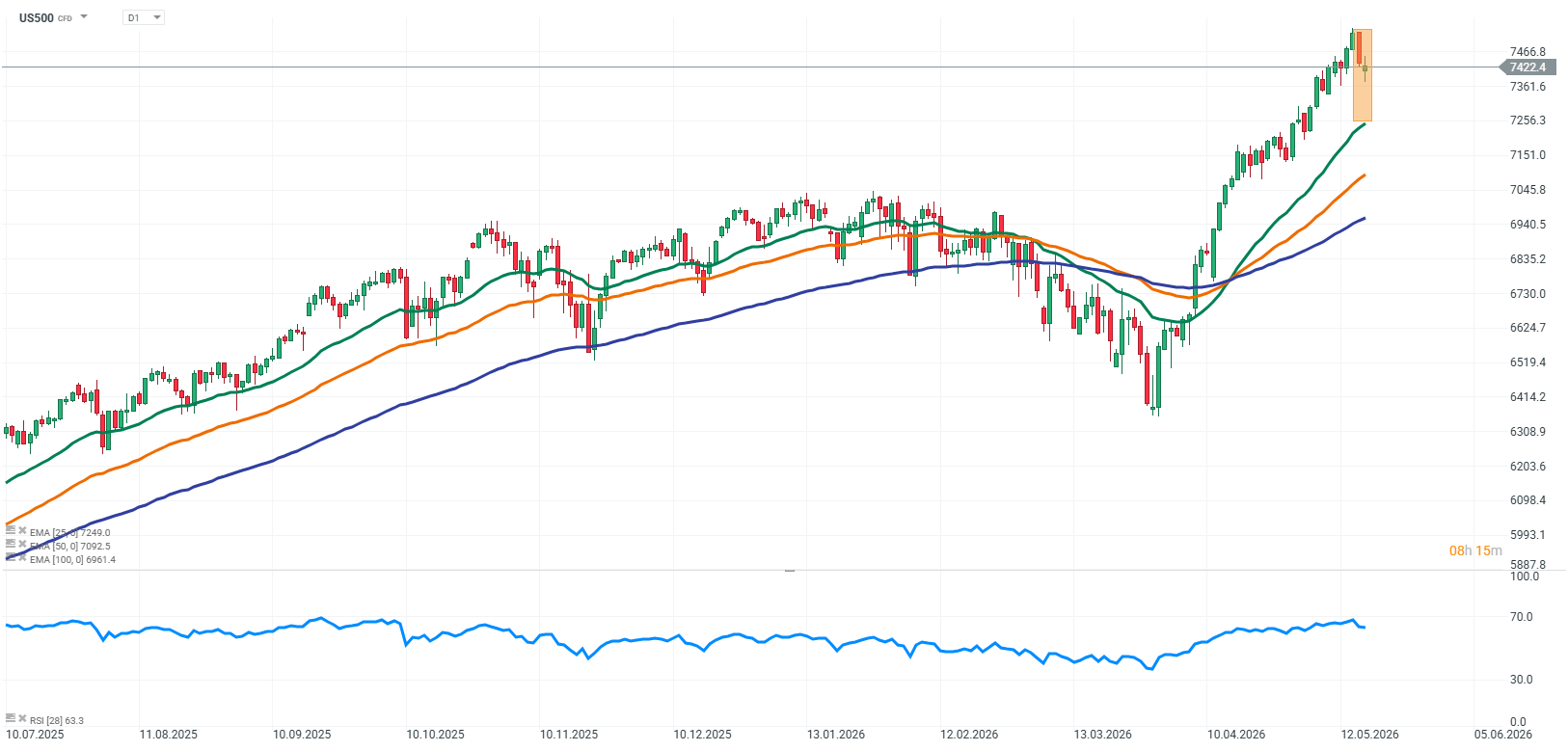

Major U.S. equity indices opened the session with mixed sentiment, while overall market direction remains limited and lacking a clear dominant trend. The Dow Jones Industrial Average is posting slight declines, similar to the S&P 500, while the Nasdaq Composite is hovering around the flat line, indicating the absence of a unified market catalyst across broader equities.

Index moves are relatively small, suggesting a cautious approach from investors and a wait-and-see attitude ahead of fresh signals. Sentiment on Wall Street remains broadly stable despite ongoing macroeconomic and geopolitical uncertainty in the background. The market appears to be operating in a low-visibility environment, where short-term data and capital flows drive intraday volatility but do not materially alter the broader market picture.

