U.S. stock indices are opening today's session with sharp declines, giving back some of last week's record highs. Futures on the Dow Jones Industrial Average (US30) are down about 0.9%, the S&P 500 (US500) is down 0.8%, and the tech-heavy Nasdaq-100 (US100) is also down 0.8%. The Russell 2000 (US2000) index of smaller companies is showing similar weakness, down about 0.8% at the start of trading. Investors are rushing to reduce their risk appetite, and a significant uncertainty premium is once again being priced in.

The main factor driving the market today is the rapid escalation of tensions in the Middle East. The United States seized and fired upon an Iranian cargo ship in the Gulf of Oman, and in response, Iran once again completely blocked the Strait of Hormuz, which is crucial for trade. The approaching end of the ceasefire has drastically reduced market hopes for successful peace negotiations in Islamabad. As a result, we are seeing a massive rally in the energy sector, where WTI and Brent crude oil prices have jumped by as much as 6-7% at times, which further dampens market sentiment and fuels fears of prolonged inflation.

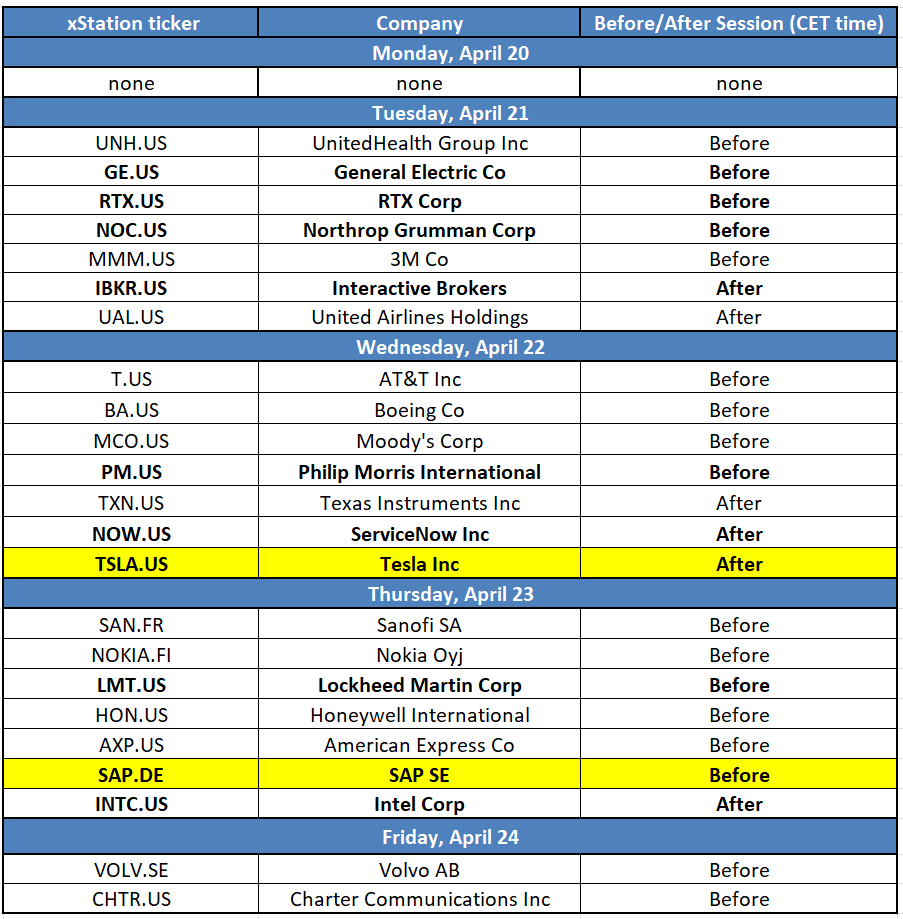

Today’s macroeconomic calendar for the United States is virtually empty, and Fed officials have already entered the media blackout period ahead of the interest rate decision scheduled for April 29. Market attention is therefore focused on the upcoming events this week. Investors are primarily awaiting tomorrow’s March retail sales data, which is expected to show a solid rebound driven by higher fuel prices, as well as the key hearing of Kevin Warsh, the nominee for the new chair of the Federal Reserve. Below is the calendar of quarterly earnings releases for major companies this week. Source: XTB

