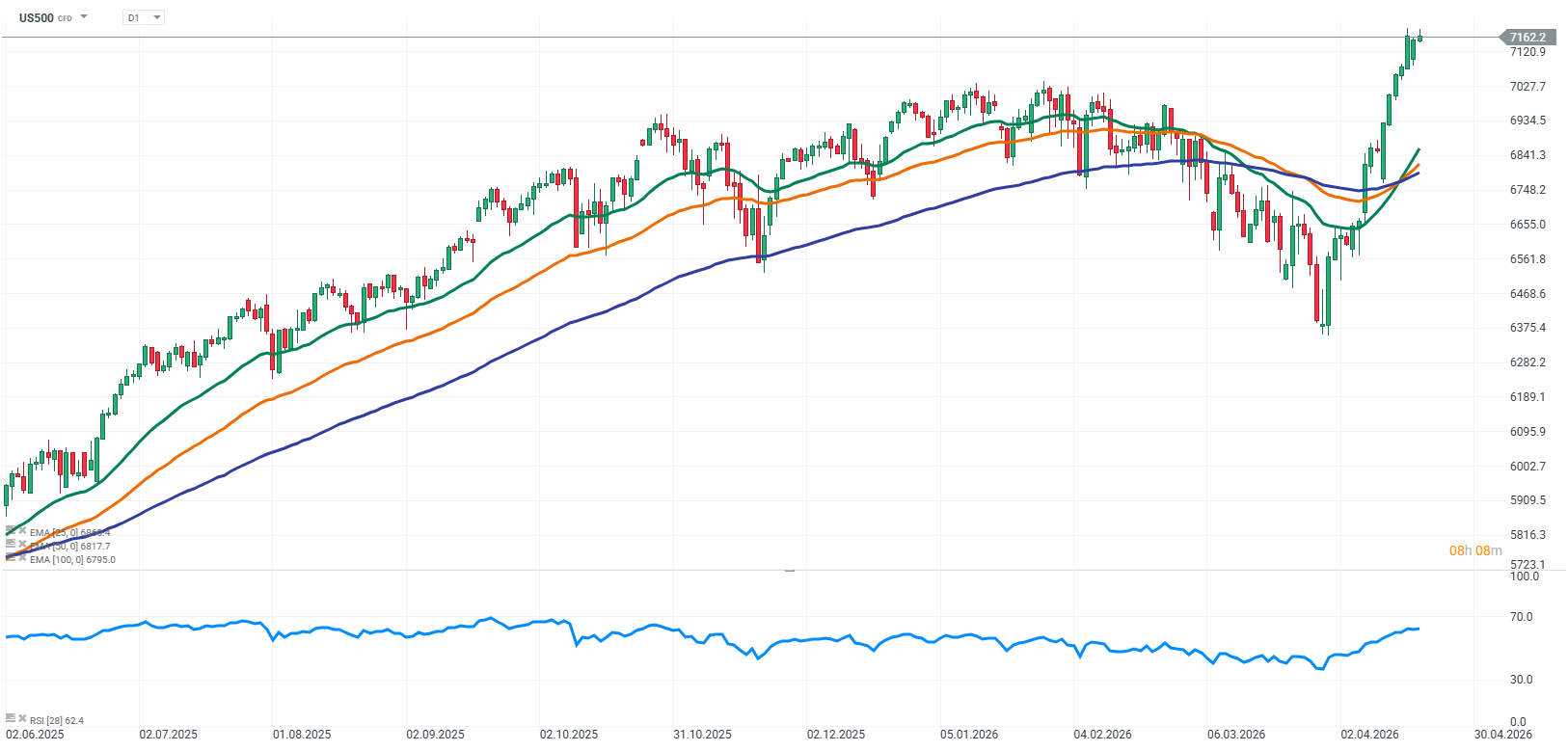

Today’s picture on Wall Street is shaped by the simultaneous impact of two key drivers: stronger-than-expected U.S. economic data and a shifting geopolitical backdrop, which in the short term is clearly influencing investors’ risk appetite. The market is trying to assess both the real strength of the U.S. consumer and the scale of potential risks stemming from tensions in the Middle East, resulting in elevated volatility but also support for equity indices.

On the macroeconomic side, the most important data point is U.S. retail sales, which came in significantly above expectations. Part of this increase was driven by higher gasoline prices, which lift nominal sales figures, but there was also visible strength in the underlying reading excluding the most volatile components. This suggests that the consumer remains active despite ongoing cost pressures and high interest rates. The market interprets this as a sign that the U.S. economy is not heading into a sharp slowdown, but rather into a more controlled cooling of activity. In this environment, overall sentiment improves and risk appetite in equities increases.