Investors have largely already priced in developments following the U.S.–China meeting in Beijing. The summit did not produce any breakthrough agreements that could meaningfully reshape trade or technology relations. Communications from both sides were limited to general statements about continuing dialogue and cautious signals of partial reopening of selected cooperation channels. In practice, the market interpreted this more as the absence of a negative surprise rather than any real progress, which in the current environment is also viewed as a form of stabilization.

Meanwhile, geopolitical tensions related to Iran remain present in the background and continue to reappear in market narratives as a potential source of volatility. Media reports and speculation around possible escalation in U.S. rhetoric periodically weigh on oil prices and broader risk assets. However, at this stage, this is not a factor that consistently drives equity valuations, but rather one that maintains an elevated level of investor caution.

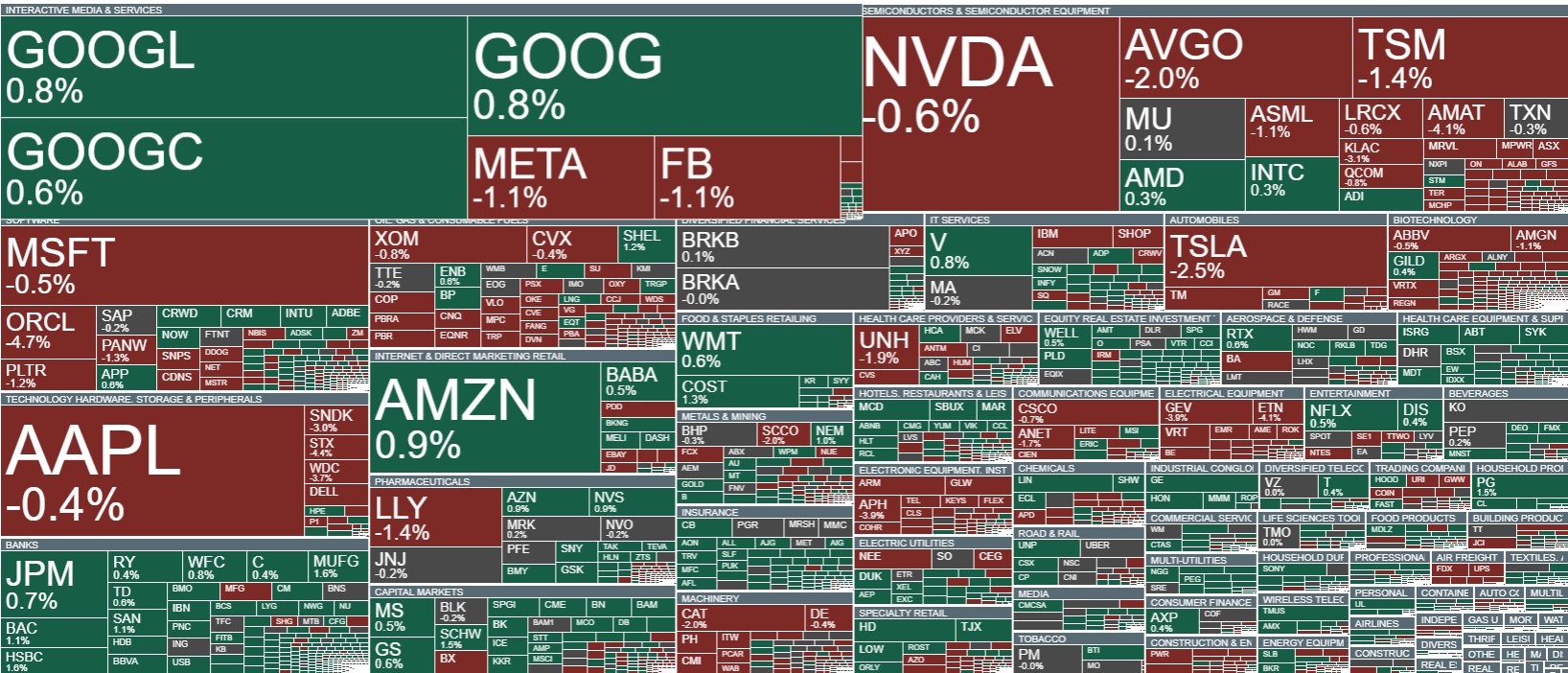

The key pillar supporting market sentiment remains the technology sector, particularly semiconductors. This segment continues to act as the main driver of equity indices, offsetting weaker sentiment in other areas of the market and sustaining the overall bullish narrative. In effect, technology still sets the tone for broader market direction, while other sectors largely adjust to its momentum.