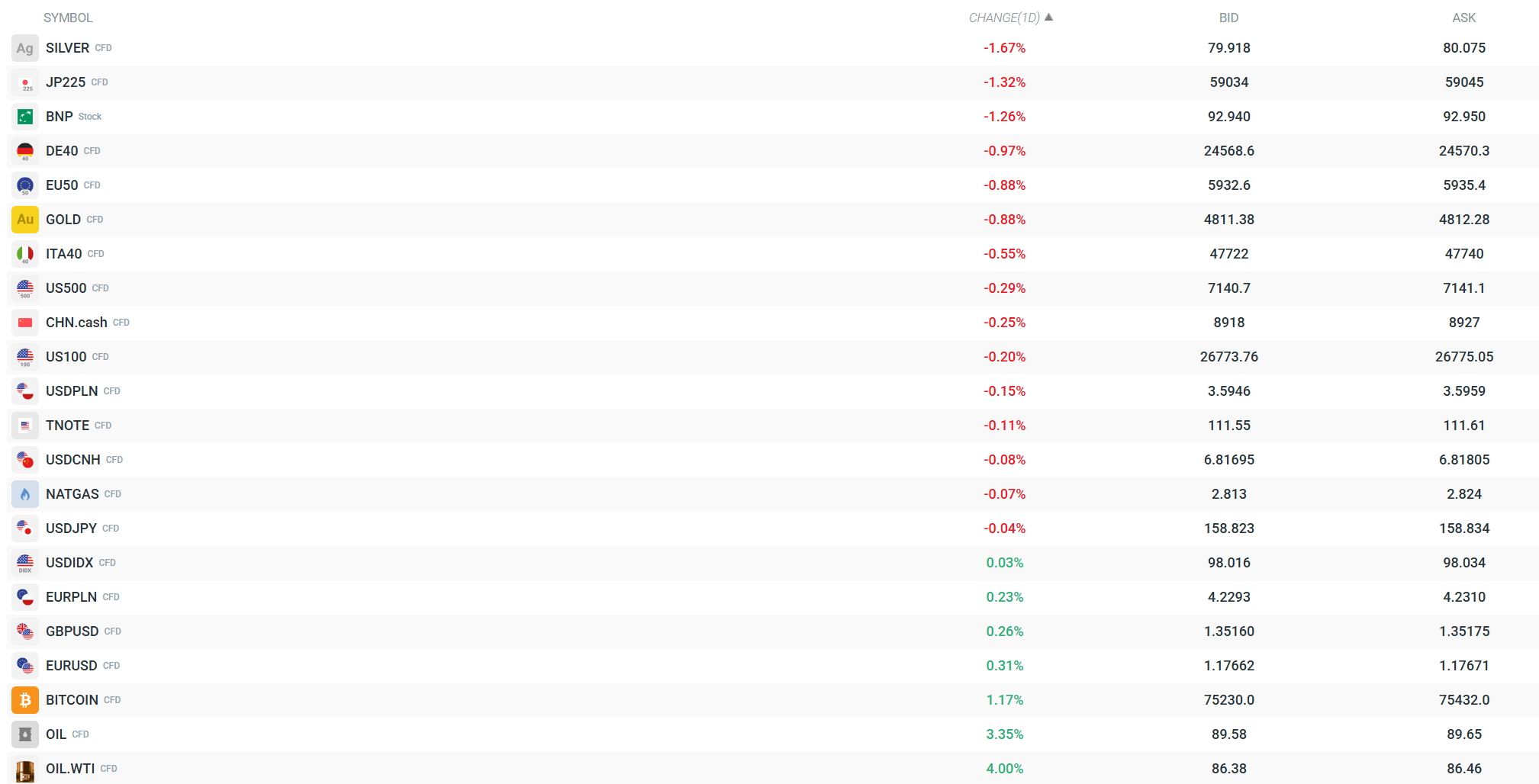

Volatility is currently evident in key markets. Source: xStation

Key company information:

- American Airlines (AAL) – The airline’s shares are down about 3% in pre-market trading. The company has officially dismissed speculation about a potential mega-merger with United Airlines, arguing that the merger would be harmful to competition and consumers. Such a deal would create the world’s largest airline, but analysts have long pointed to the slim chances of it being approved by antitrust authorities. The airline sector is under additional pressure today due to a sharp rise in fuel prices caused by tensions in the Middle East.