An additional factor reinforcing this picture is the impact of energy prices on economic data. Higher fuel costs, driven by geopolitical tensions, directly inflate nominal retail sales figures while partially distorting the view of underlying consumer strength. As a result, the data looks very solid on the headline level, but its structure requires more cautious interpretation, as it does not fully reflect the real dynamics of spending.

The second key pillar of today’s move is geopolitics, where signals of a possible resumption of talks between the United States and Iran are emerging, alongside persistent uncertainty and conflicting messages from the region. Even the prospect of dialogue, however uncertain, tends to calm markets as it reduces fears of further escalation and potential disruptions in energy markets. This in turn lowers the risk premium and supports flows into risk assets.

As a result, we are seeing a combination of relatively strong U.S. economic data and a temporary improvement in geopolitical sentiment. This mix naturally supports equity indices and fuels gains, although it remains a conditional environment highly sensitive to shifts in both macro data and political developments.

Source: xStation5

U.S. S&P 500 futures (US500) are posting slight gains today, driven by surprisingly strong retail sales data. The figures show that U.S. consumer demand remains resilient, easing concerns about a sharp deterioration in economic momentum and supporting equity valuations. Additionally, investors are reacting positively to signals suggesting a potential resumption of U.S.–Iran talks, which temporarily ease geopolitical tensions and improve overall market sentiment.