Investors are now focused on NVIDIA, which is set to report quarterly earnings this Wednesday. Expectations remain very high, with the market pricing in not only a clear earnings beat but also continued confirmation of the strength of the artificial intelligence investment cycle and rising demand for computing power. In this context, NVIDIA has effectively become a barometer for the broader AI narrative, which has been one of the key drivers of the technology rally in recent months.

Any disappointment in earnings or guidance could therefore trigger a reaction extending beyond a single stock. In such a scenario, the market could shift into a more defensive mode, with profit-taking spreading across a wider basket of technology names that have recently benefited from strong momentum. Elevated expectations leave limited room for error, meaning even a modest miss could be interpreted as a catalyst for a broader correction.

Source: xStation5

U.S. stock index futures (US500) are trading around the flat line, reflecting clear market caution and a lack of directional conviction at the start of the session. Sentiment remains subdued amid the absence of meaningful progress in U.S.–Iran relations and rising war rhetoric, which continues to increase uncertainty and encourages investors to reduce risk exposure.

Source: xStation5

Company news

Citi has raised price targets for Intel (INTC.US) and AMD (AMD.US), citing a more positive outlook for the CPU market than previously expected. Analysts anticipate stronger demand growth driven by artificial intelligence development and continued expansion of data centers, supporting a constructive view on both companies. At the same time, Intel came into focus after Donald Trump commented that, in earlier discussions regarding U.S. government involvement in the company, he “should have asked for more.”

Arm Holdings (ARM.US) is edging higher at the start of the session despite an ongoing U.S. antitrust investigation. Regulators are examining whether the company is leveraging its dominant position in semiconductor licensing to restrict competition, including limiting access to key licenses or worsening licensing terms. The investigation also considers potential conflicts of interest related to Arm’s expansion into its own chip design activities.

Ryanair (RYAAY.US) reported better-than-expected results, posting a roughly 40% increase in net profit to €2.26 billion and an 11% rise in revenue to €15.5 billion, supported by higher ticket prices and strong travel demand. Passenger numbers increased by 4%, while cost discipline further supported profitability. Despite strong results, the company highlighted ongoing uncertainty related to fuel prices and geopolitical risks.

Daily Summary - Oil gains due to uncertainty, market awaits inflation data

⬆️Oil back above $88

US Open: Nasdaq Seeks Direction 🗽 Hims & Hers Shares React to Earnings

⚫Commodity wrap - Oil, Gold, Natgas, Emiss (11.08.2026)

The content of this report has been created by XTB S.A., with its registered office in Warsaw, at Prosta 67, 00-838 Warsaw, Poland, (KRS number 0000217580) and supervised by Polish Supervision Authority ( No. DDM-M-4021-57-1/2005). This material is a marketing communication within the meaning of Art. 24 (3) of Directive 2014/65/EU of the European Parliament and of the Council of 15 May 2014 on markets in financial instruments and amending Directive 2002/92/EC and Directive 2011/61/EU (MiFID II). Marketing communication is not an investment recommendation or information recommending or suggesting an investment strategy within the meaning of Regulation (EU) No 596/2014 of the European Parliament and of the Council of 16 April 2014 on market abuse (market abuse regulation) and repealing Directive 2003/6/EC of the European Parliament and of the Council and Commission Directives 2003/124/EC, 2003/125/EC and 2004/72/EC and Commission Delegated Regulation (EU) 2016/958 of 9 March 2016 supplementing Regulation (EU) No 596/2014 of the European Parliament and of the Council with regard to regulatory technical standards for the technical arrangements for objective presentation of investment recommendations or other information recommending or suggesting an investment strategy and for disclosure of particular interests or indications of conflicts of interest or any other advice, including in the area of investment advisory, within the meaning of the Trading in Financial Instruments Act of 29 July 2005 (i.e. Journal of Laws 2019, item 875, as amended). The marketing communication is prepared with the highest diligence, objectivity, presents the facts known to the author on the date of preparation and is devoid of any evaluation elements. The marketing communication is prepared without considering the client’s needs, his individual financial situation and does not present any investment strategy in any way. The marketing communication does not constitute an offer of sale, offering, subscription, invitation to purchase, advertisement or promotion of any financial instruments. XTB S.A. is not liable for any client’s actions or omissions, in particular for the acquisition or disposal of financial instruments, undertaken on the basis of the information contained in this marketing communication. In the event that the marketing communication contains any information about any results regarding the financial instruments indicated therein, these do not constitute any guarantee or forecast regarding the future results.