- Marvell Technology (MRVL) – Shares of this semiconductor manufacturer are up an impressive 7% at the opening bell. The rally is being driven by media reports that the company is in advanced talks with Google (Alphabet). The collaboration is said to involve the design of two new, highly specialized chips intended for more efficient handling of artificial intelligence models. The prospect of strengthening technological ties with such a massive giant firmly positions the company in the lucrative AI market, which explains today’s euphoria.

- TopBuild (BLD) – Shares of the distributor and installer of insulation materials are surging by over 17%. The sharp volatility is a result of news that the company is being acquired by the QXO conglomerate for $17 billion. As part of this merger, TopBuild shareholders will have the option to receive either cash ($505 per share) or QXO shares, representing a premium of over 23% relative to Friday’s closing price. The deal will immediately boost the new group’s profits, creating the second-largest distributor of building materials in North America.

- AST SpaceMobile (ASTS) – Shares of this innovative telecommunications company plummeted by 14–15% this morning. The reason for this sell-off is the failed weekend launch of Blue Origin’s New Glenn rocket, which placed the AST satellite into the wrong, too-low orbit. The satellite will be unable to use its thrusters to correct its course and will soon burn up in the atmosphere. Although management is reassuring investors that the cost of the satellite will be covered by an insurance policy, this painful incident is creating uncertainty regarding the timeline for future commercial deployments.

