CBOE VIX volatility index futures (VIX) are up nearly 2% today to 22.8, having gained about 20% in recent days, with a peak near 24.5. The main risks currently being hedged by Wall Street are developments in the Middle East (including the potential paralysis of shipping through the Strait of Hormuz) as well as increasingly visible cracks in the private credit and private equity sectors, which were recently highlighted by Apollo Global Management. Among those facing difficulties with their financial products are U.S.-listed firms such as Blue Owl Capital and private markets giant Blackstone. Let’s take a look at what the VIX is currently signaling about S&P 500 volatility.

VIX (H1)

Looking at RSI, we can see a divergence - the indicator is cooling despite the index remaining in a clear upward trend. Meanwhile, the MACD structure suggests the possibility of short-term bearish momentum from the moving averages. On the other hand, on the hourly timeframe the VIX has pulled back to around 50, which could potentially leave room for another dynamic upward move.

Source: xStation5

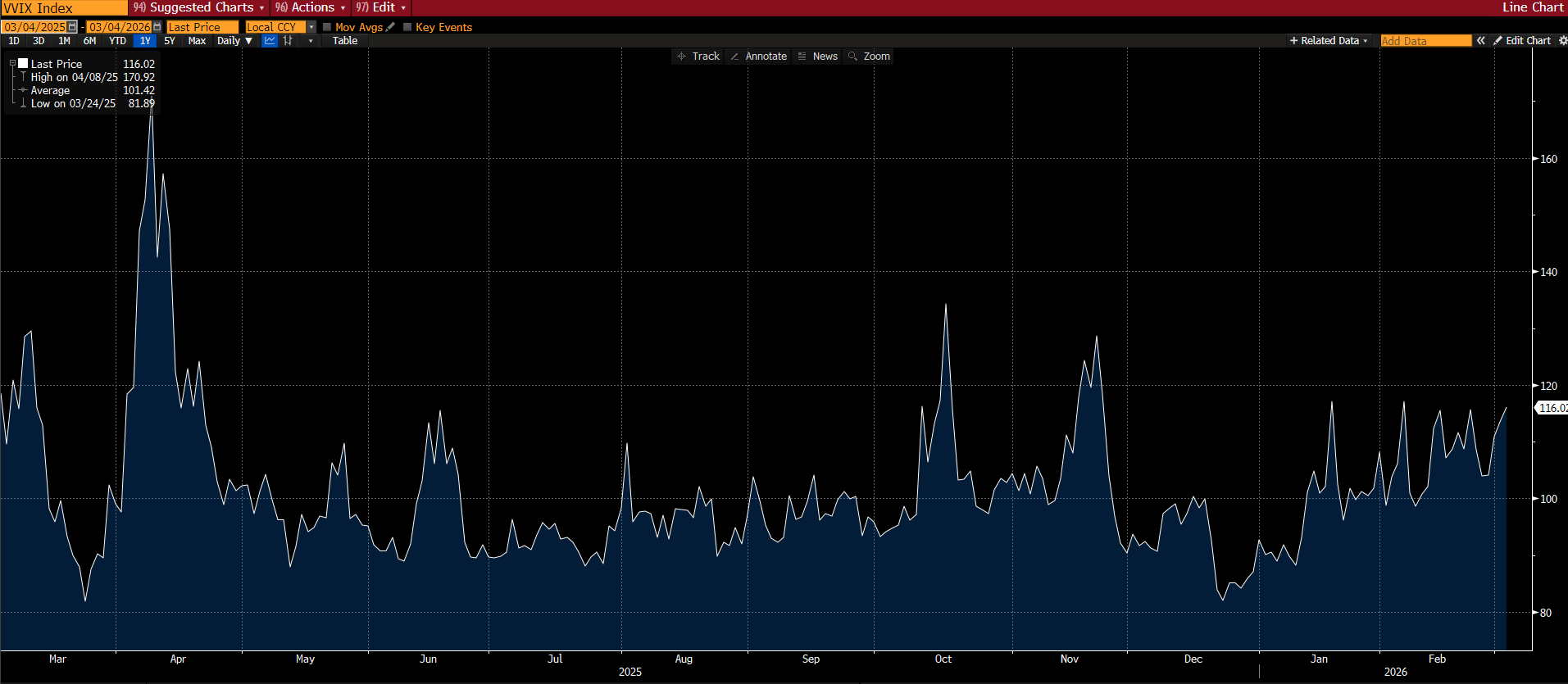

VVIX readings (the expected volatility of the volatility index itself) indicate strong demand for downside protection, although the market does not yet appear to be pricing in a probable crash — which would likely require VVIX above 130.

Source: Bloomberg Finance L.P.