Source: xStation5

Company News

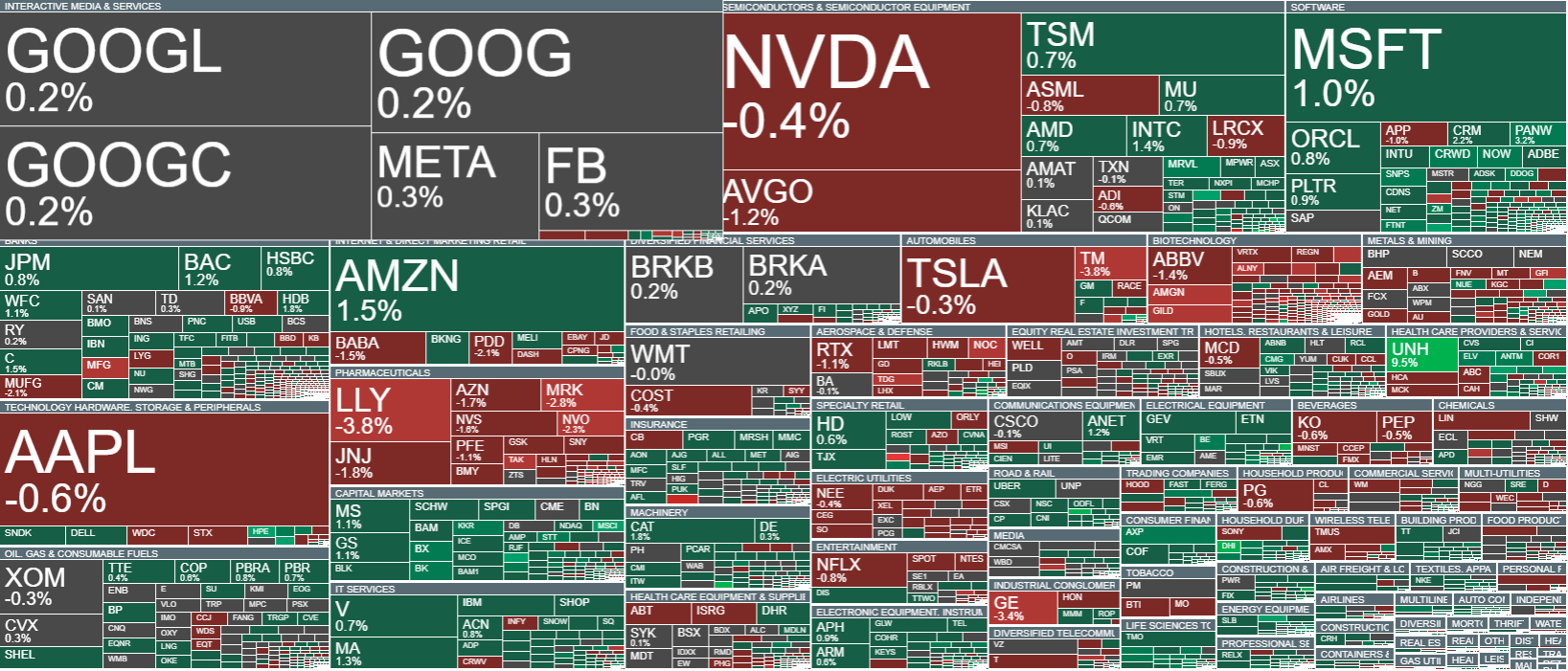

UnitedHealth (UNH.US) significantly surprised the market with better-than-expected Q1 2026 results and raised its full-year earnings guidance, signaling continued strong operational performance. In addition, a $2 billion share buyback program further strengthened the positive reaction and supported the stock price. The market interprets this as confirmation that the company remains one of the most stable leaders in the healthcare sector.

Amazon (AMZN.US) is rising after announcing a major acceleration in artificial intelligence through an expanded partnership with Anthropic and a significant investment package. The partnership strengthens AWS’s position as a core infrastructure provider for AI development, while the scale of planned spending and computing capacity suggests very strong long-term demand for Amazon’s services. The market views this as another step in reinforcing Amazon’s leadership in the global AI race.

RTX (RTX.US) is higher after delivering very strong Q1 results that beat expectations on both revenue and earnings. The company also raised parts of its full-year outlook, which the market interpreted as confirmation of sustained strong demand in the defense sector and a gradual recovery in commercial aviation. This continues to support the broader defense industry, where order volumes remain high and contract inflows are stable.

Northrop Grumman (NOC.US), despite better-than-expected results, came under mild selling pressure as investors focused on full-year guidance that did not provide a clear upside surprise. While the company delivered solid revenue and earnings, the lack of a stronger upward revision to the outlook limited market enthusiasm. At the same time, the sector fundamentals remain strong, supported by high defense budgets and a robust pipeline of orders, which continues to underpin the long-term investment case.

Apple (AAPL.US) announced a major leadership change, with Tim Cook set to step down as CEO and transition to the role of chairman of the board, while John Ternus will take over as CEO. The news has triggered a mixed reaction among investors.

Daily Summary: Wall Street Regains Ground; Another Intervention in the Yen Market❓

Three Markets to Watch Next Week (July 31, 2026)

Market Wrap: European equities at 3-week highs! Apple dips in US premarket!

Euro Area core inflation above estiamtes! EURUSD under key resistance!

The content of this report has been created by XTB S.A., with its registered office in Warsaw, at Prosta 67, 00-838 Warsaw, Poland, (KRS number 0000217580) and supervised by Polish Supervision Authority ( No. DDM-M-4021-57-1/2005). This material is a marketing communication within the meaning of Art. 24 (3) of Directive 2014/65/EU of the European Parliament and of the Council of 15 May 2014 on markets in financial instruments and amending Directive 2002/92/EC and Directive 2011/61/EU (MiFID II). Marketing communication is not an investment recommendation or information recommending or suggesting an investment strategy within the meaning of Regulation (EU) No 596/2014 of the European Parliament and of the Council of 16 April 2014 on market abuse (market abuse regulation) and repealing Directive 2003/6/EC of the European Parliament and of the Council and Commission Directives 2003/124/EC, 2003/125/EC and 2004/72/EC and Commission Delegated Regulation (EU) 2016/958 of 9 March 2016 supplementing Regulation (EU) No 596/2014 of the European Parliament and of the Council with regard to regulatory technical standards for the technical arrangements for objective presentation of investment recommendations or other information recommending or suggesting an investment strategy and for disclosure of particular interests or indications of conflicts of interest or any other advice, including in the area of investment advisory, within the meaning of the Trading in Financial Instruments Act of 29 July 2005 (i.e. Journal of Laws 2019, item 875, as amended). The marketing communication is prepared with the highest diligence, objectivity, presents the facts known to the author on the date of preparation and is devoid of any evaluation elements. The marketing communication is prepared without considering the client’s needs, his individual financial situation and does not present any investment strategy in any way. The marketing communication does not constitute an offer of sale, offering, subscription, invitation to purchase, advertisement or promotion of any financial instruments. XTB S.A. is not liable for any client’s actions or omissions, in particular for the acquisition or disposal of financial instruments, undertaken on the basis of the information contained in this marketing communication. In the event that the marketing communication contains any information about any results regarding the financial instruments indicated therein, these do not constitute any guarantee or forecast regarding the future results.