Vodafone (VOD.UK) shares jumped more than 11% on Friday after one of the largest transactions in the European telecommunications sector in recent years was announced. Vega, an investment vehicle controlled by the family of French telecom billionaire Xavier Niel, agreed to acquire Emirates Telecommunications Group's (e&) entire 16.2% stake in Vodafone for approximately £4.4 billion (€5.1 billion / around $6 billion).

At first glance, the market's reaction appeared to be driven simply by the acquisition price. However, investors saw much more than just a premium over Vodafone's previous share price. For many market participants, the transaction represents a strong vote of confidence from one of Europe's most experienced telecom investors, suggesting that Vodafone still has considerable untapped value.

This is more than just another block trade

Following regulatory approvals, Vega will become Vodafone's largest shareholder, replacing e&, which is exiting its investment entirely.

Importantly, Xavier Niel emphasized that he has no intention of acquiring the entire company. Under the UK Takeover Code, Vega has confirmed that the investment is intended to be a long-term strategic minority holding designed to support Vodafone's future development rather than gain control of the business.

That distinction matters. Markets typically view short-term financial investors very differently from strategic industry specialists with decades of operational experience. In this case, Vodafone is gaining a shareholder that has successfully built and developed some of Europe's largest telecommunications businesses.

The purchase price suggests Vodafone may have been undervalued

The shares were purchased at approximately 110.5 pence per share, in addition to Vodafone's final dividend.

For comparison, Vodafone closed the previous trading session at 97.76 pence.

A premium of this size inevitably attracts investors' attention. When one of Europe's most successful telecom investors is willing to pay significantly above the prevailing market price, it naturally raises the question of whether the public market had been undervaluing Vodafone.

That explains why the stock quickly moved toward the transaction price following the announcement.

Who is Xavier Niel, and why does the market care?

For many investors, the identity of the buyer is even more important than the acquisition premium itself.

Xavier Niel has long been regarded as one of Europe's most influential telecommunications entrepreneurs and investors. Through companies controlled by the Niel family group, he owns telecom assets across 26 countries in Europe and Latin America, serving approximately 139 million subscribers, employing 45,000 people, and generating around €24 billion in annual revenue alongside more than €9 billion of EBITDAaL.

The portfolio includes companies such as iliad, Salt, Monaco Telecom, Eir, Tele2, and Millicom.

His investment strategy has consistently focused on identifying undervalued telecom assets, improving operational efficiency, and creating shareholder value over the long term.

In announcing the transaction, Niel described Vodafone as a company with strong brands, high-quality assets, leadership positions across multiple markets, and substantial long-term growth potential. In his view, Vodafone's ongoing simplification of its corporate structure has positioned the company to enter a new phase of growth and stronger financial performance.

Is Vodafone finally approaching a turning point?

The past several years have not been easy for Vodafone.

The company has undertaken a broad restructuring program, divesting selected businesses, simplifying its organizational structure, and concentrating resources on its most attractive markets. Among the most significant milestones were the completion of the sale of its Italian operations and the planned merger of Vodafone UK with Three UK, which is expected to generate substantial cost synergies while strengthening the operator's competitive position.

Despite these efforts, investors have remained cautious. Europe's telecommunications industry continues to struggle with modest growth, intense pricing competition, and heavy capital expenditure requirements related to fiber and 5G network deployment.

As a result, many European telecom operators have continued trading at relatively low valuation multiples despite operational improvements.

Against this backdrop, the Niel family's investment can be interpreted as a signal that the market may still underestimate the benefits of Vodafone's restructuring as well as its long-term earnings and cash flow potential.

The risks have not disappeared

That does not mean the investment is without risk.

Vodafone still operates in a sector characterized by relatively slow structural growth and substantial capital requirements. Expanding fiber networks, rolling out 5G infrastructure, and maintaining competitiveness require billions of pounds of ongoing investment, while regulatory pressure and aggressive price competition continue to limit margin expansion.

Another important challenge remains Vodafone's debt burden and its ability to generate stable free cash flow. Maintaining healthy cash generation is essential not only to finance future investments but also to sustain shareholder distributions. Ultimately, the success of the company's restructuring will depend on whether management can translate a leaner corporate structure into sustainably higher profitability.

What should investors watch next?

Over the coming months, investors will primarily focus on the completion of the transaction and the first signs of cooperation between Vodafone's management team and its new largest shareholder.

From an investment perspective, however, three questions are likely to dominate attention:

- Can Vodafone continue improving its free cash flow generation?

- Will the restructuring translate into sustainably higher profitability?

- Can Xavier Niel's extensive telecom expertise help unlock greater value across Vodafone's European and African operations?

While Friday's rally was largely driven by the premium embedded in the acquisition price, the long-term significance of the transaction could prove much greater.

The market is not merely pricing in a higher valuation—it is also placing confidence in an investor who has repeatedly demonstrated an ability to create value in one of Europe's most challenging industries.

If Vodafone succeeds in converting years of restructuring into stronger earnings growth and free cash flow generation, Friday's transaction may ultimately be remembered as the moment investors began reassessing the company's long-term investment case.