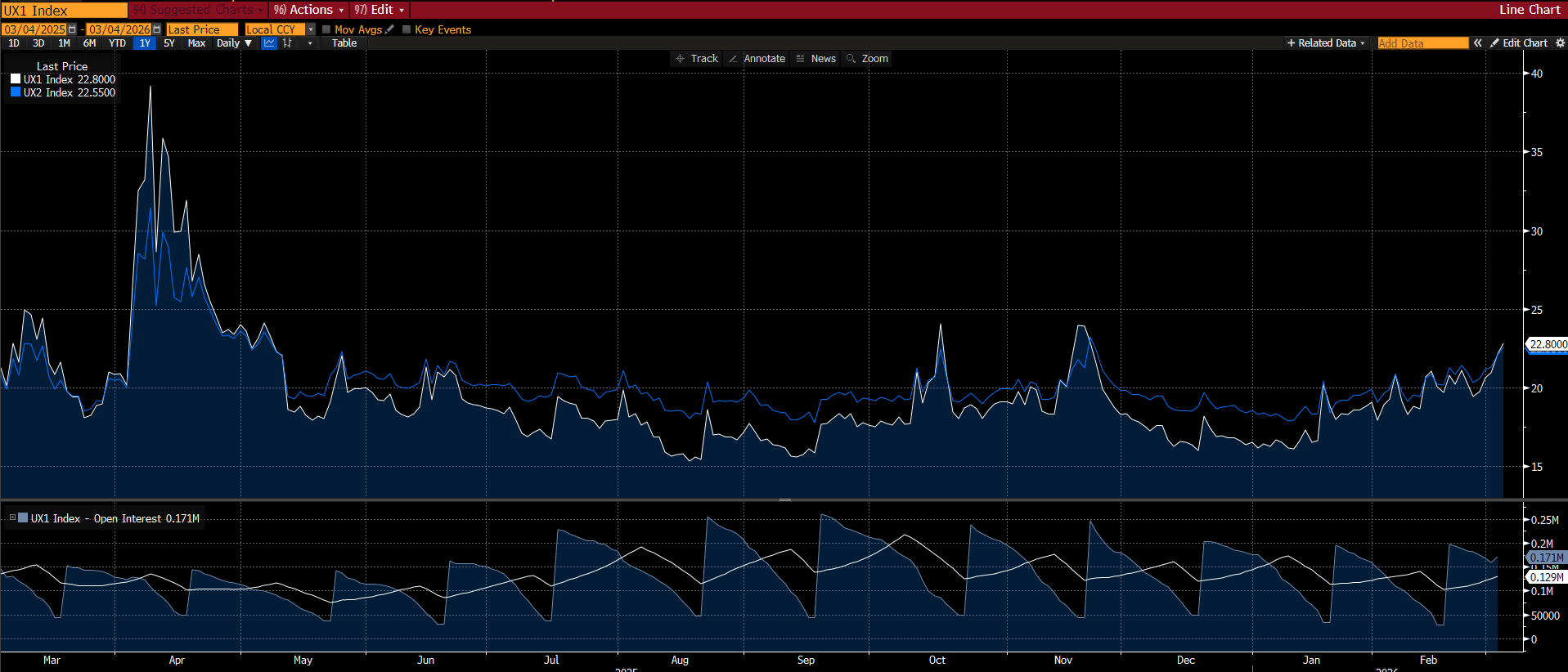

The spread between the front VIX futures contract and the next maturity shows only very mild backwardation (22.8 for UX1 vs 22.55 for UX2). This suggests that the market is pricing slightly elevated near-term risk, but remains far from anticipating a severe panic scenario. The volatility term structure remains relatively flat, pointing more to cautious short-term hedging than to expectations of a lasting volatility shock across markets.

Source: Bloomberg Finance L.P.

Daily summary: Sense of relief to global markets🎢 OIL prices dip 8%🚨

BREAKING: US ISM Manufacturing - Strong Beat Across the Board

Eurozone PMIs: German Factory Revival Masks Underlying Stagnation 🇪🇺

Wall Street rebounds as Q2 earnings season significantly exceeds investors expectations

The content of this report has been created by XTB S.A., with its registered office in Warsaw, at Prosta 67, 00-838 Warsaw, Poland, (KRS number 0000217580) and supervised by Polish Supervision Authority ( No. DDM-M-4021-57-1/2005). This material is a marketing communication within the meaning of Art. 24 (3) of Directive 2014/65/EU of the European Parliament and of the Council of 15 May 2014 on markets in financial instruments and amending Directive 2002/92/EC and Directive 2011/61/EU (MiFID II). Marketing communication is not an investment recommendation or information recommending or suggesting an investment strategy within the meaning of Regulation (EU) No 596/2014 of the European Parliament and of the Council of 16 April 2014 on market abuse (market abuse regulation) and repealing Directive 2003/6/EC of the European Parliament and of the Council and Commission Directives 2003/124/EC, 2003/125/EC and 2004/72/EC and Commission Delegated Regulation (EU) 2016/958 of 9 March 2016 supplementing Regulation (EU) No 596/2014 of the European Parliament and of the Council with regard to regulatory technical standards for the technical arrangements for objective presentation of investment recommendations or other information recommending or suggesting an investment strategy and for disclosure of particular interests or indications of conflicts of interest or any other advice, including in the area of investment advisory, within the meaning of the Trading in Financial Instruments Act of 29 July 2005 (i.e. Journal of Laws 2019, item 875, as amended). The marketing communication is prepared with the highest diligence, objectivity, presents the facts known to the author on the date of preparation and is devoid of any evaluation elements. The marketing communication is prepared without considering the client’s needs, his individual financial situation and does not present any investment strategy in any way. The marketing communication does not constitute an offer of sale, offering, subscription, invitation to purchase, advertisement or promotion of any financial instruments. XTB S.A. is not liable for any client’s actions or omissions, in particular for the acquisition or disposal of financial instruments, undertaken on the basis of the information contained in this marketing communication. In the event that the marketing communication contains any information about any results regarding the financial instruments indicated therein, these do not constitute any guarantee or forecast regarding the future results.