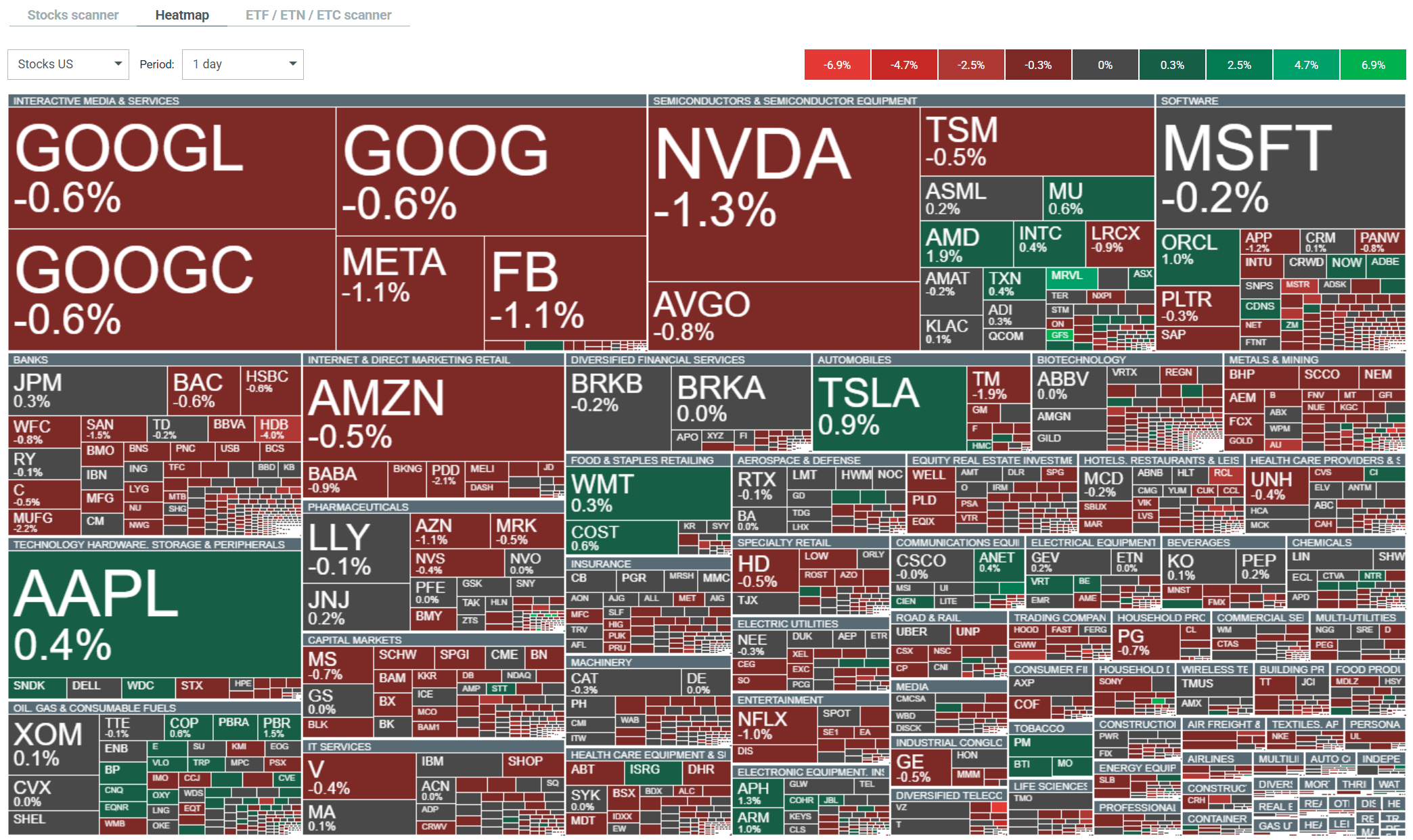

Sectors at the start of the session: Energy shines, tourism falters

During today’s session, we are seeing a clear rotation of capital and extreme performance across different sectors. The energy sector is the clear leader, surging on the back of rapidly rising oil prices, which is boosting the shares of giants such as Exxon Mobil, Chevron, ConocoPhillips, and APA. At the opposite end of the spectrum is the broader travel industry—including primarily airlines and cruise operators (such as Carnival and Royal Caribbean)—which is under intense selling pressure due to concerns about a drastic rise in fuel costs. As risk appetite waned, cyclical companies (including the automotive and banking sectors) and entities linked to the cryptocurrency market also joined the ranks of today’s biggest laggards. Source: xStation

Daily Summary: Wall Street Regains Ground; Another Intervention in the Yen Market❓

Three Markets to Watch Next Week (July 31, 2026)

Market Wrap: European equities at 3-week highs! Apple dips in US premarket!

Euro Area core inflation above estiamtes! EURUSD under key resistance!

The content of this report has been created by XTB S.A., with its registered office in Warsaw, at Prosta 67, 00-838 Warsaw, Poland, (KRS number 0000217580) and supervised by Polish Supervision Authority ( No. DDM-M-4021-57-1/2005). This material is a marketing communication within the meaning of Art. 24 (3) of Directive 2014/65/EU of the European Parliament and of the Council of 15 May 2014 on markets in financial instruments and amending Directive 2002/92/EC and Directive 2011/61/EU (MiFID II). Marketing communication is not an investment recommendation or information recommending or suggesting an investment strategy within the meaning of Regulation (EU) No 596/2014 of the European Parliament and of the Council of 16 April 2014 on market abuse (market abuse regulation) and repealing Directive 2003/6/EC of the European Parliament and of the Council and Commission Directives 2003/124/EC, 2003/125/EC and 2004/72/EC and Commission Delegated Regulation (EU) 2016/958 of 9 March 2016 supplementing Regulation (EU) No 596/2014 of the European Parliament and of the Council with regard to regulatory technical standards for the technical arrangements for objective presentation of investment recommendations or other information recommending or suggesting an investment strategy and for disclosure of particular interests or indications of conflicts of interest or any other advice, including in the area of investment advisory, within the meaning of the Trading in Financial Instruments Act of 29 July 2005 (i.e. Journal of Laws 2019, item 875, as amended). The marketing communication is prepared with the highest diligence, objectivity, presents the facts known to the author on the date of preparation and is devoid of any evaluation elements. The marketing communication is prepared without considering the client’s needs, his individual financial situation and does not present any investment strategy in any way. The marketing communication does not constitute an offer of sale, offering, subscription, invitation to purchase, advertisement or promotion of any financial instruments. XTB S.A. is not liable for any client’s actions or omissions, in particular for the acquisition or disposal of financial instruments, undertaken on the basis of the information contained in this marketing communication. In the event that the marketing communication contains any information about any results regarding the financial instruments indicated therein, these do not constitute any guarantee or forecast regarding the future results.