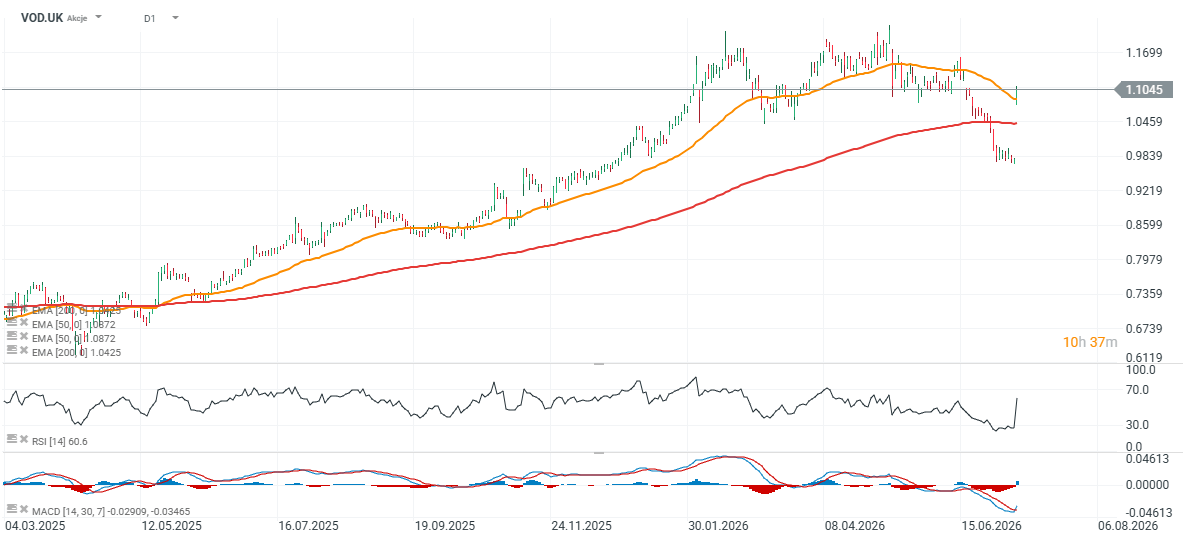

Vodafone share price chart (VOD.UK, Daily)

Following Xavier Niel's investment, Vodafone shares broke decisively above their 200-day exponential moving average (EMA200), attempting to reverse the long-term downtrend.

For the bullish scenario to remain intact, the stock will need to hold above the 105 pence area, where both the recent breakout gap and the 50-day EMA provide support. If buying momentum continues, the next major upside target lies around 117 pence, which represents the first significant technical resistance zone.

Source: xStation 5

Daily Summary 🗽 Wall Street Holds Firm Despite Weakness in Memory Stocks, Rising Oil Price

Moderna shares slide despite mFlusiva success 📉 What's next for the mRNA vaccines market giant?

Stock of the Week: Arista Networks—A Second-Tier Technology with Top-Tier Results

US Open: S&P 500 shows strength as semiconductor lags 🚩 Western Digital down 12%

The content of this report has been created by XTB S.A., with its registered office in Warsaw, at Prosta 67, 00-838 Warsaw, Poland, (KRS number 0000217580) and supervised by Polish Supervision Authority ( No. DDM-M-4021-57-1/2005). This material is a marketing communication within the meaning of Art. 24 (3) of Directive 2014/65/EU of the European Parliament and of the Council of 15 May 2014 on markets in financial instruments and amending Directive 2002/92/EC and Directive 2011/61/EU (MiFID II). Marketing communication is not an investment recommendation or information recommending or suggesting an investment strategy within the meaning of Regulation (EU) No 596/2014 of the European Parliament and of the Council of 16 April 2014 on market abuse (market abuse regulation) and repealing Directive 2003/6/EC of the European Parliament and of the Council and Commission Directives 2003/124/EC, 2003/125/EC and 2004/72/EC and Commission Delegated Regulation (EU) 2016/958 of 9 March 2016 supplementing Regulation (EU) No 596/2014 of the European Parliament and of the Council with regard to regulatory technical standards for the technical arrangements for objective presentation of investment recommendations or other information recommending or suggesting an investment strategy and for disclosure of particular interests or indications of conflicts of interest or any other advice, including in the area of investment advisory, within the meaning of the Trading in Financial Instruments Act of 29 July 2005 (i.e. Journal of Laws 2019, item 875, as amended). The marketing communication is prepared with the highest diligence, objectivity, presents the facts known to the author on the date of preparation and is devoid of any evaluation elements. The marketing communication is prepared without considering the client’s needs, his individual financial situation and does not present any investment strategy in any way. The marketing communication does not constitute an offer of sale, offering, subscription, invitation to purchase, advertisement or promotion of any financial instruments. XTB S.A. is not liable for any client’s actions or omissions, in particular for the acquisition or disposal of financial instruments, undertaken on the basis of the information contained in this marketing communication. In the event that the marketing communication contains any information about any results regarding the financial instruments indicated therein, these do not constitute any guarantee or forecast regarding the future results.